|

Code of Federal Regulations (Last Updated: November 8, 2024) |

|

Title 12 - Banks and Banking |

|

Chapter III - Federal Deposit Insurance Corporation |

|

SubChapter B - Regulations and Statements of General Policy |

|

Part 324 - Capital Adequacy of FDIC-Supervised Institutions |

|

Subpart D - Risk-Weighted Assets - Standardized Approach |

|

Risk-Weighted Assets for General Credit Risk |

§ 324.34 - Derivative contracts.

-

§ 324.34 Derivative contracts.

.(a) Exposure amount for derivative contracts -

(1) FDIC-supervised institution that is not an advanced approaches FDIC-supervised institution.

(i) A FDIC-supervised institution that is not an advanced approaches FDIC-supervised institution must use the current exposure methodology (CEM) described in paragraph (b) of this section to calculate the exposure amount for all its OTC derivative contracts

(a) Exposure amount -

(, unless the FDIC-supervised institution makes the election provided in paragraph (a)(1)(ii) of this section.

(ii) A FDIC-supervised institution that is not an advanced approaches FDIC-supervised institution may elect to calculate the exposure amount for all its OTC derivative contracts under the standardized approach for counterparty credit risk (SA-CCR) in § 324.132(c) by notifying the FDIC, rather than calculating the exposure amount for all its derivative contracts using CEM. A FDIC-supervised institution that elects under this paragraph (a)(1)(ii) to calculate the exposure amount for its OTC derivative contracts under SA-CCR must apply the treatment of cleared transactions under § 324.133 to its derivative contracts that are cleared transactions and to all default fund contributions associated with such derivative contracts, rather than applying § 324.35. A FDIC-supervised institution that is not an advanced approaches FDIC-supervised institution must use the same methodology to calculate the exposure amount for all its derivative contracts and, if a FDIC-supervised institution has elected to use SA-CCR under this paragraph (a)(1)(ii), the FDIC-supervised institution may change its election only with prior approval of the FDIC.

(2) Advanced approaches FDIC-supervised institution. An advanced approaches FDIC-supervised institution must calculate the exposure amount for all its derivative contracts using SA-CCR in § 324.132(c) for purposes of standardized total risk-weighted assets. An advanced approaches FDIC-supervised institution must apply the treatment of cleared transactions under § 324.133 to its derivative contracts that are cleared transactions and to all default fund contributions associated with such derivative contracts for purposes of standardized total risk-weighted assets.

b(b) Current exposure methodology exposure amount -

(1) Single OTC derivative contract. Except as modified by paragraph (

mark-to-c) of this section, the exposure amount for a single OTC derivative contract that is not subject to a qualifying master netting agreement is equal to the sum of the FDIC-supervised institution's current credit exposure and potential future credit exposure (PFE) on the OTC derivative contract.

(i) Current credit exposure. The current credit exposure for a single OTC derivative contract is the greater of the

mark-to-fair value of the OTC derivative contract or zero.

(ii) PFE.

(A) The PFE for a single OTC derivative contract, including an OTC derivative contract with a negative

§ 324fair value, is calculated by multiplying the notional principal amount of the OTC derivative contract by the appropriate conversion factor in Table 1 to

34.this section.

a)(B) For purposes of calculating either the PFE under this paragraph (

ab)(1)(ii) or the gross PFE under paragraph (

§ 324.34b)(2)(ii)(A) of this section for exchange rate contracts and other similar contracts in which the notional principal amount is equivalent to the cash flows, notional principal amount is the net receipts to each party falling due on each value date in each currency.

(C) For an OTC derivative contract that does not fall within one of the specified categories in Table 1 to

Anthis section, the PFE must be calculated using the appropriate “other” conversion factor.

(D)

AnA FDIC-supervised institution must use an OTC derivative contract's effective notional principal amount (that is, the apparent or stated notional principal amount multiplied by any multiplier in the OTC derivative contract) rather than the apparent or stated notional principal amount in calculating PFE.

(E) The PFE of the protection provider of a credit derivative is capped at the net present value of the amount of unpaid premiums.

Table 1 to § 324.34 - Conversion Factor Matrix for Derivative Contracts 1

Remaining maturity 2 Interest rate Foreign

exchange

rate and goldCredit

(investment

grade

reference

asset) 3Credit

(non-investment-

grade

reference asset)Equity Precious

metals

(except gold)Other One year or less 0.00 0.01 0.05 0.10 0.06 0.07 0.10 Greater than one year and less than or equal to five years 0.005 0.05 0.05 0.10 0.08 0.07 0.12 Greater than five years 0.015 0.075 0.05 0.10 0.10 0.08 0.15 Anb(2) Multiple OTC derivative contracts subject to a qualifying master netting agreement. Except as modified by paragraph (

mark-to-c) of this section, the exposure amount for multiple OTC derivative contracts subject to a qualifying master netting agreement is equal to the sum of the net current credit exposure and the adjusted sum of the PFE amounts for all OTC derivative contracts subject to the qualifying master netting agreement.

(i) Net current credit exposure. The net current credit exposure is the greater of the net sum of all positive and negative

equalsfair values of the individual OTC derivative contracts subject to the qualifying master netting agreement or zero.

(ii) Adjusted sum of the PFE amounts. The adjusted sum of the PFE amounts, Anet, is calculated as Anet = (0.4 × Agross) + (0.6 × NGR × Agross), where:

(A) Agross

a= the gross PFE (that is, the sum of the PFE amounts as determined under paragraph (

equalsb)(1)(ii) of this section for each individual derivative contract subject to the qualifying master netting agreement); and

(B) Net-to-gross Ratio (NGR)

a= the ratio of the net current credit exposure to the gross current credit exposure. In calculating the NGR, the gross current credit exposure equals the sum of the positive current credit exposures (as determined under paragraph (

b)(1)(i) of this section) of all individual derivative contracts subject to the qualifying master netting agreement.

b(

Anc) Recognition of credit risk mitigation of collateralized OTC derivative contracts.

(1)

anA FDIC-supervised institution using CEM under paragraph (b) of this section may recognize the credit risk mitigation benefits of financial collateral that secures an OTC derivative contract or multiple OTC derivative contracts subject to a qualifying master netting agreement (netting set) by using the simple approach in § 324.37(b).

(2) As an alternative to the simple approach,

exposure as if it were uncollateralized anda FDIC-supervised institution using CEM under paragraph (b) of this section may recognize the credit risk mitigation benefits of financial collateral that secures such a contract or netting set if the financial collateral is marked-to-fair value on a daily basis and subject to a daily margin maintenance requirement by applying a risk weight to the

auncollateralized portion of the exposure, after adjusting the exposure amount calculated under paragraph (

a ∑Eb)(1) or (2) of this section using the collateral haircut approach in § 324.37(c). The FDIC-supervised institution must substitute the exposure amount calculated under paragraph (

ΣE in the equation in § 324.37(c)(2).

c(

OTCd)Counterparty credit risk for

Ancredit derivatives -

(1) Protection purchasers.

an OTCA FDIC-supervised institution that purchases

Da credit derivative that is recognized under § 324.36 as a credit risk mitigant for an exposure that is not a covered position under subpart F of this part is not required to compute a separate counterparty credit risk capital requirement under this subpart

Anprovided that the FDIC-supervised institution does so consistently for all such credit derivatives. The FDIC-supervised institution must either include all or exclude all such credit derivatives that are subject to a qualifying master netting agreement from any measure used to determine counterparty credit risk exposure to all relevant counterparties for risk-based capital purposes.

(2) Protection providers.

(i)

an OTCA FDIC-supervised institution that is the protection provider under

OTCa credit derivative must treat the

OTCcredit derivative as an exposure to the underlying reference asset. The FDIC-supervised institution is not required to compute a counterparty credit risk capital requirement for the

Dcredit derivative under this subpart

OTC, provided that this treatment is applied consistently for all such

OTCcredit derivatives. The FDIC-supervised institution must either include all or exclude all such

ccredit derivatives that are subject to a qualifying master netting agreement from any measure used to determine counterparty credit risk exposure.

(ii) The provisions of this paragraph (

OTCd)(2) apply to all relevant counterparties for risk-based capital purposes unless the FDIC-supervised institution is treating the

credit derivative as a covered position under subpart F of this part, in which case the FDIC-supervised institution must compute a supplemental counterparty credit risk capital requirement under this section.

d(

OTCe)Counterparty credit risk for

Anequity derivatives.

(1)

OTCA FDIC-supervised institution must treat an

OTCequity derivative contract as an equity exposure and compute a risk-weighted asset amount for the

OTCequity derivative contract under §§ 324.51 through 324.53 (unless the FDIC-supervised institution is treating the contract as a covered position under subpart F of this part).

(2) In addition, the FDIC-supervised institution must also calculate a risk-based capital requirement for the counterparty credit risk of an

OTCequity derivative contract under this section if the FDIC-supervised institution is treating the contract as a covered position under subpart F of this part.

(3) If the FDIC-supervised institution risk weights the contract under the Simple Risk-Weight Approach (SRWA) in § 324.52, the FDIC-supervised institution may choose not to hold risk-based capital against the counterparty credit risk of the

OTCequity derivative contract, as long as it does so for all such contracts. Where the

anequity derivative contracts are subject to a qualified master netting agreement,

a FDIC-supervised institution using the SRWA must either include all or exclude all of the contracts from any measure used to determine counterparty credit risk exposure.

e(

Af)Clearing member FDIC-supervised institution's exposure amount.

's exposure amount for an OTC derivative contractThe exposure amount of a clearing member FDIC-supervised institution

OTC derivative contracts where the FDIC-supervised institution is either acting as a financial intermediary and enters into an offsetting transaction with a QCCP or where the FDIC-supervised institution provides a guarantee to the QCCP on the performance of the clientusing CEM under paragraph (b) of this section for a client-facing derivative transaction or netting set of

aclient-facing derivative transactions equals the exposure amount calculated according to paragraph (

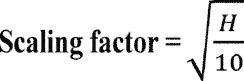

71whereb)(1) or (2) of this section multiplied by the scaling factor the square root of 1⁄2 (which equals 0.

707107). If the FDIC-supervised institution determines that a longer period is appropriate, the FDIC-supervised institution must use a larger scaling factor to adjust for a longer holding period as follows:

Where H

equals= the holding period greater than or equal to five days. Additionally, the FDIC may require the FDIC-supervised institution to set a longer holding period if the FDIC determines that a longer period is appropriate due to the nature, structure, or characteristics of the transaction or is commensurate with the risks associated with the transaction.

[78 85 FR 554714431, SeptJan. 10, 2013, as amended at 79 FR 20760, Apr. 14, 2014; 84 FR 35276, July 22, 201924, 2020]