2023-22823. Medicare Program; Medicare Part B Monthly Actuarial Rates, Premium Rates, and Annual Deductible Beginning January 1, 2024

-

Start Preamble

AGENCY:

Centers for Medicare & Medicaid Services (CMS), Department of Health and Human Services (HHS).

ACTION:

Notice.

SUMMARY:

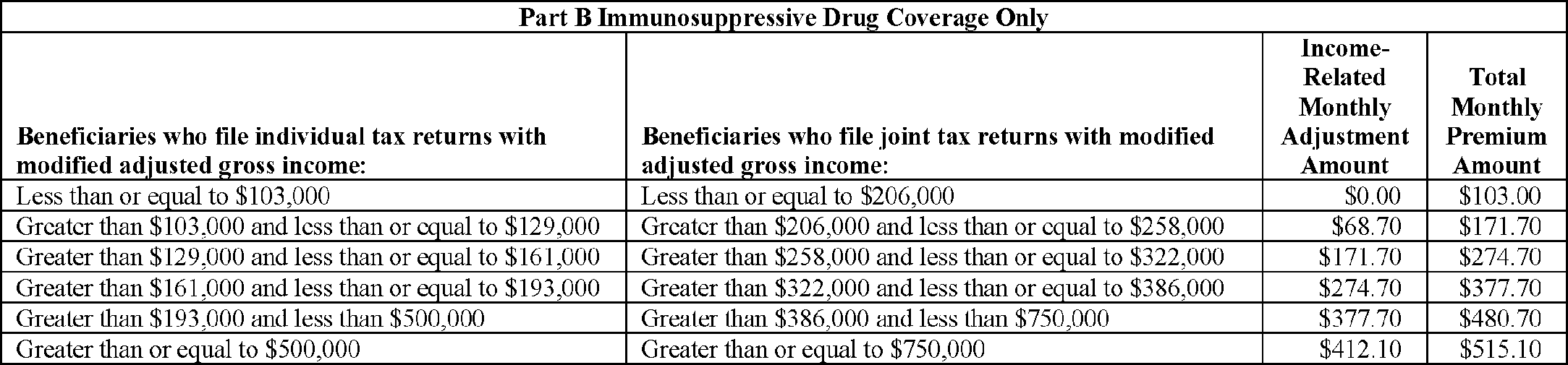

This notice announces the monthly actuarial rates for aged (age 65 and over) and disabled (under age 65) beneficiaries enrolled in Part B of the Medicare Supplementary Medical Insurance (SMI) program beginning January 1, 2024. In addition, this notice announces the monthly premium for aged and disabled beneficiaries, the deductible for 2024, and the income-related monthly adjustment amounts to be paid by beneficiaries with modified adjusted gross income above certain threshold amounts. The monthly actuarial rates for 2024 are $343.40 for aged enrollees and $427.20 for disabled enrollees. The standard monthly Part B premium rate for all enrollees for 2024 is $174.70, which is equal to 50 percent of the monthly actuarial rate for aged enrollees (or approximately 25 percent of the expected average total cost of Part B coverage for aged enrollees) plus the $3.00 repayment amount required under current law. (The 2024 premium is 5.9 percent or $9.80 higher than the 2023 standard premium rate of $164.90, which included the $3.00 repayment amount.) The Part B deductible for 2024 is $240.00 for all Part B beneficiaries. If a beneficiary has to pay an income-related monthly adjustment amount, that individual will have to pay a total monthly premium of about 35, 50, 65, 80, or 85 percent of the total cost of Part B coverage plus a repayment amount of $4.20, $6.00, $7.80, $9.60, or $10.20, respectively. Beginning in 2023, certain Medicare enrollees who are 36 months post kidney transplant, and therefore are no longer eligible for full Medicare coverage, can elect to continue Part B coverage of immunosuppressive drugs by paying a premium. For 2024, the immunosuppressive drug premium is $103.00.

DATES:

The monthly actuarial rates are effective on January 1, 2024.

Start Further InfoFOR FURTHER INFORMATION CONTACT:

M. Kent Clemens, (410) 786–6391.

End Further Info End Preamble Start Supplemental InformationSUPPLEMENTARY INFORMATION:

I. Background

Part B is the voluntary portion of the Medicare program that pays all or part of the costs for physicians' services; outpatient hospital services; certain home health services; services furnished by rural health clinics, ambulatory surgical centers, and comprehensive outpatient rehabilitation facilities; and certain other medical and health services not covered by Medicare Part Start Printed Page 71556 A, Hospital Insurance. Medicare Part B is available to individuals who are entitled to Medicare Part A, as well as to U.S. residents who have attained age 65 and are citizens and to non-citizens who were lawfully admitted for permanent residence and have resided in the United States for 5 consecutive years. Part B requires enrollment and payment of monthly premiums, as described in 42 CFR part 407, subpart B, and part 408, respectively. The premiums paid by (or on behalf of) all enrollees fund approximately one-fourth of the total incurred costs, and transfers from the general fund of the Treasury pay approximately three-fourths of these costs.

The Secretary of Health and Human Services (the Secretary) is required by section 1839 of the Social Security Act (the Act) to announce the Part B monthly actuarial rates for aged and disabled beneficiaries as well as the monthly Part B premium. The Part B annual deductible, income-related monthly adjustment amounts, and the immunosuppressive drug premium are included because their determinations are directly linked to the aged actuarial rate.

The monthly actuarial rates for aged and disabled enrollees are used to determine the correct amount of general revenue financing per beneficiary each month. These amounts, according to actuarial estimates, will equal, respectively, one-half of the expected average monthly cost of Part B for each aged enrollee (age 65 or over) and one-half of the expected average monthly cost of Part B for each disabled enrollee (under age 65).

The Part B deductible to be paid by enrollees is also announced. Prior to the Medicare Prescription Drug, Improvement, and Modernization Act of 2003 (MMA) (Pub. L. 108–173), the Part B deductible was set in statute. After setting the 2005 deductible amount at $110.00, section 629 of the MMA (amending section 1833(b) of the Act) required that the Part B deductible be indexed beginning in 2006. The inflation factor to be used each year is the annual percentage increase in the Part B actuarial rate for enrollees age 65 and over. Specifically, the 2024 Part B deductible is calculated by multiplying the 2023 deductible by the ratio of the 2024 aged actuarial rate to the 2023 aged actuarial rate. The amount determined under this formula is then rounded to the nearest $1.00.

The monthly Part B premium rate to be paid by aged and disabled enrollees is also announced. (Although the costs to the program per disabled enrollee are different than for the aged, the statute provides that the two groups pay the same premium amount.) Beginning with the passage of section 203 of the Social Security Amendments of 1972 (Pub. L. 92–603), the premium rate, which was determined on a fiscal-year basis, was limited to the lesser of the actuarial rate for aged enrollees, or the current monthly premium rate increased by the same percentage as the most recent general increase in monthly Title II Social Security benefits.

However, the passage of section 124 of the Tax Equity and Fiscal Responsibility Act of 1982 (TEFRA) (Pub. L. 97–248) suspended this premium determination process. Section 124 of TEFRA changed the premium basis to 50 percent of the monthly actuarial rate for aged enrollees (that is, 25 percent of program costs for aged enrollees). Section 606 of the Social Security Amendments of 1983 (Pub. L. 98–21), section 2302 of the Deficit Reduction Act of 1984 (DEFRA 84) (Pub. L. 98–369), section 93130 of the Consolidated Omnibus Budget Reconciliation Act of 1985 (COBRA 85) (Pub. L. 99–272), section 4080 of the Omnibus Budget Reconciliation Act of 1987 (OBRA 87) (Pub. L. 100–203), and section 6301 of the Omnibus Budget Reconciliation Act of 1989 (OBRA 89) (Pub. L. 101–239) extended the provision that the premium be based on 50 percent of the monthly actuarial rate for aged enrollees (that is, 25 percent of program costs for aged enrollees). This extension expired at the end of 1990.

The premium rate for 1991 through 1995 was legislated by section 1839(e)(1)(B) of the Act, as added by section 4301 of the Omnibus Budget Reconciliation Act of 1990 (OBRA 90) (Pub. L. 101–508). In January 1996, the premium determination basis would have reverted to the method established by the 1972 Social Security Act Amendments. However, section 13571 of the Omnibus Budget Reconciliation Act of 1993 (OBRA 93) (Pub. L. 103–66) changed the premium basis to 50 percent of the monthly actuarial rate for aged enrollees (that is, 25 percent of program costs for aged enrollees) for 1996 through 1998.

Section 4571 of the Balanced Budget Act of 1997 (BBA) (Pub. L. 105–33) permanently extended the provision that the premium be based on 50 percent of the monthly actuarial rate for aged enrollees (that is, 25 percent of program costs for aged enrollees).

The BBA included a further provision affecting the calculation of the Part B actuarial rates and premiums for 1998 through 2003. Section 4611 of the BBA modified the home health benefit payable under Part A for individuals enrolled in Part B. Under this section, beginning in 1998, expenditures for home health services not considered “post-institutional” are payable under Part B rather than Part A. However, section 4611(e)(1) of the BBA required that there be a transition from 1998 through 2002 for the aggregate amount of the expenditures transferred from Part A to Part B. Section 4611(e)(2) of the BBA also provided a specific yearly proportion for the transferred funds. The proportions were one-sixth for 1998, one-third for 1999, one-half for 2000, two-thirds for 2001, and five-sixths for 2002. For the purpose of determining the correct amount of financing from general revenues of the Federal Government, it was necessary to include only these transitional amounts in the monthly actuarial rates for both aged and disabled enrollees, rather than the total cost of the home health services being transferred.

Section 4611(e)(3) of the BBA also specified, for the purpose of determining the premium, that the monthly actuarial rate for enrollees age 65 and over be computed as though the transition would occur for 1998 through 2003 and that one-seventh of the cost be transferred in 1998, two-sevenths in 1999, three-sevenths in 2000, four-sevenths in 2001, five-sevenths in 2002, and six-sevenths in 2003. Therefore, the transition period for incorporating this home health transfer into the premium was 7 years while the transition period for including these services in the actuarial rate was 6 years.

Section 811 of the MMA, which amended section 1839 of the Act, requires that, starting on January 1, 2007, the Part B premium a beneficiary pays each month be based on that individual's annual income. (The MMA specified that there be a 5-year transition period to reach full implementation of this provision. However, section 5111 of the Deficit Reduction Act of 2005 (DRA) (Pub. L. 109–171) modified the transition to a 3-year period, which ended in 2009.) Specifically, if a beneficiary's modified adjusted gross income is greater than the legislated threshold amounts (for 2024, $103,000 for a beneficiary filing an individual income tax return and $206,000 for a beneficiary filing a joint tax return), the beneficiary is responsible for a larger portion of the estimated total cost of Part B benefit coverage. In addition to the standard 25-percent premium, these beneficiaries now have to pay an income-related monthly adjustment amount. The MMA made no change to the actuarial rate calculation, and the standard premium, which will continue to be paid by Start Printed Page 71557 beneficiaries whose modified adjusted gross income is below the applicable thresholds, still represents 25 percent of the estimated total cost to the program of Part B coverage for an aged enrollee. However, depending on income and tax filing status, a beneficiary can now be responsible for 35, 50, 65, 80, or 85 percent of the estimated total cost of Part B coverage, rather than 25 percent. Section 402 of the Medicare Access and CHIP Reauthorization Act of 2015 (MACRA) (Pub. L. 114–10) modified the income thresholds beginning in 2018, and section 53114 of the Bipartisan Budget Act of 2018 (BBA of 2018) (Pub. L. 115–123) further modified the income thresholds beginning in 2019. For years beginning in 2019, the BBA of 2018 established a new income threshold. If a beneficiary's modified adjusted gross income is greater than or equal to $500,000 for a beneficiary filing an individual income tax return and $750,000 for a beneficiary filing a joint tax return, the beneficiary is responsible for 85 percent of the estimated total cost of Part B coverage. The BBA of 2018 specified that these new income threshold levels be inflation-adjusted beginning in 2028. The end result of the higher premium is that the Part B premium subsidy is reduced, and less general revenue financing is required, for beneficiaries with higher income because they are paying a larger share of the total cost with their premium. That is, the premium subsidy continues to be approximately 75 percent for beneficiaries with income below the applicable income thresholds, but it will be reduced for beneficiaries with income above these thresholds.

The Consolidated Appropriations Act, 2021 (Pub. L. 116–260) established a new basis for Medicare Part B eligibility for post-kidney-transplant immunosuppressive drug coverage only. Medicare eligibility due solely to end-stage renal disease generally ends 36 months after a successful kidney transplant. Beginning in 2023, post-kidney-transplant individuals without certain types of insurance coverage can elect to enroll in Part B and receive coverage of immunosuppressive drugs only. The premium for this continuation of coverage is 15 percent of a different aged actuarial rate, which is equal to 100 percent of costs for aged enrollees (rather than the standard aged actuarial rate, which is equal to one-half of the costs for aged enrollees). Enrollees paying the immunosuppressive premium are not subject to the late enrollment penalty and the $3.00 repayment amounts, but they are subject to the hold-harmless provision (described later) and the income-related monthly adjustment amounts. The law requires transfers equal to the reduction in aggregate premiums payable that results from enrollees with coverage only for immunosuppressive drugs paying the immunosuppressive drug Part B premium rather than the standard Part B premium. These transfers are to be treated as premiums payable for general revenue matching purposes.

Section 4732(c) of the BBA added section 1933(c) of the Act, which required the Secretary to allocate money from the Part B trust fund to the State Medicaid programs for the purpose of providing Medicare Part B premium assistance from 1998 through 2002 for the low-income Medicaid beneficiaries who qualify under section 1933 of the Act. This allocation, while not a benefit expenditure, was an expenditure of the trust fund and was included in calculating the Part B actuarial rates through 2002. For 2003 through 2015, the expenditure was made from the trust fund because the allocation was temporarily extended. However, because the extension occurred after the financing was determined, the allocation was not included in the calculation of the financing rates for these years. Section 211 of MACRA permanently extended this expenditure, which is included in the calculation of the Part B actuarial rates for 2016 and subsequent years.

Another provision affecting the calculation of the Part B premium is section 1839(f) of the Act, as amended by section 211 of the Medicare Catastrophic Coverage Act of 1988 (MCCA 88) (Pub. L. 100–360). (The Medicare Catastrophic Coverage Repeal Act of 1989 (Pub. L. 101–234) did not repeal the revisions to section 1839(f) of the Act made by MCCA 88.) Section 1839(f) of the Act, referred to as the hold-harmless provision, provides that, if an individual is entitled to benefits under section 202 or 223 of the Act (the Old-Age and Survivors Insurance Benefit and the Disability Insurance Benefit, respectively) and has the Part B premium deducted from these benefit payments, the premium increase will be reduced, if necessary, to avoid causing a decrease in the individual's net monthly payment. This decrease in payment occurs if the increase in the individual's Social Security benefit due to the cost-of-living adjustment under section 215(i) of the Act is less than the increase in the premium. Specifically, the reduction in the premium amount applies if the individual is entitled to benefits under section 202 or 223 of the Act for November and December of a particular year and the individual's Part B premiums for December and the following January are deducted from the respective month's section 202 or 223 benefits. The hold-harmless provision does not apply to beneficiaries who are required to pay an income-related monthly adjustment amount.

A check for benefits under section 202 or 223 of the Act is received in the month following the month for which the benefits are due. The Part B premium that is deducted from a particular check is the Part B payment for the month in which the check is received. Therefore, a benefit check for November is not received until December, but December's Part B premium has been deducted from it.

Generally, if a beneficiary qualifies for hold-harmless protection, the reduced premium for the individual for that January and for each of the succeeding 11 months is the greater of either—

- The monthly premium for January reduced as necessary to make the December monthly benefits, after the deduction of the Part B premium for January, at least equal to the preceding November's monthly benefits, after the deduction of the Part B premium for December; or

- The monthly premium for that individual for that December.

In determining the premium limitations under section 1839(f) of the Act, the monthly benefits to which an individual is entitled under section 202 or 223 of the Act do not include retroactive adjustments or payments and deductions on account of work. Also, once the monthly premium amount is established under section 1839(f) of the Act, it will not be changed during the year even if there are retroactive adjustments or payments and deductions on account of work that apply to the individual's monthly benefits.

Individuals who have enrolled in Part B late or who have re-enrolled after the termination of a coverage period are subject to an increased premium under section 1839(b) of the Act. The increase is a percentage of the premium and is based on the new premium rate before any reductions under section 1839(f) of the Act are made.

Section 1839 of the Act, as amended by section 601(a) of the Bipartisan Budget Act of 2015 (Pub. L. 114–74), specified that the 2016 actuarial rate for enrollees age 65 and older be determined as if the hold-harmless provision did not apply. The premium revenue that was lost by using the resulting lower premium (excluding the forgone income-related premium revenue) was replaced by a transfer of general revenue from the Treasury, Start Printed Page 71558 which will be repaid over time to the general fund.

Similarly, section 1839 of the Act, as amended by section 2401 of the Continuing Appropriations Act, 2021 and Other Extensions Act (Pub. L. 116–159), specified that the 2021 actuarial rate for enrollees age 65 and older be determined as the sum of the 2020 actuarial rate for enrollees age 65 and older and one-fourth of the difference between the 2020 actuarial rate and the preliminary 2021 actuarial rate (as determined by the Secretary) for such enrollees. The premium revenue lost by using the resulting lower premium (excluding the forgone income-related premium revenue) was replaced by a transfer of general revenue from the Treasury, which will be repaid over time.

Starting in 2016, in order to repay the balance due (which includes the transfer amounts and the forgone income-related premium revenue from the Bipartisan Budget Act of 2015 and the Continuing Appropriations Act, 2021 and Other Extensions Act), the Part B premium otherwise determined will be increased by $3.00. These repayment amounts will be added to the Part B premium otherwise determined each year and will be paid back to the general fund of the Treasury, and they will continue until the balance due is paid back.

High-income enrollees pay the $3.00 repayment amount plus an additional $1.20, $3.00, $4.80, $6.60, or $7.20 in repayment as part of the income-related monthly adjustment amount (IRMAA) premium dollars, which reduce (dollar for dollar) the amount of general revenue received by Part B from the general fund of the Treasury. Because of this general revenue offset, the repayment IRMAA premium dollars are not included in the direct repayments made to the general fund of the Treasury from Part B in order to avoid a double repayment. (Only the $3.00 monthly repayment amounts are included in the direct repayments.)

These repayment amounts will continue until the balance due is zero. (In the final year of the repayment, the additional amounts may be modified to avoid an overpayment.) The repayment amounts (excluding those for high-income enrollees) are subject to the hold-harmless provision. The original balance due was $9,066,409,000, consisting of $1,625,761,000 in forgone income-related premium revenue plus a transfer amount of $7,440,648,000 from the provisions of the Bipartisan Budget Act of 2015. The increase in the balance due in 2021 was $8,799,829,000, consisting of $946,046,000 in forgone income-related premium income plus a transfer amount of $7,853,783,000 from the provisions of the Continuing Appropriations Act, 2021 and Other Extensions Act. An estimated $14,624,044,000 will have been repaid to the general fund by the end of 2023, with an estimated $3,242,194,000 remaining to be repaid.

II. Provisions of the Notice

A. Notice of Medicare Part B Monthly Actuarial Rates, Monthly Premium Rates, and Annual Deductible

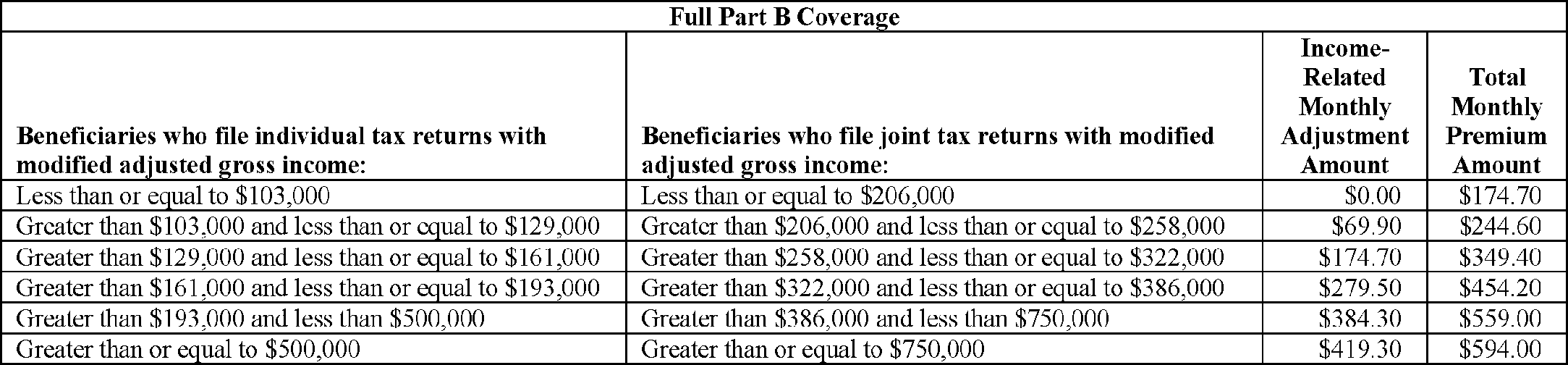

The Medicare Part B monthly actuarial rates applicable for 2024 are $343.40 for enrollees age 65 and over and $427.20 for disabled enrollees under age 65. In section II.B. of this notice, we present the actuarial assumptions and bases from which these rates are derived. The Part B standard monthly premium rate for all enrollees for 2024 is $174.70. The Part B immunosuppressive drug premium is $103.00.

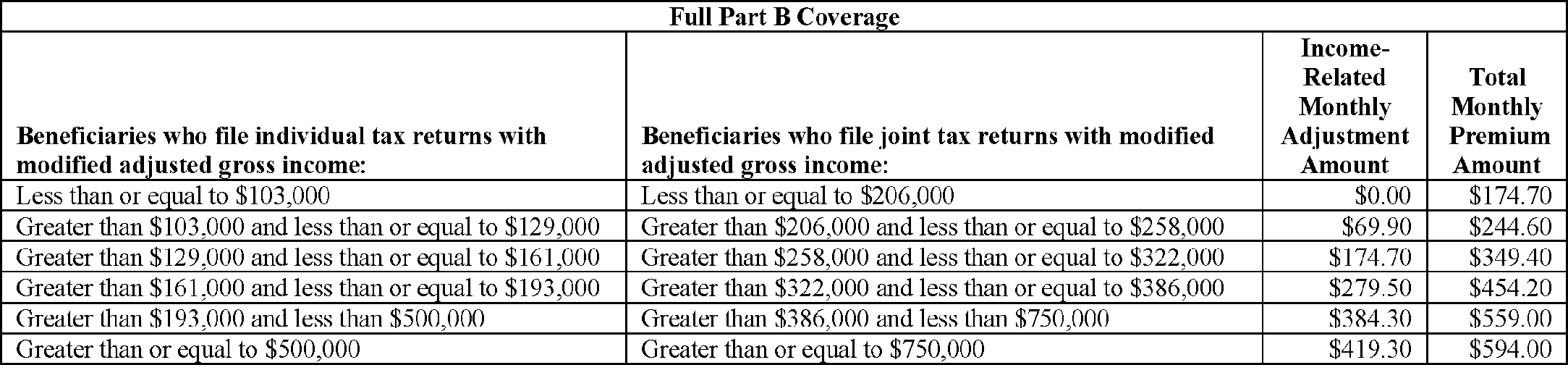

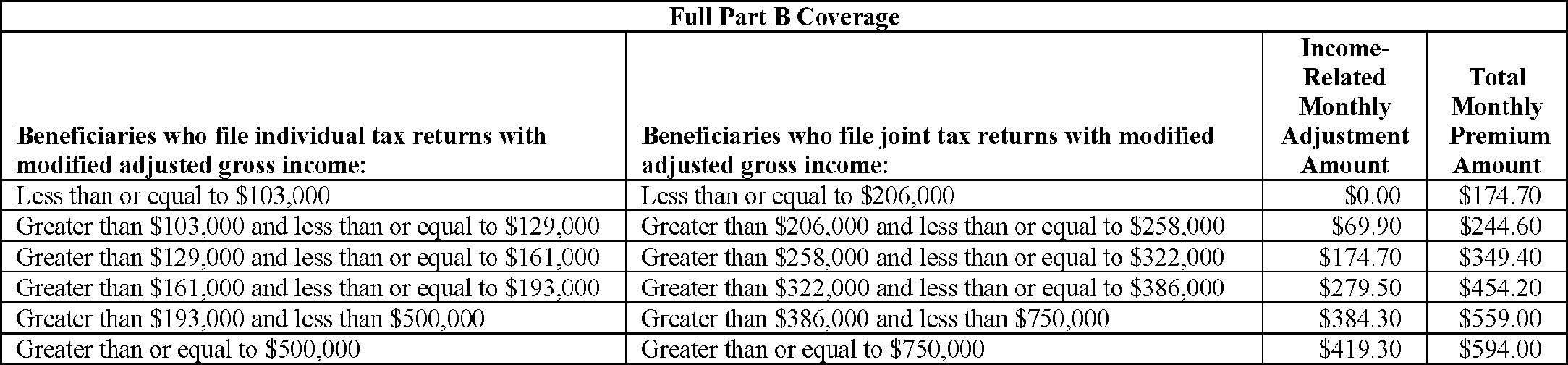

The following are the 2024 Part B monthly premium rates to be paid by (or on behalf of) beneficiaries with full Part B coverage who file either individual tax returns (and are single individuals, heads of households, qualifying widows or widowers with dependent children, or married individuals filing separately who lived apart from their spouses for the entire taxable year) or joint tax returns.

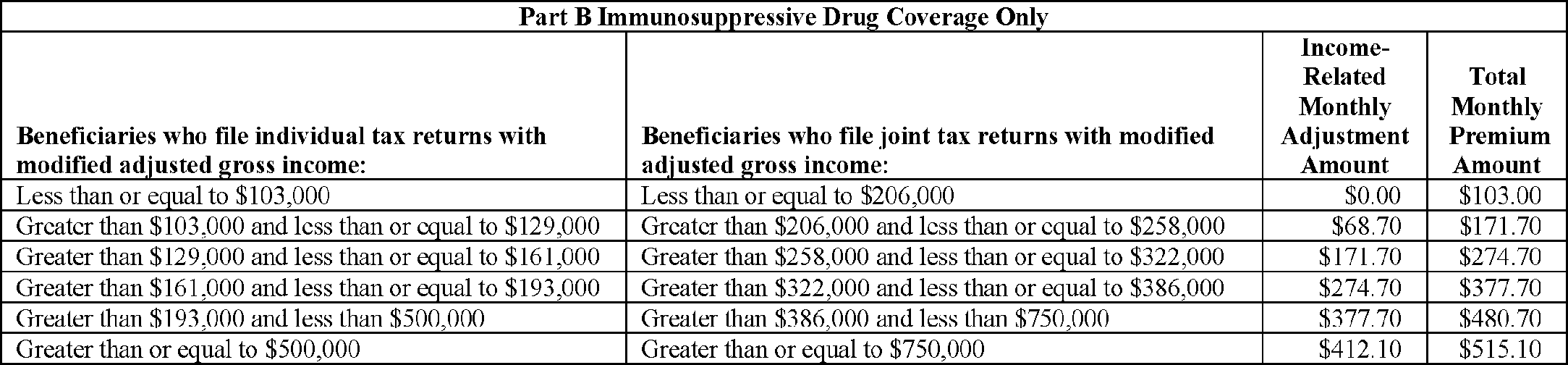

For beneficiaries with immunosuppressive drug only Part B coverage, who file either individual tax returns (and are single individuals, heads of households, qualifying widows or widowers with dependent children, or married individuals filing separately who lived apart from their spouses for the entire taxable year) or joint tax returns, the 2024 Part B monthly premium rates are shown below.

Start Printed Page 71559

In addition, the monthly premium rates to be paid by (or on behalf of) beneficiaries with full Part B coverage who are married and lived with their spouses at any time during the taxable year, but who file separate tax returns from their spouses, are as follows:

The monthly premium rates to be paid by (or on behalf of) beneficiaries with immunosuppressive drug only Part B coverage who are married and lived with their spouses at any time during the taxable year, but who file separate tax returns from their spouses, are as follows:

The Part B annual deductible for 2024 is $240.00 for all beneficiaries.

B. Statement of Actuarial Assumptions and Bases Employed in Determining the Monthly Actuarial Rates and the Monthly Premium Rate for Part B Beginning January 2024

Except where noted, the actuarial assumptions and bases used to determine the monthly actuarial rates and the monthly premium rates for Part B are established by the Centers for Medicare & Medicaid Services' Office of the Actuary. The estimates underlying these determinations are prepared by actuaries meeting the qualification standards and following the actuarial standards of practice established by the Actuarial Standards Board.

1. Actuarial Status of the Part B Account in the Supplementary Medical Insurance Trust Fund

Under section 1839 of the Act, the starting point for determining the standard monthly premium is the amount that would be necessary to finance Part B on an incurred basis. This is the amount of income that would be sufficient to pay for services furnished during that year (including associated administrative costs) even though payment for some of these services will not be made until after the close of the year. The portion of income required to cover benefits not paid until after the close of the year is added to the trust fund and used when needed.

Because the premium rates are established prospectively, they are subject to projection error. Additionally, legislation enacted after the financing was established, but effective for the period in which the financing is set, may affect program costs. As a result, the income to the program may not equal incurred costs. Trust fund assets must therefore be maintained at a level that is adequate to cover an appropriate degree of variation between actual and projected costs, and the amount of incurred, but unpaid, expenses. Numerous factors determine what level of assets is appropriate to cover variation between actual and projected costs. For 2024, the four most important of these factors are (1) the impact of expected additional payments from the Part B account to 340B providers in response to a judicial remand order; (2) the difference from prior years between the actual performance of the program and estimates made at the time financing was established; (3) the likelihood and potential magnitude of expenditure changes resulting from enactment of legislation affecting Part B costs in a year subsequent to the Start Printed Page 71560 establishment of financing for that year; and (4) the expected relationship between incurred and cash expenditures. The projected costs have a somewhat higher degree of uncertainty for 2024 due to the impact of the judicial remand order resulting in additional 340B drug payments. The other three factors are analyzed on an ongoing basis, as the trends can vary over time.

Table 1 summarizes the estimated actuarial status of the trust fund as of the end of the financing period for 2022 and 2023.

2. Monthly Actuarial Rate for Enrollees Age 65 and Older

The monthly actuarial rate for enrollees age 65 and older is one-half of the sum of monthly amounts for (1) the projected cost of benefits and (2) administrative expenses for each enrollee age 65 and older, after adjustments to this sum to allow for interest earnings on assets in the trust fund and an adequate contingency margin. The contingency margin is an amount appropriate to provide for possible variation between actual and projected costs and to amortize any surplus assets or unfunded liabilities.

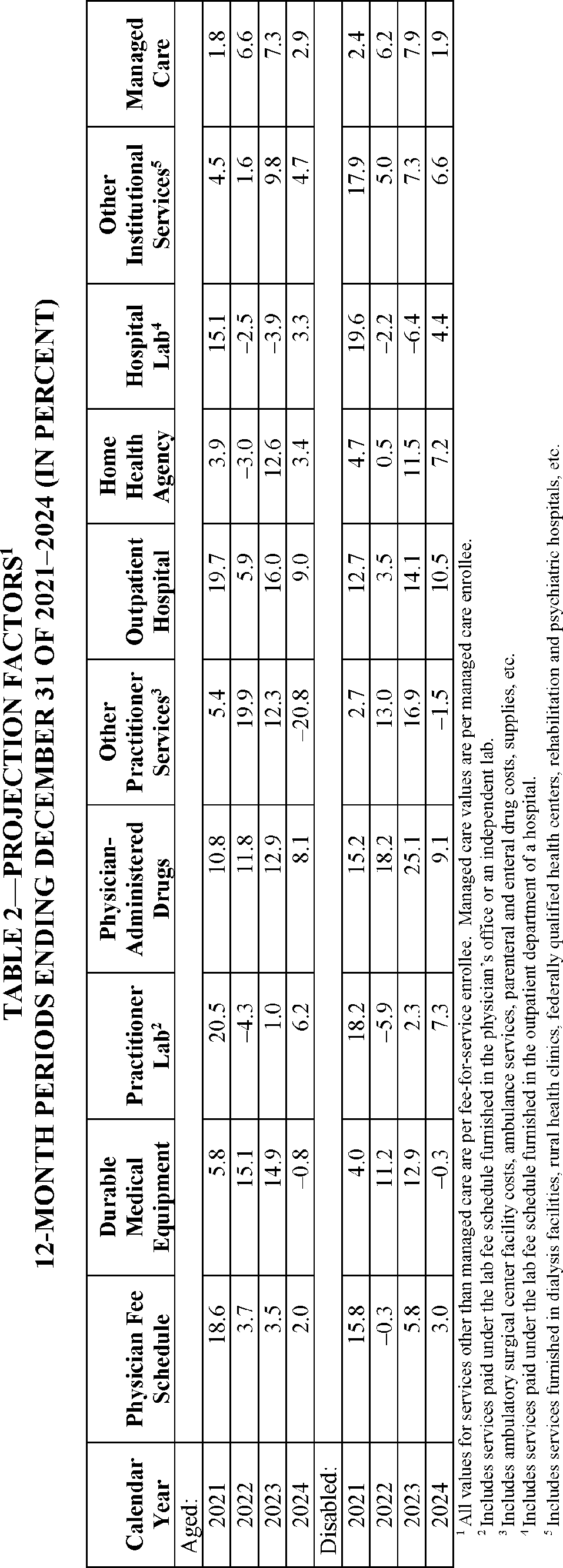

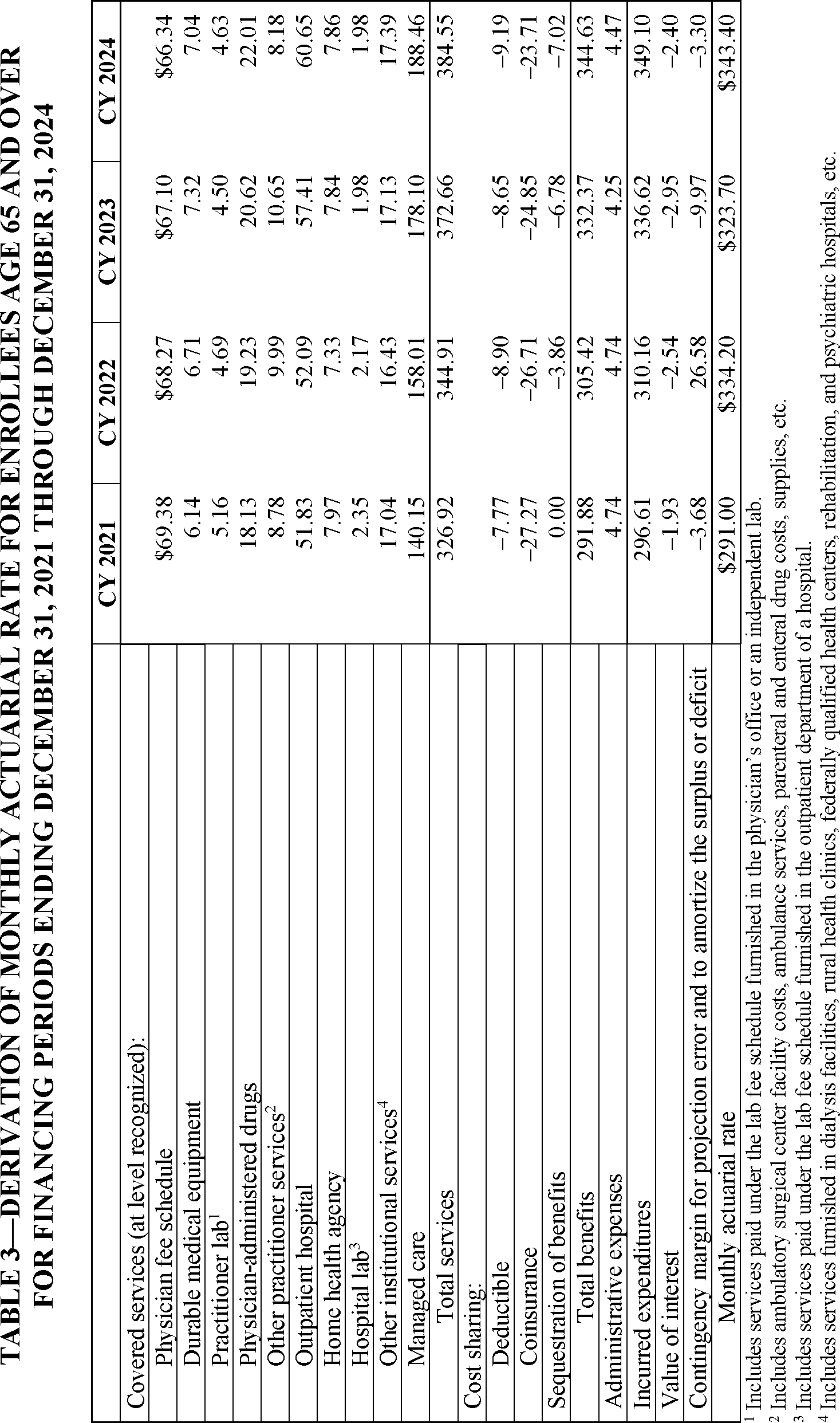

The monthly actuarial rate for enrollees age 65 and older for 2024 is determined by first establishing per enrollee costs by type of service from program data through 2021 and then projecting these costs for subsequent years. The projection factors used for financing periods from January 1, 2021 through December 31, 2024 are shown in Table 2.

As indicated in Table 3, the projected per enrollee amount required to pay for one-half of the total of benefits and administrative costs for enrollees age 65 and over for 2024 is $349.10. Based on current estimates, the assets at the end of 2023 are sufficient to cover the amount of incurred, but unpaid, expenses, to provide for substantial variation between actual and projected costs. Thus, a negative contingency margin can be included to decrease assets to a more appropriate level. The monthly actuarial rate of $343.40 provides an adjustment of −$3.30 for a contingency margin and −$2.40 for interest earnings.

The contingency margin for 2024 is affected by several factors. Additional payments to 340B drug providers from Part B are expected as a result of a judicial remand order. In the unique context of a pending rulemaking on remand from a court, we anticipate that additional 340B payments will reduce the surplus in 2024, resulting in a higher contingency margin. We also anticipate that, should we finalize proposed payment decreases in future years to providers, that would result in correspondingly lower Part B financing rates in those years. Another factor affecting Part B costs is the broader coverage for certain newly-approved drugs that treat Alzheimer's disease starting in July 2023. The broader coverage of these drugs results in a somewhat higher contingency margin. The Part B projected program costs were developed based on these assumptions and were included in the margin development.

In addition, starting in 2011, manufacturers and importers of brand-name prescription drugs pay a fee that is allocated to the Part B account of the SMI trust fund. For 2024, the total of these brand-name drug fees is estimated to be $2.8 billion. The contingency margin for 2024 has been reduced to account for this additional revenue.

The traditional goal for the Part B reserve has been that assets minus liabilities at the end of a year should represent between 15 and 20 percent of the following year's total incurred expenditures. To accomplish this goal, a 17-percent reserve ratio, which is a fully adequate contingency reserve level, has been the normal target used to calculate the Part B premium. At the end of 2023, the reserve ratio is expected to be 25.3 percent. When the reserve ratio is considerably higher than 20 percent, the typical approach in the premium determination is to target a gradual reduction in the reserve ratio to 20 percent over a number of years. The Secretary, who determines the Part B premium each year under section 1839 of the Act, directed the Office of the Actuary to use a 2024 premium increase of 5.9 percent, which targets a reserve ratio for the Part B premium determination of 22.6 percent by the end of 2024.

The actuarial rate of $343.40 per month for aged beneficiaries, as announced in this notice for 2024, reflects the combined effect of the factors and legislation previously described and the projected assumptions listed in Table 2.

3. Monthly Actuarial Rate for Disabled Enrollees

Disabled enrollees are those persons under age 65 who are enrolled in Part B because of entitlement to Social Security disability benefits for more than 24 months or because of entitlement to Medicare under the end-stage renal disease (ESRD) program. Projected monthly costs for disabled enrollees (other than those with ESRD) are prepared in a manner parallel to the projection for the aged using Start Printed Page 71561 appropriate actuarial assumptions (see Table 2). Costs for the ESRD program are projected differently because of the different nature of services offered by the program.

As shown in Table 4, the projected per enrollee amount required to pay for one-half of the total of benefits and administrative costs for disabled enrollees for 2024 is $436.36. The monthly actuarial rate of $427.20 also provides an adjustment of −$2.39 for interest earnings and −$6.77 for a contingency margin, reflecting the same factors and legislation described previously for the aged actuarial rate at magnitudes applicable to the disabled rate determination. Based on current estimates, the assets associated with the disabled Medicare beneficiaries at the end of 2023 are sufficient to cover the amount of incurred, but unpaid, expenses and to provide for a significant degree of variation between actual and projected costs.

The actuarial rate of $427.20 per month for disabled beneficiaries, as announced in this notice for 2024, reflects the combined net effect of the factors and legislation described previously for aged beneficiaries and the projection assumptions listed in Table 2.

4. Sensitivity Testing

Several factors contribute to uncertainty about future trends in medical care costs. It is appropriate to test the adequacy of the rates using alternative cost growth rate assumptions, the results of which are shown in Table 5. One set represents increases that are higher and, therefore, more pessimistic than the current estimate, and the other set represents increases that are lower and, therefore, more optimistic than the current estimate. The values for the alternative assumptions were determined from a statistical analysis of the historical variation in the respective increase factors.

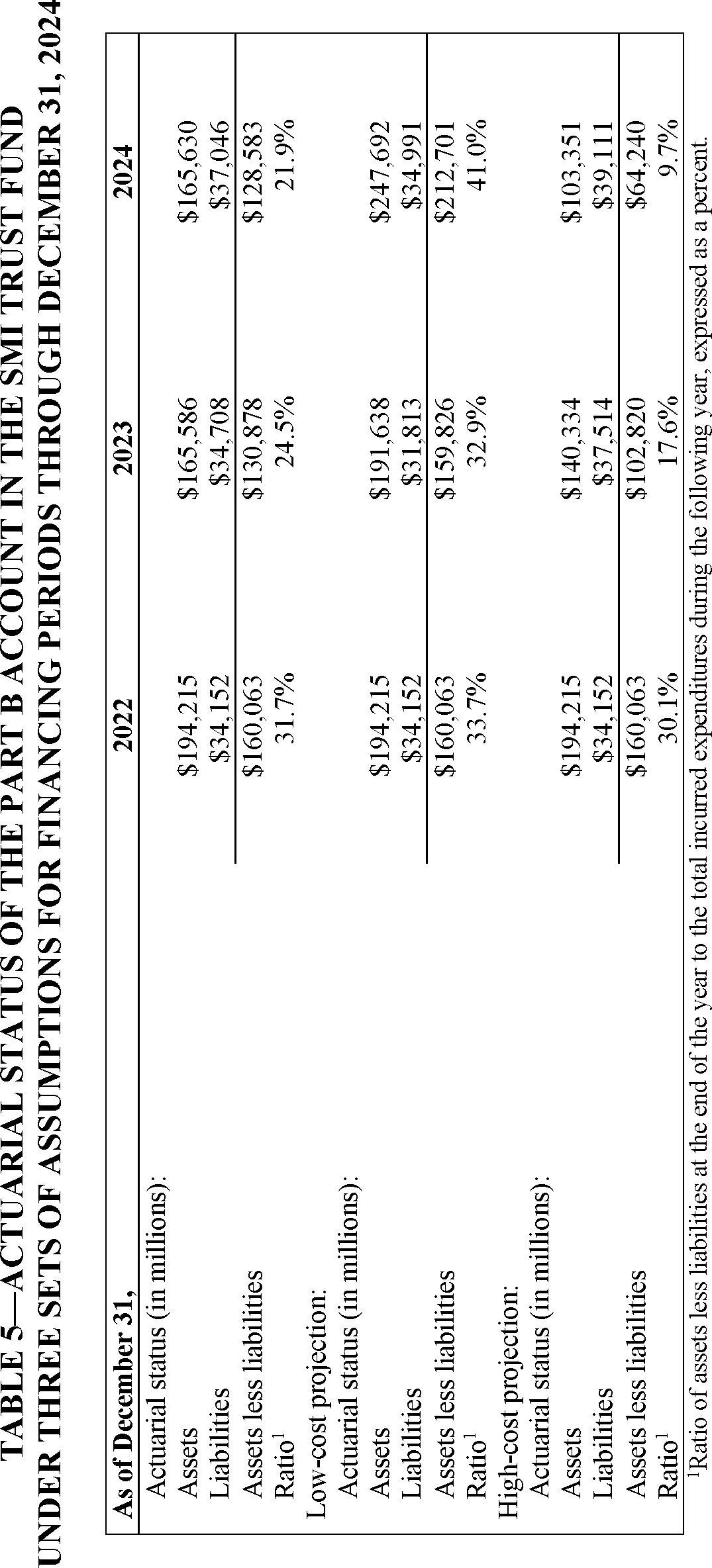

As indicated in Table 5, the monthly actuarial rates would result in an excess of assets over liabilities of $128,583 million by the end of December 2024 under the cost growth rate assumptions shown in Table 2 and under the assumption that the provisions of current law are fully implemented. This result amounts to 21.9 percent of the estimated total incurred expenditures for the following year.

Assumptions that are somewhat more pessimistic (and that therefore test the adequacy of the assets to accommodate projection errors) produce a surplus of $64,240 million by the end of December 2024 under current law, which amounts to 9.7 percent of the estimated total incurred expenditures for the following year. Under fairly optimistic assumptions, the monthly actuarial rates would result in a surplus of $212,701 million by the end of December 2024, or 41.0 percent of the estimated total incurred expenditures for the following year.

The sensitivity analysis indicates that, in a typical year, the premium and general revenue financing established for 2024, together with existing Part B account assets, would be adequate to cover estimated Part B costs for 2024 under current law, should actual costs prove to be somewhat greater than expected.

5. Premium Rates and Deductible

As determined in accordance with section 1839 of the Act, the following are the 2024 Part B monthly premium rates to be paid by (or on behalf of) beneficiaries with full Part B coverage who file either individual tax returns (and are single individuals, heads of households, qualifying widows or widowers with dependent children, or married individuals filing separately who lived apart from their spouses for the entire taxable year) or joint tax returns.

For beneficiaries with immunosuppressive drug only Part B coverage who file either individual tax returns (and are single individuals, heads of households, qualifying widows or widowers with dependent children, or married individuals filing separately who lived apart from their spouses for the entire taxable year) or joint tax returns, the 2024 Part B monthly premium rates are shown below.

Start Printed Page 71562

In addition, the monthly premium rates to be paid by (or on behalf of) beneficiaries with full Part B coverage who are married and lived with their spouses at any time during the taxable year, but who file separate tax returns from their spouses, are as follows:

The monthly premium rates to be paid by (or on behalf of) beneficiaries with immunosuppressive drug only Part B coverage who are married and lived with their spouses at any time during the taxable year, but who file separate tax returns from their spouses, are as follows:

The Part B annual deductible for 2024 is $240.00 for all beneficiaries.

Start Printed Page 71563

Start Printed Page 71564

Start Printed Page 71565

Start Printed Page 71566

III. Collection of Information Requirements

This document does not impose information collection requirements—that is, reporting, recordkeeping, or third-party disclosure requirements. Consequently, there is no need for review by the Office of Management and Budget under the authority of the Paperwork Reduction Act of 1995 (44 U.S.C. 3501 et seq.).

IV. Regulatory Impact Analysis

A. Statement of Need

This notice announces the monthly actuarial rates and premium rates, as required by section 1839(a) of the Act, and the annual deductible, as required by section 1833(b) of the Act, for beneficiaries enrolled in Part B of the Medicare Supplementary Medical Insurance (SMI) program beginning January 1, 2024. It also responds to section 1839(a)(1) of the Act, which requires the Secretary to provide for Start Printed Page 71567 publication of these amounts in the Federal Register during the September that precedes the start of each calendar year. As section 1839 prescribes a detailed methodology for calculating these amounts, we do not have the discretion to adopt an alternative approach on these issues.

B. Overall Impact

We have examined the impact of this notice as required by Executive Order 12866 on Regulatory Planning and Review (September 30, 1993), Executive Order 13563 on Improving Regulation and Regulatory Review (January 18, 2011), Executive Order 14094 entitled “Modernizing Regulatory Review” (April 6, 2023), the Regulatory Flexibility Act (RFA) (September 19, 1980, Pub. L. 96–354), section 1102(b) of the Social Security Act, section 202 of the Unfunded Mandates Reform Act of 1995 (March 22, 1995; Pub. L. 104–4), Executive Order 13132 on Federalism (August 4, 1999), and the Congressional Review Act (5 U.S.C. 804(2)).

Executive Orders 12866 and 13563 direct agencies to assess all costs and benefits of available regulatory alternatives and, if regulation is necessary, to select regulatory approaches that maximize net benefits (including potential economic, environmental, public health and safety effects, distributive impacts, and equity). The Executive Order 14094 entitled “Modernizing Regulatory Review” (hereinafter, the Modernizing E.O.) amends section 3(f)(1) of Executive Order 12866 (Regulatory Planning and Review). The amended section 3(f) of Executive Order 12866 defines a “significant regulatory action” as an action that is likely to result in a notice/rule: (1) having an annual effect on the economy of $200 million or more in any one year (adjusted every 3 years by the Administrator of OIRA for changes in gross domestic product), or adversely affect in a material way the economy, a sector of the economy, productivity, competition, jobs, the environment, public health or safety, or State, local, territorial, or tribal governments or communities; (2) creating a serious inconsistency or otherwise interfering with an action taken or planned by another agency; (3) materially altering the budgetary impacts of entitlement grants, user fees, or loan programs or the rights and obligations of recipients thereof; or (4) raise legal or policy issues for which centralized review would meaningfully further the President's priorities, or the principles set forth in the Executive Order, as specifically authorized in a timely manner by the Administrator of OIRA in each case.

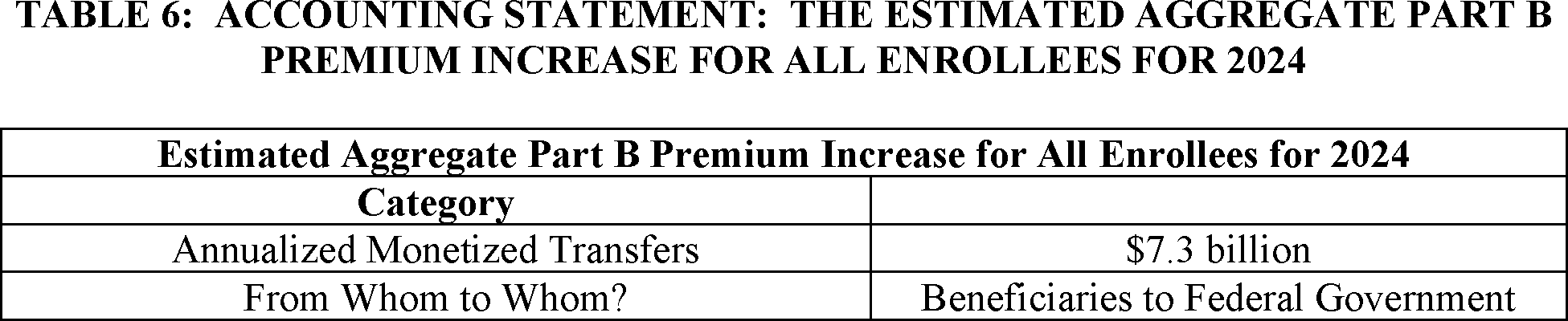

A regulatory impact analysis (RIA) must be prepared for major rules with significant regulatory action/s and/or with significant effects as per section 3(f)(1) ($200 million or more in any one year). Based on our estimates, OMB's Office of Information and Regulatory Affairs has determined this rulemaking is significant per section 3(f)(1) as measured by the $200 million threshold or more in any one year, and hence also a major rule under Subtitle E of the Small Business Regulatory Enforcement Fairness Act of 1996 (also known as the Congressional Review Act). The 2024 standard Part B premium of $174.70 is $9.80 higher than the 2023 premium of $164.90. We estimate that the total premium increase, for the approximately 62 million Part B enrollees in 2024, will be $7.3 billion, which is an annual effect on the economy of $200 million or more. Accordingly, we have prepared a Regulatory Impact Analysis that to the best of our ability presents the costs and benefits of the rulemaking. Therefore, OMB has reviewed these proposed regulations, and the Departments have provided the following assessment of their impact.

C. Detailed Economic Analysis

As discussed earlier, this notice announces that the monthly actuarial rates applicable for 2024 are $343.40 for enrollees age 65 and over and $427.20 for disabled enrollees under age 65. It also announces the 2024 monthly Part B premium rates to be paid by (or on behalf of) beneficiaries with full Part B coverage who file either individual tax returns (and are single individuals, heads of households, qualifying widows or widowers with dependent children, or married individuals filing separately who lived apart from their spouses for the entire taxable year) or joint tax returns.

For beneficiaries with immunosuppressive drug only Part B coverage, who file either individual tax returns (and are single individuals, heads of households, qualifying widows or widowers with dependent children, or married individuals filing separately who lived apart from their spouses for the entire taxable year) or joint tax returns, the 2024 Part B monthly premium rates are announced and shown below.

Start Printed Page 71568

In addition, the monthly premium rates to be paid by (or on behalf of) beneficiaries with full Part B coverage who are married and lived with their spouses at any time during the taxable year, but who file separate tax returns from their spouses, are also announced and listed in the following table:

The monthly premium rates to be paid by (or on behalf of) beneficiaries with immunosuppressive drug only Part B coverage who are married and lived with their spouses at any time during the taxable year, but who file separate tax returns from their spouses, are announced and listed in the following table:

D. Accounting Statement and Table

As required by OMB Circular A–4 (available at www.whitehouse.gov/sites/whitehouse.gov/files/omb/circulars/A4/a-4.pdf), in Table 6 we have prepared an accounting statement showing the estimated aggregate Part B premium increase for all enrollees in 2024.

E. Regulatory Flexibility Act (RFA)

The RFA requires agencies to analyze options for regulatory relief of small businesses, if a rule or other regulatory document has a significant impact on a substantial number of small entities. For purposes of the RFA, small entities include small businesses, nonprofit organizations, and small governmental jurisdictions. Individuals and States are not included in the definition of a small entity. This notice announces the monthly actuarial rates for aged (age 65 and over) and disabled (under 65) beneficiaries enrolled in Part B of the Medicare SMI program beginning January 1, 2024. Also, this notice announces the monthly premium for aged and disabled beneficiaries as well as the income-related monthly adjustment amounts to be paid by beneficiaries with modified adjusted Start Printed Page 71569 gross income above certain threshold amounts. As a result, we are not preparing an analysis for the RFA because the Secretary has determined that this notice will not have a significant economic impact on a substantial number of small entities.

In addition, section 1102(b) of the Act requires us to prepare a regulatory impact analysis if a rule or other regulatory document may have a significant impact on the operations of a substantial number of small rural hospitals. This analysis must conform to the provisions of section 604 of the RFA. For purposes of section 1102(b) of the Act, we define a small rural hospital as a hospital that is located outside of a Metropolitan Statistical Area and has fewer than 100 beds. As we discussed previously, we are not preparing an analysis for section 1102(b) of the Act because the Secretary has determined that this notice will not have a significant effect on a substantial number of small rural hospitals.

Section 202 of the Unfunded Mandates Reform Act of 1995 (UMRA) also requires that agencies assess anticipated costs and benefits before issuing any rule whose mandates require spending in any one year of $100 million in 1995 dollars, updated annually for inflation. In 2023, that threshold is approximately $177 million. Part B enrollees who are also enrolled in Medicaid have their monthly Part B premiums paid by Medicaid. The cost to each State Medicaid program from the 2024 premium increase is estimated to be more than the threshold. This notice does not impose mandates that will have a consequential effect of the threshold amount or more on State, local, or tribal governments or on the private sector.

Executive Order 13132 establishes certain requirements that an agency must meet when it publishes a proposed rule or other regulatory document (and subsequent final rule or other regulatory document) that imposes substantial direct compliance costs on State and local governments, preempts State law, or otherwise has Federalism implications. We have determined that this notice does not significantly affect the rights, roles, and responsibilities of States. Accordingly, the requirements of Executive Order 13132 do not apply to this notice.

In accordance with the provisions of Executive Order 12866, this notice was reviewed by the Office of Management and Budget.

V. Waiver of Proposed Rulemaking

We ordinarily publish a notice of proposed rulemaking in the Federal Register and invite public comment prior to a rule taking effect in accordance with section 1871 of the Act and section 553(b) of the Administrative Procedure Act (APA). Section 1871(a)(2) of the Act provides that no rule, requirement, or other statement of policy (other than a national coverage determination) that establishes or changes a substantive legal standard governing the scope of benefits, the payment for services, or the eligibility of individuals, entities, or organizations to furnish or receive services or benefits under Medicare shall take effect unless it is promulgated through notice and comment rulemaking. Unless there is a statutory exception, section 1871(b)(1) of the Act generally requires the Secretary of the Department of Health and Human Services (the Secretary) to provide for notice of a proposed rule in the Federal Register and provide a period of not less than 60 days for public comment before establishing or changing a substantive legal standard regarding the matters enumerated by the statute. Similarly, under 5 U.S.C. 553(b) of the APA, the agency is required to publish a notice of proposed rulemaking in the Federal Register before a substantive rule takes effect. Section 553(d) of the APA and section 1871(e)(1)(B)(i) of the Act usually require a 30-day delay in effective date after issuance or publication of a rule, subject to exceptions. Sections 553(b)(B) and 553(d)(3) of the APA provide for exceptions from the advance notice and comment requirement and the delay in effective date requirements. Sections 1871(b)(2)(C) and 1871(e)(1)(B)(ii) of the Act also provide exceptions from the notice and 60-day comment period and the 30-day delay in effective date. Section 553(b)(B) of the APA and section 1871(b)(2)(C) of the Act expressly authorize an agency to dispense with notice and comment rulemaking for good cause if the agency makes a finding that notice and comment procedures are impracticable, unnecessary, or contrary to the public interest.

The annual updated amounts for the Part B monthly actuarial rates for aged and disabled beneficiaries, the Part B premium, and the Part B deductible set forth in this notice do not establish or change a substantive legal standard regarding the matters enumerated by the statute or constitute a substantive rule that would be subject to the notice requirements in section 553(b) of the APA. However, to the extent that an opportunity for public notice and comment could be construed as required for this notice, we find good cause to waive this requirement.

Section 1839 of the Act requires the Secretary to determine the monthly actuarial rates for aged and disabled beneficiaries, as well as the monthly Part B premium (including the income-related monthly adjustment amounts to be paid by beneficiaries with modified adjusted gross income above certain threshold amounts), for each calendar year in accordance with the statutory formulae, in September preceding the year to which they will apply. Further, the statute requires that the agency promulgate the Part B premium amount, in September preceding the year to which it will apply, and include a public statement setting forth the actuarial assumptions and bases employed by the Secretary in arriving at the amount of an adequate actuarial rate for enrollees age 65 and older. We include the Part B annual deductible, which is established in accordance with a specific formula described in section 1833(b) of the Act, because the determination of the amount is directly linked to the rate of increase in actuarial rate under section 1839(a)(1) of the Act. We have calculated the monthly actuarial rates for aged and disabled beneficiaries, the Part B deductible, and the monthly Part B premium as directed by the statute; since the statute establishes both when the monthly actuarial rates for aged and disabled beneficiaries and the monthly Part B premium must be published and the information that the Secretary must factor into those amounts, we do not have any discretion in that regard. We find notice and comment procedures to be unnecessary for this notice, and we find good cause to waive such procedures under section 553(b)(B) of the APA and section 1871(b)(2)(C) of the Act, if such procedures may be construed to be required at all. Through this notice, we are simply notifying the public of the updates to the monthly actuarial rates for aged and disabled beneficiaries and the Part B deductible, as well as the monthly Part B premium amounts and the income-related monthly adjustment amounts to be paid by certain beneficiaries, in accordance with the statute, for CY 2024. As such, we also note that even if notice and comment procedures were required for this notice, we would find good cause, for the previously stated reason, to waive the delay in effective date of the notice, as additional delay would be contrary to the public interest under section 1871(e)(1)(B)(ii) of the Act. Start Printed Page 71570 Publication of this notice is consistent with section 1839 of the Act, and we believe that any potential delay in the effective date of the notice, if such delay were required at all, could cause unnecessary confusion for both the agency and Medicare beneficiaries.

Chiquita Brooks-LaSure, Administrator of the Centers for Medicare & Medicaid Services, approved this document on October 11, 2023.

Start SignatureEnd Signature End Supplemental InformationDated: October 11, 2023.

Xavier Becerra,

Secretary, Department of Health and Human Services.

BILLING CODE 4120–01–P

BILLING CODE 4120–01–C

BILLING CODE 4120–01–P

BILLING CODE 4120–01–C

BILLING CODE 4120–01–P

BILLING CODE 4120–01–C

[FR Doc. 2023–22823 Filed 10–12–23; 4:15 pm]

BILLING CODE 4120–01–P

Document Information

- Effective Date:

- 1/1/2024

- Published:

- 10/17/2023

- Department:

- Centers for Medicare & Medicaid Services

- Entry Type:

- Notice

- Action:

- Notice.

- Document Number:

- 2023-22823

- Dates:

- The monthly actuarial rates are effective on January 1, 2024.

- Pages:

- 71555-71570 (16 pages)

- Docket Numbers:

- CMS-8085-N

- RINs:

- 0938-AV13: Medicare Part B Monthly Actuarial Rates, Premium Rates, and Annual Deductible Beginning January 1, 2024 (CMS-8085)

- RIN Links:

- https://www.federalregister.gov/regulations/0938-AV13/medicare-part-b-monthly-actuarial-rates-premium-rates-and-annual-deductible-beginning-january-1-2024

- PDF File:

- 2023-22823.pdf