-

Start Preamble

Start Printed Page 16426

AGENCY:

Office of Postsecondary Education, Department of Education.

ACTION:

Notice of proposed rulemaking.

SUMMARY:

The Secretary proposes to amend the regulations on institutional eligibility under the Higher Education Act of 1965, as amended (HEA), and the Student Assistance General Provisions to establish measures for determining whether certain postsecondary educational programs prepare students for gainful employment in a recognized occupation, and the conditions under which these educational programs remain eligible under the Federal Student Aid programs authorized under title IV of the HEA (title IV, HEA programs).

DATES:

We must receive your comments on or before May 27, 2014.

ADDRESSES:

Submit your comments through the Federal eRulemaking Portal or via postal mail, commercial delivery, or hand delivery. We will not accept comments by fax or by email or those submitted after the comment period. To ensure that we do not receive duplicate copies, please submit your comments only once. In addition, please include the Docket ID at the top of your comments.

- Federal eRulemaking Portal: Go to www.regulations.gov to submit your comments electronically. Information on using Regulations.gov, including instructions for accessing agency documents, submitting comments, and viewing the docket, is available on the site under “Are you new to the site?”

- Postal Mail, Commercial Delivery, or Hand Delivery: The Department strongly encourages commenters to submit their comments electronically. However, if you mail or deliver your comments about the proposed regulations, address them to Ashley Higgins, U.S. Department of Education, 1990 K Street NW., room 8037, Washington, DC 20006-8502.

Privacy Note: The Department's policy is to make all comments received from members of the public available for public viewing in their entirety on the Federal eRulemaking Portal at www.regulations.gov. Therefore, commenters should be careful to include in their comments only information that they wish to make publicly available.

Start Further InfoFOR FURTHER INFORMATION CONTACT:

John Kolotos, U.S. Department of Education, 1990 K Street NW., Room 8018, Washington, DC 20006-8502. Telephone: (202) 502-7762 or by email: gainfulemploymentregulations@ed.gov.

If you use a telecommunications device for the deaf (TDD) or a text telephone (TTY), call the Federal Relay Service (FRS), toll free, at 1-800-877-8339.

End Further Info End Preamble Start Supplemental InformationSUPPLEMENTARY INFORMATION:

Executive Summary:

Purpose of This Regulatory Action: As discussed in more detail under “§ 668.401 Scope and purpose,” the proposed regulations are intended to address growing concerns about educational programs that, as a condition of eligibility for title IV, HEA program funds, are required by statute to provide training that prepares students for gainful employment in a recognized occupation (GE programs), but instead are leaving students with unaffordable levels of loan debt in relation to their earnings, or leading to default. GE programs include nearly all educational programs at for-profit institutions of higher education, as well as non-degree programs at public and private non-profit institutions such as community colleges.

Specifically, the Department is concerned that a number of GE programs: (1) Do not train students in the skills they need to obtain and maintain jobs in the occupation for which the program purports to provide training, (2) provide training for an occupation for which low wages do not justify program costs, and (3) are experiencing a high number of withdrawals or “churn” because relatively large numbers of students enroll but few, or none, complete the program, which can often lead to default. We are also concerned about the growing evidence, from Federal and State investigations and qui tam lawsuits, that many GE programs are engaging in aggressive and deceptive marketing and recruiting practices. As a result of these practices, prospective students and their families are potentially being pressured and misled into critical decisions regarding their educational investments that are against their interests.

For these reasons, through this regulatory action, the Department seeks to establish: (1) An accountability framework for GE programs that will define what it means to prepare students for gainful employment in a recognized occupation by establishing measures by which the Department would evaluate whether a GE program remains eligible for title IV, HEA program funds, and (2) a transparency framework that would increase the quality and availability of information about the outcomes of students enrolled in GE programs. Better outcomes information would benefit: students, prospective students, and their families, as they make critical decisions about their educational investments; the public, taxpayers, and the Government, by providing information that would enable better protection of the Federal investment in these programs; and institutions, by providing them with meaningful information that they could use to help improve student outcomes in their programs.

The accountability framework is designed to define what it means to prepare students for gainful employment by establishing measures that would assess whether programs provide quality education and training to their students that lead to earnings that will allow students to pay back their student loan debts. For programs that perform poorly under the measures, institutions would need to make improvements in the initial years of the rule, or lose program eligibility for title IV, HEA program funds. For programs that are not among the very worst, but nonetheless do not have outcomes that meet minimum acceptable levels of performance, institutions would be required to make improvements after the regulations become effective to avoid losing eligibility, but would be given a relatively greater amount of time to do so.

The transparency framework is designed to establish reporting and disclosure requirements that would increase the transparency of student outcomes of GE programs so that information is disseminated to students, prospective students, and their families that is accurate and comparable and could help them make better informed decisions about where to invest their time and money in pursuit of a postsecondary degree or credential. Further, this information would provide the public, taxpayers, and the Government with relevant information to better safeguard the Federal investment in these programs. Finally, the transparency framework would provide institutions with meaningful information that they could use to improve student outcomes in these programs.

Authority for This Regulatory Action:

To accomplish these two primary goals of accountability and transparency, the Secretary proposes to amend parts 600 and 668 of title 34 of the Code of Federal Regulations (CFR). Start Printed Page 16427The Department's authority for this regulatory action is derived primarily from three sources, which are discussed in more detail in “§ 668.401 Scope and purpose” and “§ 668.403 Gainful employment framework.” First, sections 101 and 102 of the HEA define an eligible institution, as pertinent here, as one that provides an “eligible program of training to prepare students for gainful employment in a recognized occupation.” 20 U.S.C. 1001(b)(1), 1002(b)(1)(A)(i), (c)(1)(A). Section 481(b) of the HEA defines “eligible program” to include a program that “provides a program of training to prepare students for gainful employment in a recognized profession.” 20 U.S.C. 1088(b). Briefly, this authority establishes the requirement that the educational programs that are eligible for title IV, HEA program funds under these sections must provide training to prepare students for gainful employment in a recognized occupation—the requirement that the Department seeks to define through the proposed regulations.

Second, section 410 of the General Education Provisions Act provides the Secretary with authority to make, promulgate, issue, rescind, and amend rules and regulations governing the manner of operations of, and governing the applicable programs administered by, the Department. 20 U.S.C. 1221e-3. Furthermore, under section 414 of the Department of Education Organization Act, the Secretary is authorized to prescribe such rules and regulations as the Secretary determines necessary or appropriate to administer and manage the functions of the Secretary or the Department. 20 U.S.C. 3474. These authorities thus include promulgating regulations that, in this case: set measures to determine the eligibility of GE programs for title IV, HEA program funds; require institutions to report information about the program to the Secretary; and require the institution to disclose information about the program to students, prospective students, and their families, the public, taxpayers, and the Government, and institutions.

As also explained in more detail in “§ 668.401 Scope and purpose,” the Department's authority for the transparency framework is further supported by section 431 of the Department of Education Organization Act, which provides authority to the Secretary, in relevant part, to inform the public regarding federally supported education programs; and collect data and information on applicable programs for the purpose of obtaining objective measurements of the effectiveness of such programs in achieving the intended purposes of such programs. 20 U.S.C. 1231a.

The Department's authority for the proposed regulations is also informed by the legislative history of these provisions, as discussed in “§ 668.403 Gainful employment framework,” as well as the rulings of the U.S. District Court for the District of Columbia in Association of Private Sector Colleges and Universities v. Duncan, 870 F.Supp.2d 133 (D.D.C. 2012), and 930 F.Supp.2d 210 (D.D.C. 2013). Notably, the court specifically considered the Department's authority to define what it means to prepare students for gainful employment and to require institutions to report and disclose relevant information about their GE programs.

Summary of the Major Provisions of This Regulatory Action:

As discussed under “Purpose of This Regulatory Action,” the proposed regulations would establish an accountability framework and a transparency framework.

The accountability framework would, among other things, create a certification process by which an institution would establish a GE program's eligibility for title IV, HEA program funds, as well as a process by which the Department would determine whether a program remains eligible. First, an institution would establish the eligibility of a GE program by certifying that the program is included in the institution's accreditation and satisfies any applicable State or Federal program-level accrediting and licensing requirements for the occupations for which the program purports to prepare students to enter. This requirement would serve as a baseline protection against the harm that students could experience by enrolling in programs that do not meet all State or Federal accrediting standards and licensing requirements necessary to secure the jobs associated with the training.

Under the accountability framework, we also propose two complementary yet independent measures—the debt-to-earnings (D/E) rates measure and the program cohort default rate (pCDR) measure—that would be used to determine whether a GE program remains eligible for title IV, HEA program funds.

The D/E rates measure would evaluate the amount of debt students who completed a GE program incurred to attend that program in comparison to those same students' discretionary and annual earnings after completing the program. The proposed regulations would establish the standards by which the program would be assessed to determine, for each year rates are calculated, whether it passes or fails the D/E rates measure or is “in the zone.” Under the proposed regulations, to pass the D/E rates measure, the GE program must have a discretionary income rate less than or equal to 20 percent or an annual earnings rate less than or equal to 8 percent. The proposed regulations would also establish a zone for GE programs that have a discretionary income rate between 20 percent and 30 percent or an annual earnings rate between 8 percent and 12 percent. GE programs with a discretionary income rate over 30 percent and an annual earnings rate over 12 percent would fail the D/E rates measure. Under the proposed regulations, a GE program would become ineligible for title IV, HEA program funds, if it fails the D/E rates measure for two out of three consecutive years, or has a combination of D/E rates measures that are in the zone or failing for four consecutive years. We propose the D/E rates measure and the thresholds, as explained in more detail in “§ 668.403 Gainful employment framework,” to assess whether a GE program has indeed prepared students to earn enough to repay their loans, or was sufficiently low cost, such that students are not unduly burdened with debt, and to better safeguard the Federal investment in the program.

In addition to the D/E rates measure, the proposed regulations would establish a pCDR measure. The pCDR measure would evaluate the default rate of former students enrolled in a GE program, regardless of whether they completed the program. Under the proposed regulations, a program would lose eligibility if its GE program has a pCDR of 30 percent or greater for three consecutive fiscal years. We propose the pCDR measure and the thresholds, as explained in more detail in “§ 668.403 Gainful employment framework,” to identify those programs that may pass, or may not be evaluated by, the D/E rates measure, but whose students incur debt they cannot repay and ultimately default on their loans. Unlike the D/E rates measure, the pCDR measure would include students who did not complete their programs and therefore could disqualify programs with low completion rates that, regardless of the earnings of students who complete the program, leave a significant number of students without credentials and with unmanageable debt.

The proposed regulations would also establish procedures for the calculation of the D/E rates and pCDR measures, as well as a process for challenging the information used to calculate the D/E rates and pCDR measures and appealing Start Printed Page 16428those determinations. For the D/E rates measure, the proposed regulations also would establish a transition period for the first four years of the rule to allow institutions an opportunity to pass the D/E rates measure by taking immediate steps to improve otherwise failing GE programs by reducing the loan debt of currently enrolled students.

For a GE program that could become ineligible in an immediately succeeding year, based on the program's performance in prior years, the proposed regulations would require the GE program to warn students and prospective students of the potential loss of eligibility for title IV, HEA program funds, as well as the implications of such loss. Specifically, institutions would be required to provide written warnings to students that describe the options available to continue their education at the institution, or at another institution, in the event that the program loses its eligibility and whether the students will be able to receive a refund of tuition and fees. The proposed regulations also provide that, for a GE program that loses eligibility for title IV, HEA program funds, as well as any failing or zone program that is discontinued by the institution, the loss of eligibility is for three calendar years.

Through these provisions, we intend to: Ensure that, in the initial few years after the proposed regulations become effective, institutions would have a meaningful opportunity and reasonable time to improve their programs and to ensure that those improvements would be reflected in the D/E rates; protect students and prospective students and ensure that they are informed about programs that are failing or could potentially lose eligibility; and provide institutions and other interested parties with clarity as to how the calculations would be made, the opportunities institutions would have to ensure the information used in the calculations is accurate, and the consequences of failing a measure and losing eligibility.

In addition to the accountability framework, the proposed regulations would establish a transparency framework. First, the proposed regulations would establish reporting requirements, under which institutions would report information related to their GE programs to the Secretary. The reporting requirements would both facilitate the Department's evaluation of the GE programs under the accountability framework, as well as support the goals of the transparency framework. Second, the proposed regulations would require institutions to disclose relevant information and data about the GE programs through a disclosure template developed by the Secretary. The proposed disclosure requirements would help ensure students, prospective students, and their families, the public, taxpayers, and the Government, and institutions have access to meaningful and comparable information related to student outcomes and overall performance of GE programs.

Costs and Benefits:

There would be two primary benefits of the proposed regulations. Because the proposed regulations would establish an accountability framework that assesses program performance we would expect students, prospective students, taxpayers, and the Federal Government to receive a better return on money spent on education. The proposed regulations would also establish a transparency framework designed to improve market information that would assist students, prospective students, and their families in making critical decisions about their educational investment and in understanding potential outcomes of that investment. The public, taxpayers, the Government, and institutions would also gain relevant and useful information about GE programs, allowing them to better evaluate their investment in these programs. Institutions would largely bear the costs of the proposed regulations, which would fall into two categories: paperwork costs associated with institutions complying with the proposed regulations, and other costs that could be incurred by institutions if they attempt to improve their GE programs and due to changing student enrollment. In addition, if programs that provided valuable education to students shut down as a result of the proposed regulations, then the foregone value of that service would be another cost to society. See “Discussion of Costs, Benefits, and Transfers” in the regulatory impact analysis in Appendix A to this document for a more complete discussion of the costs and benefits of the proposed regulations.

Invitation to Comment: We invite you to submit comments regarding the proposed regulations. To ensure that your comments have maximum effect in developing the final regulations, we urge you to identify clearly the specific section or sections of the proposed regulations that each of your comments addresses, and provide relevant information and data whenever possible, even when there is no specific solicitation of data and other supporting materials in the request for comment. Please do not submit comments outside the scope of the specific proposals in this notice of proposed rulemaking. We will not respond to comments that do not specifically relate to the proposed regulations. See “ADDRESSES” for instructions on how to submit comments.

We invite you to assist us in complying with the specific requirements of Executive Orders 12866 and 13563 and their overall requirement of reducing regulatory burden that might result from the proposed regulations. Please let us know of any further ways we could reduce potential costs or increase potential benefits while preserving the effective and efficient administration of the Department's programs and activities.

During and after the comment period, you may inspect all public comments about the proposed regulations by accessing Regulations.gov. You may also inspect the comments in person in room 8037, 1990 K Street NW., Washington, DC, between 8:30 a.m. and 4:00 p.m., Washington, DC time, Monday through Friday of each week except Federal holidays. If you want to schedule time to inspect comments, please contact the person listed under FOR FURTHER INFORMATION CONTACT.

Assistance to Individuals with Disabilities in Reviewing the Rulemaking Record: On request, we will provide an appropriate accommodation or auxiliary aid to an individual with a disability who needs assistance to review the comments or other documents in the public rulemaking record for the proposed regulations. If you want to schedule an appointment for this type of accommodation or auxiliary aid, please contact the person listed under FOR FURTHER INFORMATION CONTACT.

Background of the Proposed Regulations, Public Participation, and Negotiated Rulemaking

Background

The Secretary proposes to amend parts 600 and 668 of title 34 of the CFR. The regulations in 34 CFR part 600 and 668 pertain to institutional eligibility under the HEA and participation in title IV, HEA programs. We propose these amendments to establish measures for determining whether certain postsecondary educational programs prepare students for gainful employment in a recognized occupation and the conditions under which these educational programs remain eligible under the title IV, HEA programs.

Negotiated Rulemaking Requirement

Section 492 of the HEA, 20 U.S.C. 1098a, requires the Secretary, before Start Printed Page 16429publishing any proposed regulations for programs authorized by title IV of the HEA, to obtain public involvement in the development of proposed regulations. After obtaining advice and recommendations from the public, including individuals and representatives of groups involved in the title IV, HEA programs, the Secretary must subject the proposed regulations to a negotiated rulemaking process. If negotiators reach consensus on the proposed regulations, the Department agrees to publish without alteration a defined group of regulations on which the negotiators reached consensus unless the Secretary reopens the process or provides a written explanation to the participants stating why the Secretary has decided to depart from the agreement reached during negotiations. Further information on the negotiated rulemaking process can be found at: http://www2.ed.gov/policy/highered/reg/hearulemaking/hea08/neg-reg-faq.html.

Prior Negotiated Rulemaking

Between November 2009 and January 2010, the Department held three negotiated rulemaking sessions aimed at improving program integrity in the title IV, HEA programs, and that discussed gainful employment and 13 other program integrity topics. As a result of those discussions, during which consensus was not reached on issues related to gainful employment, the Department published three notices of proposed rulemaking (NPRM) related to the topic of gainful employment. Notably, those proposed regulations included two debt measures to determine whether a program provides training that prepares students for gainful employment in a recognized occupation. One measure was based on the Federal student loan repayment rates of students enrolled in the program, and the other measure was based on the debt-to-earnings ratios of students who completed the program.

On October 29, 2010, and June 13, 2011, the Department published final regulations on gainful employment: “Program Integrity: Reporting/Disclosure Requirements for GE Programs”; “Program Integrity: Gainful Employment—New Programs”; and “Gainful Employment: Gainful Employment—Debt Measures” (75 FR 66832; 75 FR 66665; 76 FR 34385). In this document, we refer to those final regulations, when discussing them collectively, as the “2011 Final Rules.” We did not publish final regulations for the NPRM published on September 27, 2011, relating to the application and approval process for new programs that prepare students for gainful employment in a recognized occupation.

Among other things, with respect to the two debt measures for determining whether a program provides training that prepares students for gainful employment in a recognized occupation, the 2011 Final Rules established a maximum debt-to-earnings ratio of 30 percent of discretionary income and 12 percent of annual earnings and a minimum standard of 35 percent for the loan repayment rate.

The chart below summarizes the past NPRMs and 2011 Final Rules.

Date NPRM Date Final rule June 18, 2010 Program Integrity Issues (75 FR 34806) Oct. 29, 2010 Reporting/Disclosure Requirements for GE Programs. Effective on July 1, 2011 (75 FR 66832). July 26, 2010 Gainful Employment (75 FR 43616) Oct. 29, 2010 Gainful Employment—New Programs (75 FR 66665). June 13, 2011 Gainful Employment—Debt Measures (76 FR 34385). Sept. 27, 2011 Application and Approval Process for New Programs (76 FR 59864) (No final rule published). Litigation on the 2011 Final Rules

In July 2011, immediately after the first set of final regulations for gainful employment took effect, the Association of Private Sector Colleges and Universities (APSCU), an industry organization representing for-profit institutions, brought suit against the Department in the U.S. District Court for the District of Columbia challenging, among other things, the debt measures, reporting and disclosure requirements, and new program approval requirements in the 2011 Final Rules. On June 30, 2012, the court struck down most of the 2011 Final Rules, finding that the threshold for the loan repayment measure lacked a reasoned basis. Association of Private Sector Colleges and Universities v. Duncan, 870 F.Supp.2d 133 (D.D.C. 2012). We refer to the case in this document as “APSCU v. Duncan.” Although the court rejected APSCU's argument that the debt-to-earnings measure was not the product of reasoned decision-making, the court nonetheless found that the two debt measures and other provisions of the regulations were so intertwined that the threshold in the loan repayment measure could not be severed from the debt measures and other parts of the regulations. For this reason, the court vacated almost all of the 2011 Final Rules.

Notably, however, the disclosure requirements survived and are still in effect. Under the disclosure requirements, for each GE program, an institution must disclose the occupation that the program prepares students to enter; the on-time graduation rate for students completing the program; the tuition and fees charged; and the placement rate and median loan debt for students completing the program. The court held that the disclosure requirements are within the Department's authority under the HEA and are not arbitrary or capricious.

Additionally, the court noted in its opinion that the Secretary enjoys broad authority to make, promulgate, issue, rescind, and amend the rules and regulations governing the applicable programs administered by the Department and that the Secretary is “authorized to prescribe such rules and regulations as the Secretary determines necessary or appropriate to administer and manage the functions of the Secretary or the Department.” APSCU v. Duncan, 870 F.Supp.2d at 141; see 20 U.S.C. 3474 (2006). Furthermore, in responding to the question of whether the Department's regulatory effort to define gainful employment is within the Department's authority, the court agreed with the Department and concluded that the phrase “gainful employment in a recognized occupation” is ambiguous and that in enacting it Congress delegated interpretive authority to the Department. Id. at 146.

The Department subsequently filed a motion to alter or amend the judgment, Start Printed Page 16430asking the court to reinstate the vacated reporting requirements, as they were required for the Department to comply with its obligations under the provisions relating to the disclosure requirements. The court denied this motion on March 19, 2013.

In its opinion, the court refused to reinstate the reporting requirements for the reason that they required institutions to report to the Department information about students enrolled in GE programs who did not apply for or receive title IV, HEA program funds. The court concluded that the Department was prohibited under section 134 of the HEA, 20 U.S.C. 1015c, from maintaining information about those students in the Department's National Student Loan Data System (NSLDS), as planned. APSCU v. Duncan, 930 F.Supp.2d 210 (D.D.C. 2013). Neither the Department nor APSCU appealed the court's rulings.

As a result of APSCU v. Duncan, certain sections of the 2011 Final Rules were vacated either in whole or in part. For the purpose of this NPRM, when referencing a section that was vacated in part, we treat the entire section as vacated. Throughout this document, we refer to the sections that were vacated or are treated here as vacated as part of the “2011 Prior Rule.” Although the text of these vacated sections remains in the CFR and we refer to them in this document in the present tense, these sections are of no effect. Section 668.6(b) of the 2011 Final Rules, relating to disclosure requirements for GE programs, was not vacated as a result of APSCU v. Duncan. This section remains in effect, and we refer to this section in this document as the “2011 Current Rule.” In discussing the current regulations and proposed regulations under “Significant Proposed Regulations,” we discuss relevant parts of the 2011 Final Rules, but we distinguish between sections that are part of the 2011 Prior Rule and sections that are part of the 2011 Current Rule.

New Negotiated Rulemaking

On May 1, 2012, the Department published a document in the Federal Register (77 FR 25658) announcing its intent to establish a negotiated rulemaking committee under section 492 of the HEA, 20 U.S.C. 1098a, to develop proposed regulations designed to prevent fraud and otherwise ensure proper use of title IV, HEA program funds. In particular, we announced our intent to propose regulations to address the use of debit cards and other banking mechanisms for disbursing title IV, HEA program funds, and to improve and streamline the campus-based Federal Student Aid programs. We also announced two public hearings at which interested parties could comment on the topics suggested by the Department and suggest additional topics for consideration for action by the negotiated rulemaking committee. Those hearings were held on May 23, 2012, in Phoenix, Arizona, and on May 31, 2012, in Washington, DC. We invited parties to comment and submit topics for consideration in writing, as well.

On April 16, 2013, we published a document in the Federal Register (78 FR 22467, as corrected at 78 FR 25235), announcing additional topics for consideration for action by the negotiated rulemaking committee. Those additional topics for consideration included cash management of funds provided under the title IV, HEA programs; State authorization for programs offered through distance education or correspondence education; State authorization for foreign locations of institutions located in a State; clock to credit hour conversion; gainful employment; changes made by the Violence Against Women Reauthorization Act of 2013, Public Law 113-4, to the campus safety and security reporting requirements in the HEA; and the definition of “adverse credit” for borrowers in the Federal Direct PLUS Loan Program. We also announced three public hearings at which interested parties could comment on the new topics suggested by the Department and suggest additional topics for consideration for action by the negotiating committee.

On May 13, 2013, we announced in the Federal Register (78 FR 27880) the addition of a fourth hearing. The four hearings were held in May 2013, in Washington, DC, Minneapolis, Minnesota, and San Francisco, California; and in June 2013, in Atlanta, Georgia. We also invited parties unable to attend a public hearing to submit written comments on the additional topics and to submit other topics for consideration. Transcripts from all six public hearings are available at http://www2.ed.gov/policy/highered/reg/hearulemaking/2012/index.html. Written comments submitted in response to the May 1, 2012, and April 16, 2013, notices may be viewed through the Federal eRulemaking Portal at www.regulations.gov. Instructions for finding comments are available on the site under “How to Use Regulations.gov” in the Help section. Individuals can enter docket ID ED-2012-OPE-0008 in the search box to locate the appropriate docket.

On June 12, 2013, we announced in the Federal Register (78 FR 35179) our intent to establish a negotiated rulemaking committee to prepare proposed regulations for the title IV, HEA programs. The proposed regulations would establish measures for programs that prepare students for gainful employment in a recognized occupation. The notice requested nominations of individuals for membership on the committee who could represent the interests of key stakeholder constituencies.

The Department considered nominations submitted between the time of the publication of the notice on June 12, 2013, and July 12, 2013. Negotiators were sought to represent constituencies that generally included students; legal assistance organizations that represent students; consumer advocacy organizations; financial aid administrators at postsecondary institutions; State higher education executive officers; State Attorneys General and other appropriate State officials; business and industry; institutions of higher education eligible to receive Federal assistance under title III, parts A, B, and F and title V of the HEA, which include Historically Black Colleges and Universities, Hispanic-Serving Institutions, American Indian Tribally Controlled Colleges and Universities, Alaska Native and Native Hawaiian-Serving Institutions, Predominantly Black Institutions, and other institutions with a substantial enrollment of needy students as defined in title III of the HEA; two-year public institutions of higher education; four-year public institutions of higher education; private, non-profit institutions of higher education; private, for-profit institutions of higher education; and regional accrediting agencies, national accrediting agencies, and specialized accrediting agencies. Each constituency selected would have a primary and an alternate member. On August 2, 2013, the Department published the list of negotiators who were selected on its Web site.[1]

The negotiated rulemaking committee met to develop proposed regulations on September 9-11 and November 18-20, 2013. The latter session was rescheduled from October 21-23, due to the shutdown of the Federal Government from October 1-16, which resulted from a lapse in appropriations. At the request of the committee, the Department added a third and final session held on December 13, 2013. These sessions, unlike the sessions Start Printed Page 16431involving the 2011 Final Rules, were focused solely on the topic of gainful employment.

At its first meeting, the committee reached agreement on its protocols, which generally set out the committee membership, the topics of discussion and negotiation, and the standards by which the committee would operate. These protocols provided, among other things, that the non-Federal negotiators would represent in negotiations the organizations listed after their names in the protocols. The committee included the following members:

Rory O'Sullivan, Young Invincibles, and Kalwis Lo (alternate), United States Students Association, representing students.

Eileen Connor, New York Legal Assistance Group, and Whitney Barkley (alternate), Mississippi Center for Justice, representing legal assistance organizations that represent students.

Margaret Reiter, a California-based consumer protection attorney, and Tom Tarantino (alternate), Veterans of America, representing consumer advocacy organizations.

Kevin Jensen, College of Western Idaho, and Rhonda Mohr (alternate), California Community Colleges Chancellor's Office, representing financial aid administrators.

Jack Warner, South Dakota Board of Regents, and Sandra Kinney (alternate), Louisiana Community and Technical College System, representing State higher education executive officers.

Della Justice, Office of the Kentucky Attorney General, and Libby DeBlasio (alternate), Office of the Colorado Attorney General, representing State attorneys.

Ted Daywalt, VetJobs, and Thomas Kriger (alternate), AFL-CIO, representing the business and labor communities.

Helga Greenfield, Spelman College, and Ronnie Higgs (alternate), California State University at Monterey Bay, representing minority-serving institutions.

Richard Heath, Anne Arundel Community College, and Glen Gabert (alternate), Hudson County Community College, representing two-year public institutions.

Barmak Nassirian, American Association of State College and Universities, and Barbara Hoblitzell (alternate), University of California, representing four-year public institutions.

Jenny Rickard, University of Puget Sound, and Thomas Dalton (alternate), Excelsior College, representing private, non-profit institutions.

Brian Jones, Strayer University, and Raymond Testa (alternate), Empire Education Group, representing private, for-profit institutions—publicly traded.

Marc Jerome, Monroe College, and Justin Berkowitz (alternate), Daytona College, representing private, for-profit institutions—not publicly traded.

Belle Wheelan, Southern Association of Colleges and Schools Commission on Colleges, and Neil Harvison (alternate), American Occupational Therapy Association, representing accrediting agencies.

John Kolotos, U.S. Department of Education, representing the Federal Government.

The protocols also provided that, unless agreed to otherwise, consensus on all issues in the proposed regulations had to be achieved for consensus to be reached on the entire proposed rule. The protocols also specified that consensus means that there must be no dissent by any members.

During each of the committee meetings, the committee reviewed and discussed the Department's drafts of proposed regulations and the committee member's alternative proposals and suggestions. At the final meeting on December 13, 2013, the committee did not reach consensus on the Department's proposed regulations. For that reason, and according to the committee's protocols, all parties who participated or were represented in the negotiated rulemaking, in addition to all members of the public, may comment freely on the proposed regulations. For more information on the negotiated rulemaking sessions, please visit: http://www2.ed.gov/policy/highered/reg/hearulemaking/2012/gainfulemployment.html.

Summary of Relevant Data Available

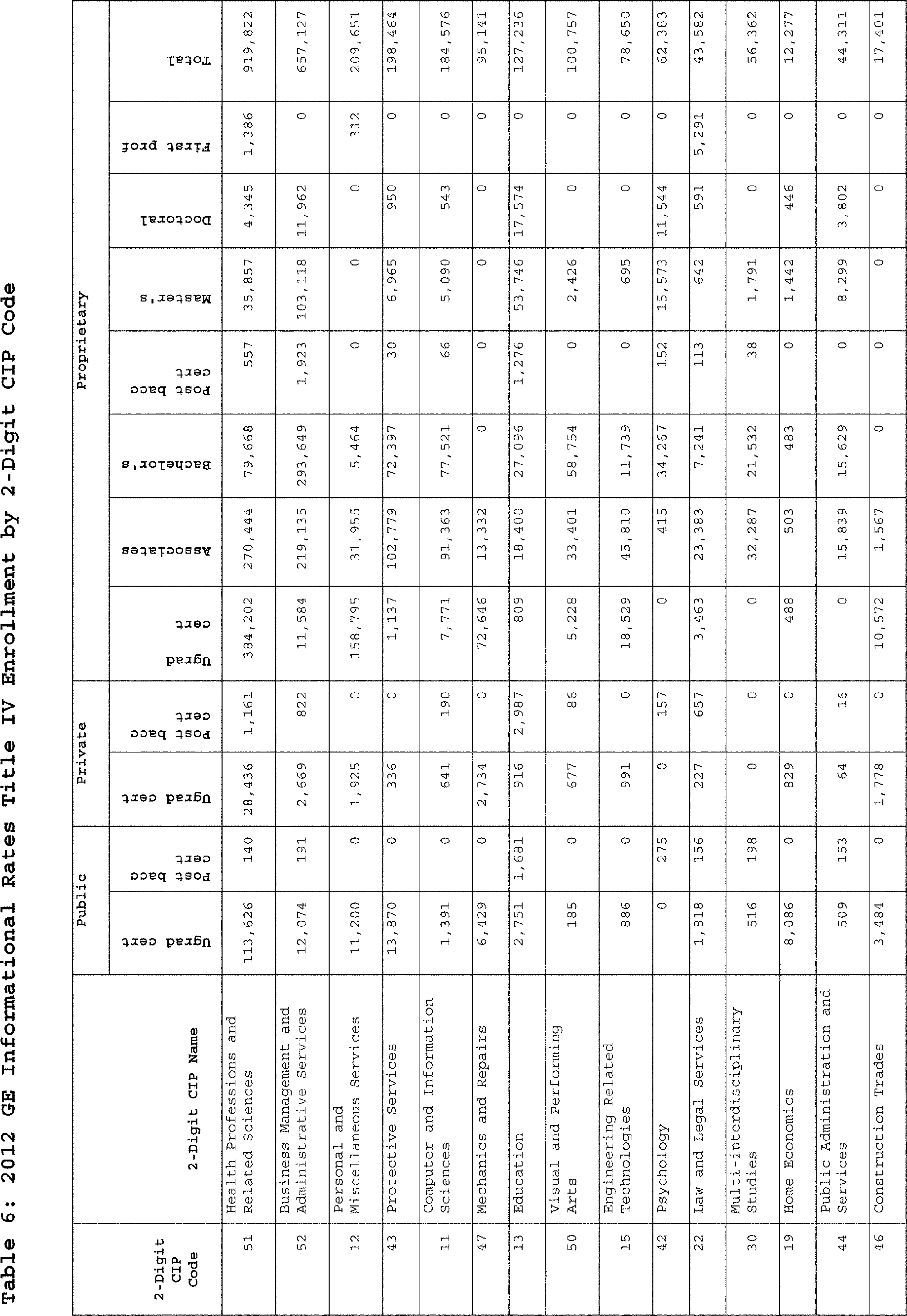

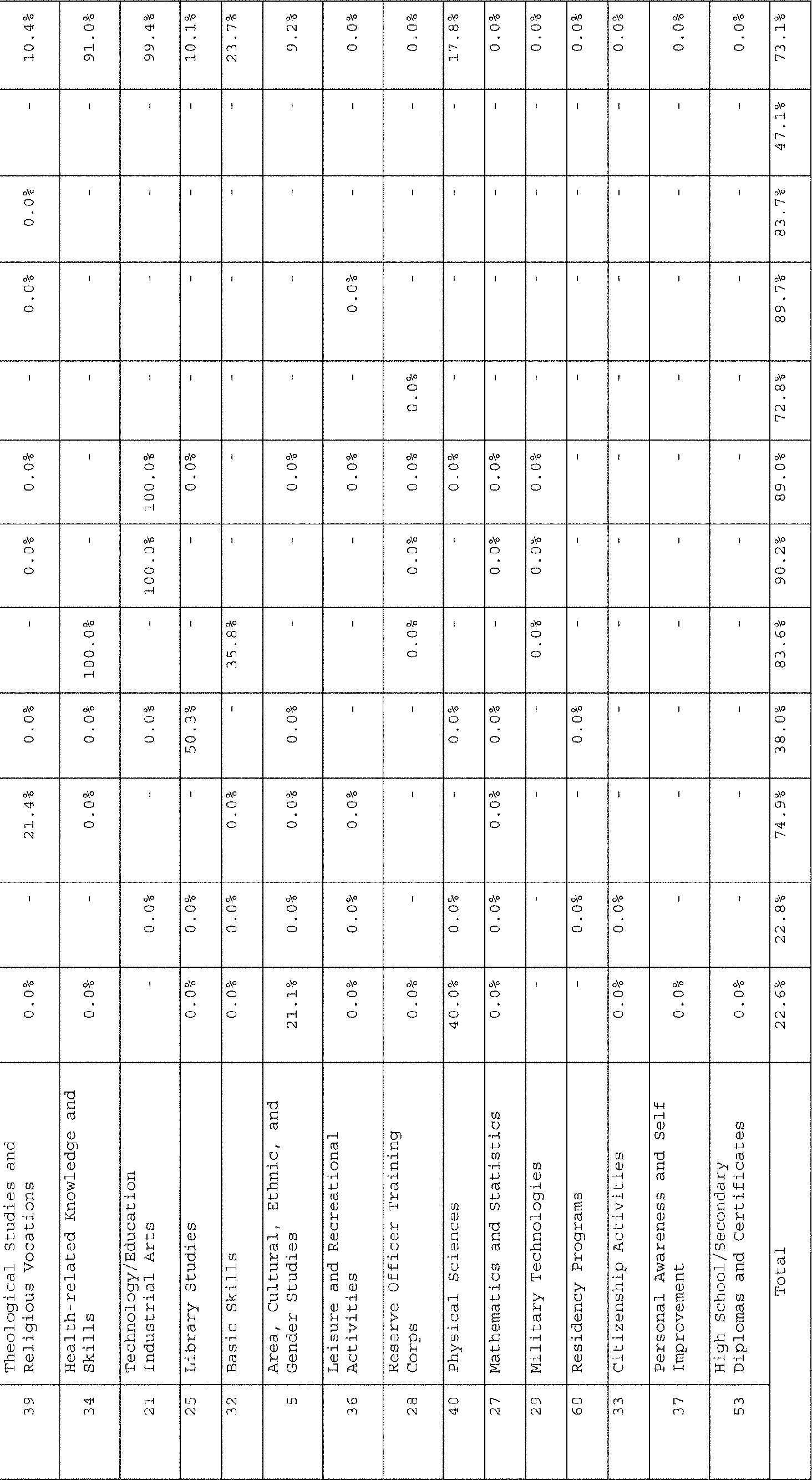

The Gainful Employment Data

After the effective date of the 2011 Final Rules on July 1, 2011, the Department received, pursuant to the reporting requirements of the 2011 Final Rules, information from institutions on their GE programs for award years 2006-2007 through 2010-2011 (GE Data). The GE Data included information on students who received title IV, HEA program funds, as well as students who did not. After the decisions in APSCU v. Duncan, the Department removed from NSLDS and destroyed the data on students who did not receive title IV, HEA program funds.

The 2011 GE Informational Rates

In June 2012, the Department released the “2011 GE informational rates.” [2] The 2011 GE informational rates include informational debt-to-earnings rates and dollar-based loan repayment rates for GE programs. The 2011 informational debt-to-earnings rates were calculated by program and based on the debt and earnings of students who completed GE programs between October 1, 2006, and September 30, 2008—the “07/08 2011 D/E rates cohort”. The annual loan payment component of the debt-to-earnings formulas was calculated for each program using information from the GE Data and NSLDS. For the annual earnings figures that were used to make the debt-to-earnings calculations, the Department obtained from the Social Security Administration (SSA) the 2010 annual earnings, by program, of the 07/08 2011 D/E rates cohort. The 2011 informational dollar-based loan repayment rates were calculated by program for students who entered repayment between October 1, 2006, and September 30, 2008—the “07/08 2011 repayment rates cohort”—on loans under the Federal Family Education Loan (FFEL) Program and under the William D. Ford Direct Loan (Direct Loan) Program for attendance in a GE program. The repayment rate calculations were made using student loan information for the 07/08 2011 repayment rates cohort from the GE Data and NSLDS.

The 2011 GE informational rates had no effect on the eligibility of GE programs. This information was intended to help institutions understand how their programs might fare under the 2011 Final Rules when they became effective.

The Session 1 2012 GE Informational Rates

On August 29, 2013, prior to the first meeting of the negotiated rulemaking committee for the new negotiated rulemaking, the Department released the “Session 1 2012 GE informational rates” [3] to inform the committee's discussion of the Department's proposals. The Session 1 2012 GE informational rates include two sets of informational debt-to-earnings rates, informational dollar-based repayment rates, and informational borrower-based Start Printed Page 16432repayment rates for GE programs. The Department also issued an explanation of the methodology used to make the Session 1 2012 GE informational rates calculations.[4] The first set of Session 1 2012 GE informational debt-to-earnings rates were calculated by program and based on the debt and earnings of students receiving title IV, HEA program funds who completed GE programs between October 1, 2006, and September 30, 2008—the “07/08 2012 D/E rates cohort.” The second set of Session 1 2012 GE informational debt-to-earnings rates were calculated by program and based on the debt and earnings of students receiving title IV, HEA program funds who completed GE programs between October 1, 2007, and September 30, 2009—the “08/09 2012 D/E rates cohort.”

The annual loan payment component of the debt-to-earnings formula for both sets of Session 1 2012 GE informational debt-to-earnings rates were calculated for each program using information from the GE Data and other information in NSLDS. For the annual earnings figures that were used in the debt-to-earnings calculations, the Department obtained from SSA the 2011 annual earnings, by program, of the 07/08 2012 D/E rates cohort and the 08/09 2012 D/E rates cohort. Both Session 1 2012 GE informational debt-to-earnings rates were calculated using the following criteria:

- N-size: 10

- Amortization schedule: 10 years for all credential levels

- Interest rate: 6.8 percent

See “§ 668.404 Calculating D/E rates” for an explanation of these criteria. The Session 1 2012 GE informational debt-to-earnings rates files also include rates calculated using variations of the n-size and amortization schedule criteria for comparative purposes.

The Session 1 2012 GE informational dollar-based and borrower-based loan repayment rates were calculated by program for students receiving title IV, HEA program funds who entered repayment between October 1, 2006, and September 30, 2008—the “07/08 2012 repayment rates cohort”—on FFEL and Direct Loans for enrollment in a GE program. The repayment rate calculations were made using student loan information for the 07/08 2012 repayment rates cohort from the GE Data and NSLDS.

The Session 1 2012 GE informational rates include information on the sector and institution type for each program based on NSLDS records as of August 2013.

The Session 3 2012 GE Informational Rates

Prior to the third rulemaking session in December 2013, the Department released the “Session 3 2012 GE informational rates.” [5] The Session 3 2012 GE informational rates include a revised version of one of the Session 1 2012 GE informational debt-to-earnings rates and, additionally, informational program cohort default rates for GE programs. The Department also issued an explanation of the methodology used to make the 2012 Session 3 GE informational rate calculations.[6]

As described above, one set of the Session 1 2012 GE informational debt-to-earnings rates is based on the debt and earnings of the 08/09 2012 D/E rates cohort. For Session 3, this set of informational debt-to-earnings rates was revised to remove a small group of non-GE programs that were included in the Session 1 2012 GE informational rates by error and, also, recalculated using an interest rate of 3.37 percent. The Session 3 2012 GE informational rates files also include debt-to-earnings rates calculated using variations of the n-size and amortization schedule criteria for comparative purposes.

The Session 3 2012 GE informational program cohort default rates were calculated by program for students receiving title IV, HEA program funds who entered repayment between October 1, 2008, and September 30, 2009—the “09 2012 program cohort default rates cohort”—on FFEL and Direct Loans for enrollment in a GE program. The program cohort default rate calculations were made using student loan information for the 09 2012 program cohort default rates cohort from the GE Data and NSLDS.

The Session 3 2012 GE informational rates include information on the sector and institution type for each program based on NSLDS records as of August 2013 for programs with D/E rates data. Sector and institution type for programs with pCDR data but no D/E rates data were based on NSLDS records as of November 2013.

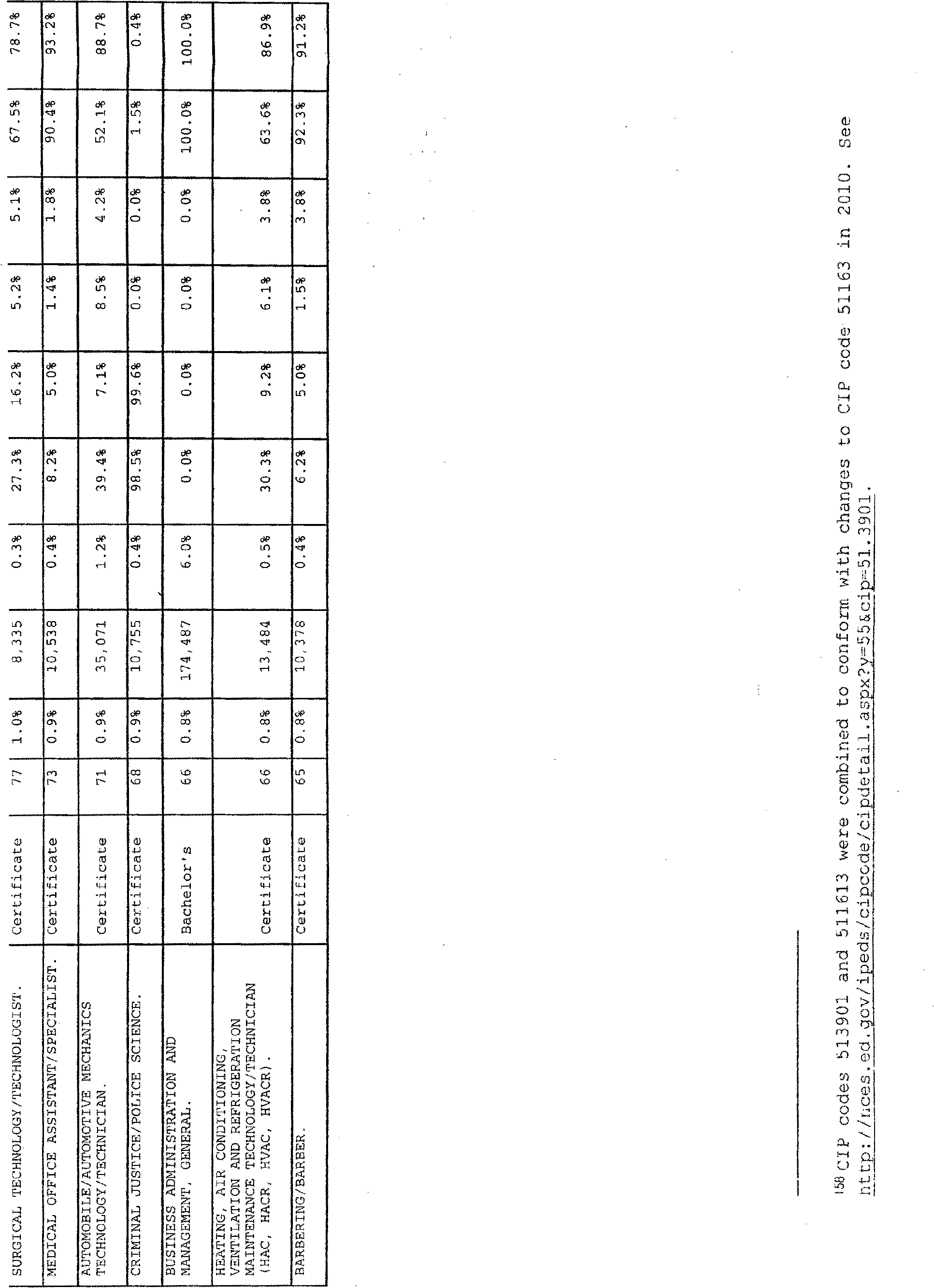

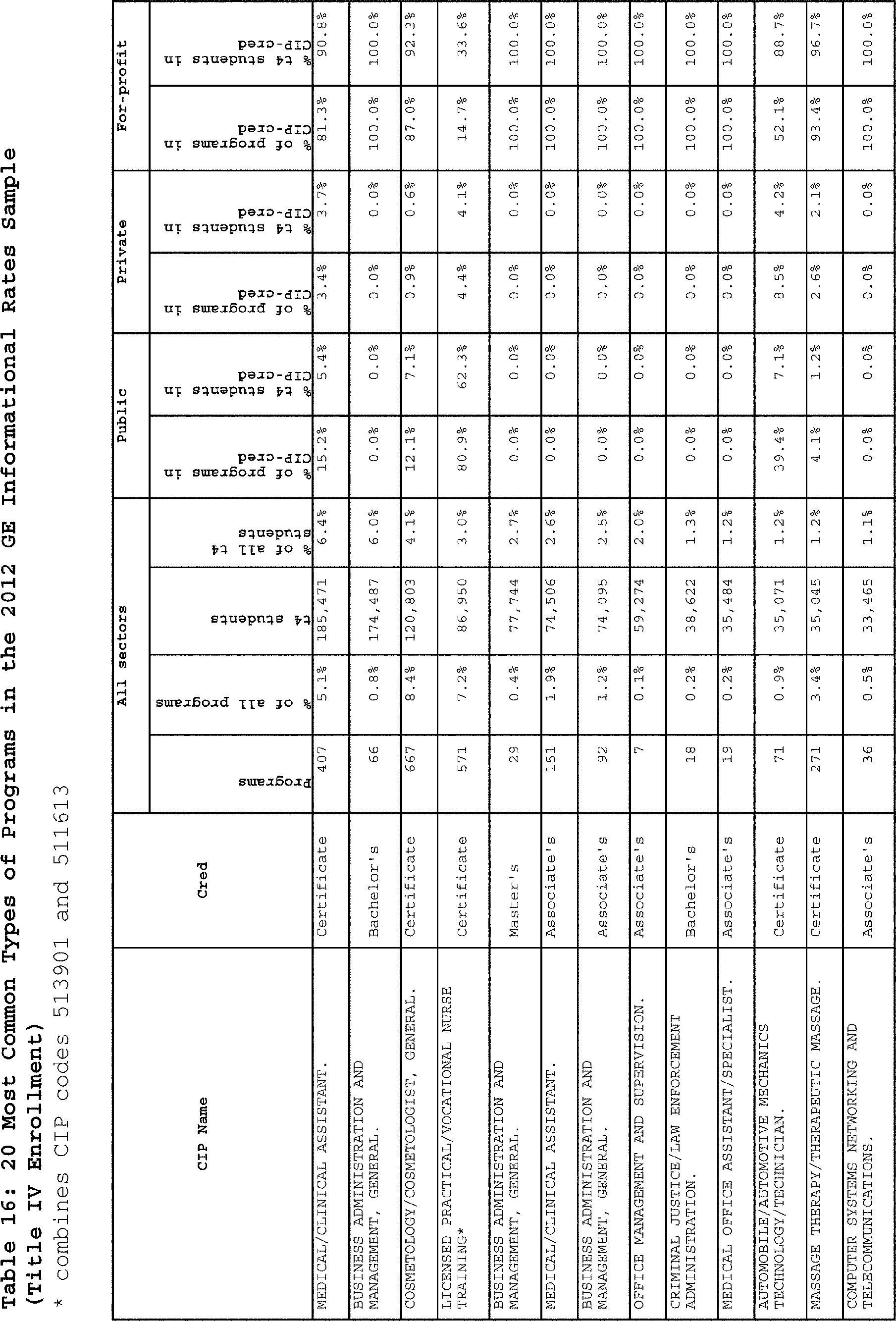

The 2012 GE Informational Rates

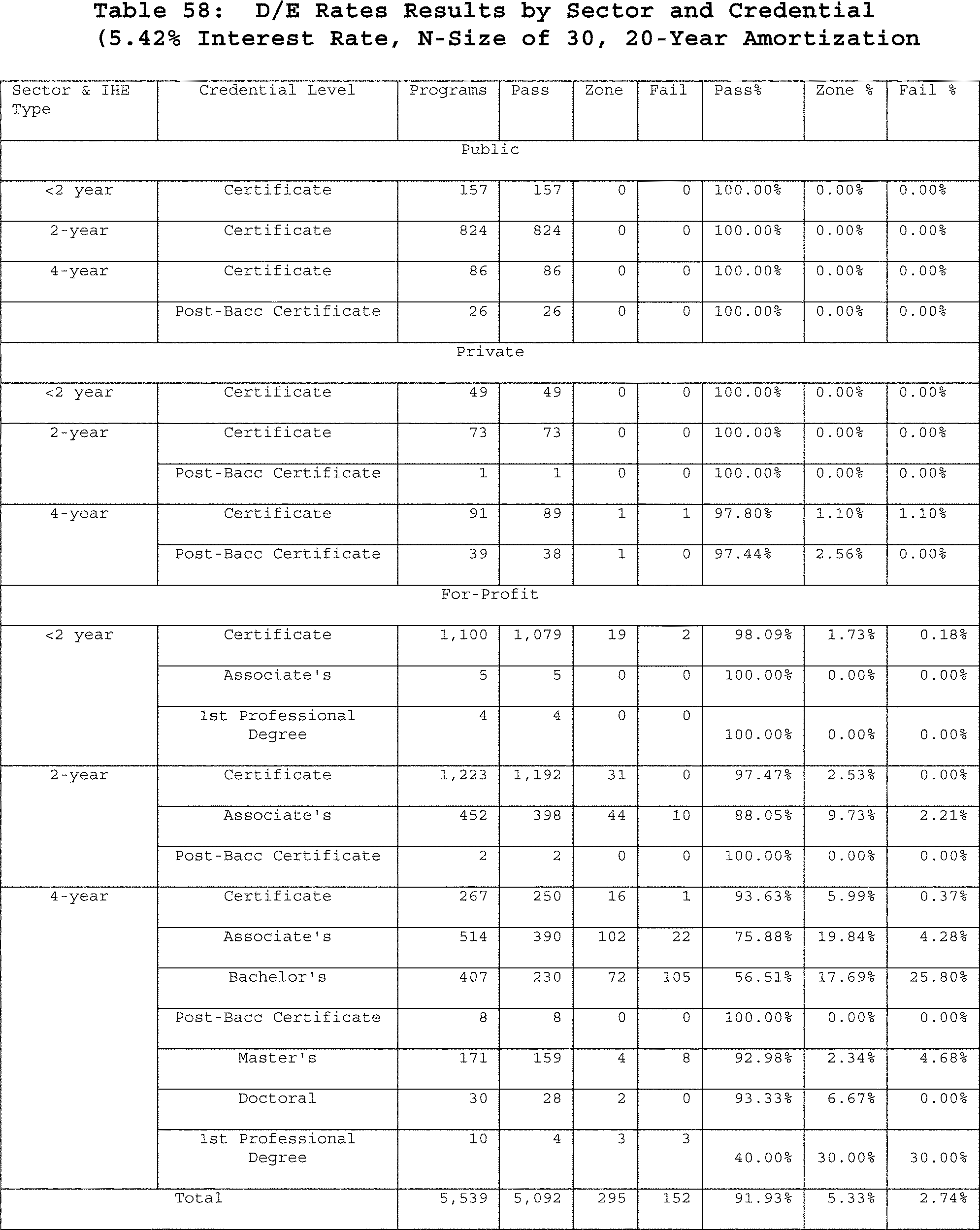

With this NPRM, the Department has released the “2012 GE informational rates.” [7] The 2012 GE informational rates include a recalculated version of the Session 3 2012 GE informational debt-to-earnings rates using the following criteria:

- N-size: 30

- Amortization schedule: 10 years for certificate and associate degree programs, 15 years for bachelor's and master's degree programs, and 20 years for doctoral and first professional programs

- Interest rate: 5.42 percent

See “§ 668.404 Calculating D/E rates” for an explanation of these criteria. The 2012 GE informational debt-to-earnings rates files also include debt-to-earnings rates calculated using variations of the n-size and amortization schedule criteria for comparative purposes. In addition to the 2012 GE informational debt-to-earnings rates, the 2012 GE informational rates also include the same informational program cohort default rates released as a part of the Session 3 2012 GE informational rates. The Department's D/E rates analysis and pCDR analysis in this NPRM are based on the 2012 GE informational rates unless otherwise specified.

The 2012 GE informational rates include information on the sector and institution type for each program based on NSLDS records as of November 2013 for all informational rate programs.

Summary of Proposed Regulations

The proposed regulations would—

- Define what it means for a program to provide training that prepares students for gainful employment in a recognized occupation.

- Create a process by which an institution establishes the eligibility of a GE program by certifying that the GE program satisfies applicable accrediting and licensing requirements for the occupations for which the program purports to prepare students.

- Establish an accountability framework, in which two complementary yet independent measures—the D/E rates measure and the pCDR measure—would be used to determine whether a GE program remains eligible for title IV, HEA program funds.

- Establish the process by which a GE program would be evaluated and the Start Printed Page 16433standards by which the program would be assessed, under the accountability framework using—

○ The D/E rates measure to evaluate the amount of debt students completing a GE program incurred in the program in comparison to their discretionary and annual earnings after completing the program.

○ The pCDR measure to evaluate the default rate of former students enrolled in a GE program, regardless of whether they completed the program.

- Require institutions with GE programs that could become ineligible in an immediately succeeding year to provide a written warning to students and prospective students of the potential loss of ineligibility and the implications.

- Provide that, for a GE program that loses eligibility for title IV, HEA program funds, as well as any program that is not passing the D/E rates measure and the pCDR measure and that is discontinued by the institution, the loss of eligibility is for three calendar years.

- Require institutions to report relevant information related to its GE programs to the Secretary.

- Require an institution to disclose, including to students and prospective students, relevant information about its GE programs through a disclosure template developed by the Secretary.

Significant Proposed Regulations

We discuss substantive issues under the sections of the proposed regulations to which they pertain. Generally, we do not address proposed regulatory changes that are technical or otherwise minor in effect.

Section 668.401 Scope and Purpose

Current Regulations: There is no equivalent provision in the 2011 Final Rules.

Proposed Regulations: Proposed § 668.401 establishes the scope and purpose for subpart Q of the proposed regulations. Subpart Q would establish the rules and procedures under which the Secretary determines a GE program's eligibility for title IV, HEA program funds; an institution reports information about the GE program to the Secretary; and the institution discloses information about the GE program to students and prospective students.

We note that the terms “gainful employment program” or “GE program,” “student,” and “prospective student,” which are defined in proposed § 668.402, are first substantively used in proposed § 668.401 and are therefore explained here. Proposed § 668.402, as in § 668.7(a)(2) of the 2011 Prior Rule, provides that a “gainful employment program” or “GE program” is an educational program offered by an institution under § 668.8(c)(3) or (d) that is identified by using a combination of the institution's six-digit Office of Postsecondary Education ID (OPEID) number, the program's six-digit Classification of instructional program (CIP) code, and credential level. Proposed § 668.401 defines a GE program, for the purpose of subpart Q, as an educational program offered by an eligible institution that prepares students for gainful employment in a recognized occupation and that meets the title IV, HEA program eligibility and other requirements in the proposed regulations.

Under the proposed regulations, the term “student” would refer to an individual who received title IV, HEA program funds for enrolling in the applicable GE program. Although we did not specifically define the term “student” in the 2011 Final Rules, operationally, “student” included any individual enrolled in a GE program, regardless of whether the individual received title IV, HEA program funds. Limiting the term “student” to refer to an individual who received title IV, HEA program funds is a significant difference between the proposed regulations and the 2011 Final Rules.

The proposed regulations also define the term “prospective student” to refer to an individual who has contacted an eligible institution for the purpose of requesting information about enrolling in a GE program or who has been contacted directly by the institution or indirectly through advertising about enrolling in a GE program. In the 2011 Final Rules, the definition of “prospective student” in § 668.41(a) was used in connection with the disclosure requirements in § 668.6(b) and the warning requirements in § 668.7(j). That definition refers only to individuals who have contacted the institution requesting institutional admission information.

Reasons:

Scope

Through this rulemaking, the Department seeks to establish standards for title IV, HEA eligibility of postsecondary educational programs that prepare students for “gainful employment” in a recognized occupation, which include nearly all educational programs at for-profit institutions of higher education regardless of program length or credential level, as well as non-degree programs at public and private non-profit institutions such as community colleges. Common GE programs provide training for occupations in cosmetology, business administration, interior design, graphic design, medical assisting, dental assisting, nursing, and massage therapy.

Based on information in the Department's databases, we estimate that there are approximately 50,000 GE programs at postsecondary institutions around the country. We estimate that about 60 percent of these programs are at public institutions, 10 percent at private non-profit institutions, and 30 percent at for-profit institutions. The Federal investment in students attending these programs is significant. We estimate that in fiscal year 2010, approximately 4 million students receiving title IV, HEA program funds were enrolled in GE programs. These students received approximately $9.7 billion in Federal student aid grants and approximately $26 billion in loans.

Purpose

The proposed regulations are intended to address growing concerns about educational programs that, as a condition of eligibility for title IV, HEA program funds, are required by statute to provide training that prepares students for gainful employment in a recognized occupation (GE programs), but instead are leaving students with unaffordable levels of loan debt in relation to their earnings, or leading to default. Many GE programs are producing positive student outcomes. But a disproportionate number are failing to do so.

The Department's primary concerns, which drive both the accountability and transparency frameworks, are that a number of GE programs: (1) do not train students in the skills they need to obtain and maintain jobs in the occupation for which the program purports to train students, (2) provide training for an occupation for which low wages do not justify program costs, and (3) are experiencing a high number of withdrawals or “churn” because relatively large numbers of students enroll but few, or none, complete the program, which can often lead to default. The causes of these problems for students are numerous, including excessive costs, low completion rates, a failure to satisfy requirements that are necessary for students to obtain higher paying jobs in a field such as licensing, work experience, and programmatic accreditation, a lack of transparency regarding program outcomes, and aggressive or deceptive marketing practices.

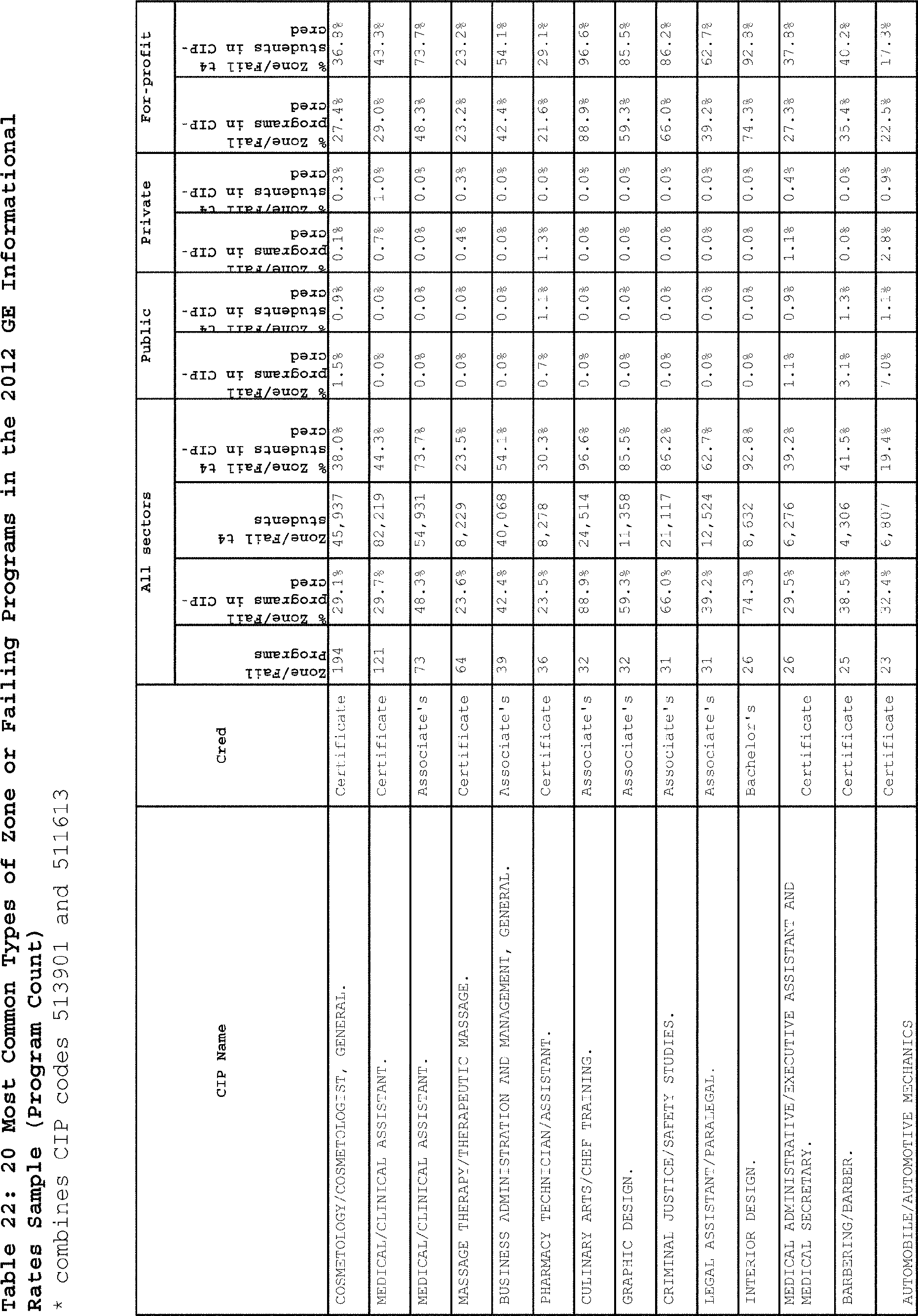

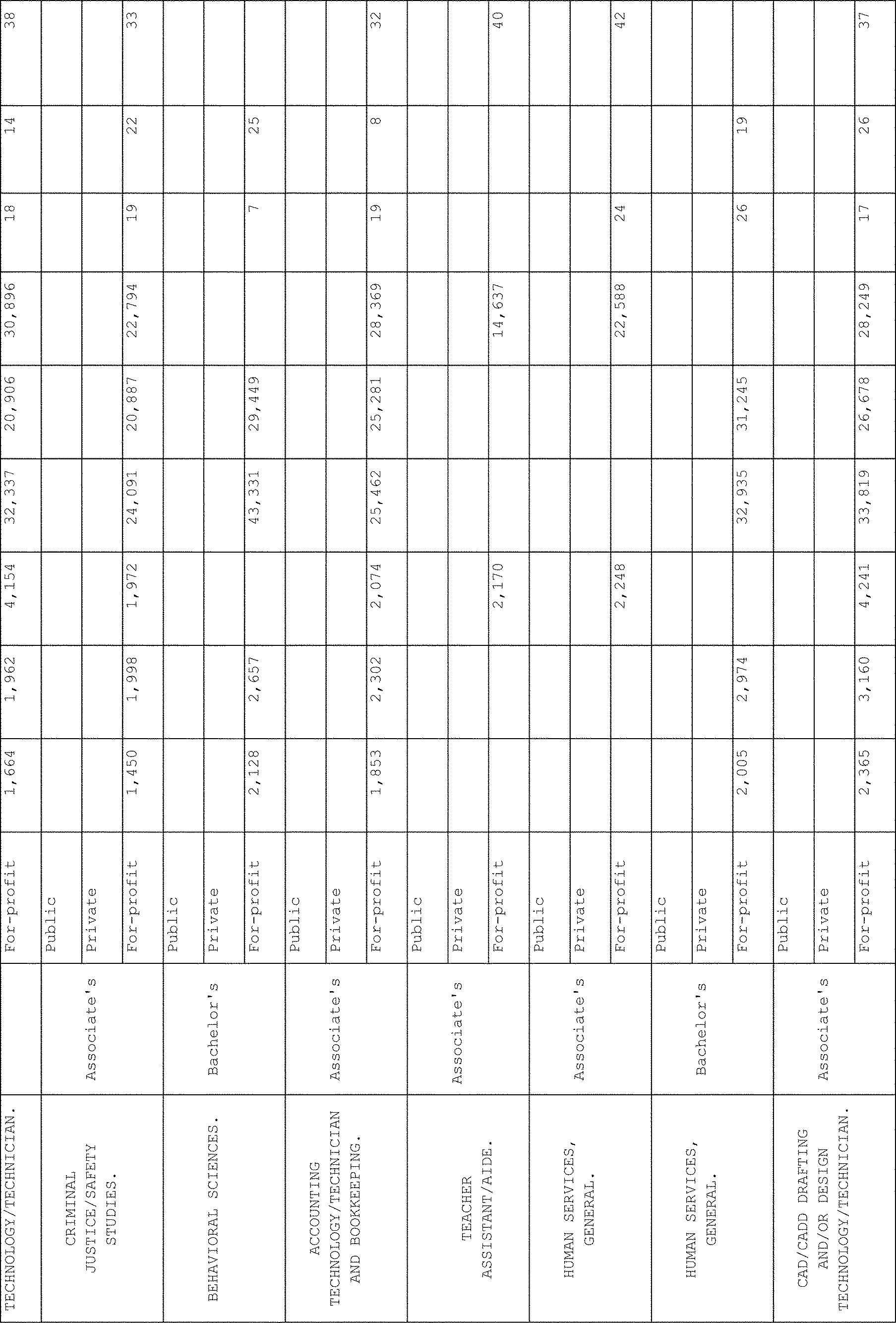

Our analysis of the D/E rates component of the 2012 GE informational rates reveals these poor outcomes among some GE programs. For example, 27 percent of GE programs evaluated produced graduates with Start Printed Page 16434average annual earnings below those of a full-time worker earning no more than the Federal minimum wage ($15,080).[8 9] Sixty-four percent of GE programs evaluated produced graduates with average annual earnings less than the earnings of individuals who have not obtained a high school diploma ($24,492).[10 11] Of programs with average earnings below those of a high school dropout, approximately 24 percent of former students defaulted on their Federal student loans within the first three years of entering repayment.[12]

As we noted in connection with the 2011 Prior Rule, the outcomes of students who attend for-profit educational institutions are of particular concern. 76 FR 34386. There is growing evidence of troubling practices at many of these institutions, such as some proprietary institutions overstating job placement rates. There has been growth in the number of qui tam lawsuits brought by private parties alleging wrongdoing at these institutions and numerous investigations brought by other Federal and State oversight agencies. Such activity only increases the Department's concerns about poor outcomes in GE programs.

For-profit institutions typically charge higher tuitions than do public postsecondary institutions. 76 FR 34386. Average tuition and fees at less-than-two-year for-profit institutions are more than double the average cost at less-than-two-year public institutions.[13] Attending a two-year for-profit institution costs a student four times as much as attending a community college.[14] Not surprisingly then, students enrolled in for-profit institutions accumulate far greater debt than students at public institutions. 76 FR 34386. In 2011-2012, 86 percent of students who earned certificates from for-profit institutions took out student loans compared to 35 percent of certificate recipients from public two-year institutions.[15] Of those who borrowed, the median loan amount borrowed of for-profit certificate recipients was $11,000 as opposed to $8,000 for certificate recipients from public two-year institutions.[16] Eighty-eight percent of associate degree graduates from for-profit institutions took out student loans, while only 40 percent of associate degree recipients from public two-year institutions took out student loans.[17] Of those who borrowed, for-profit associate degree recipients had a median loan amount borrowed of $23,590 in comparison to $10,000 for students who received their degrees from public two-year institutions.[18] Approximately 22 percent of borrowers who attended for-profit institutions default on their Federal student loans within the first three years of entering repayment as compared to about 13 percent of borrowers who attended public institutions.[19]

Although more expensive, there is growing evidence that many for-profit programs may not prepare students as well as comparable programs at public institutions. 75 FR 43618. A 2011 GAO report reviewed results of licensing exams for 10 occupations that are, by enrollment, among the largest fields of study.[20] The GAO report showed that for 9 out of 10 licensing exams, graduates of for-profit institutions had lower rates of passing than graduates of public institutions.[21] Many for-profit institutions devote greater resources to recruiting and marketing than they do to instruction or to student support services.[22] An investigation by the U.S. Senate Committee on Health, Education, Labor & Pensions (Senate HELP Committee) of thirty prominent for-profit institutions found that they spend almost 23 percent of their revenues on marketing and recruiting, but merely 17 percent on instruction.[23] Among the institutions that provided useable data to the committee, schools employed 35,202 recruiters compared with 3,512 career services staff and 12,452 support services staff.[24]

Lower rates of completion in many four-year for-profit institutions are also a cause for concern. 76 FR 34409. The six-year graduation rate of first-time undergraduate students who began at a four-year degree-granting institution in 2003-2004 was 34 percent at for-profit institutions in comparison to 65 percent at public institutions. However, for first-time undergraduate students who began at a two-year degree-granting institution in 2003-2004, the six-year graduation rate was 40 percent at for-profit institutions in comparison to 35 percent at public institutions.[25]

The higher costs of for-profit institutions, and the consequently greater amounts of debt incurred by their former students, together with generally lower rates of completion, continue to raise concerns about whether for-profit programs lead to earnings that justify the investment made by students. See 75 FR 43617. As we stated in connection with the 2011 Prior Rule, this “value proposition” is what “distinguishes programs `that lead to gainful employment in a recognized occupation.' ” 76 FR 34386. Analysis of data collected on the outcomes of 2003-2004 first-time beginning postsecondary students as a part of the Beginning Postsecondary Students Longitudinal Study shows that students who attend for-profit institutions are more likely to be idle, not working or in school, six years after starting their programs of study in comparison to students who attend other types of institutions.[26] Further, for-profit students no longer enrolled in school six years after beginning postsecondary education have lower earnings at the six-year mark than students who attend other types of institutions.[27]

These outcomes are troubling for two reasons. First, some students will have earnings that will not support the debt Start Printed Page 16435they incurred to enroll in these GE programs. Second, because students are limited under the HEA in the amounts of Federal grants and loans they may receive to support their education, their options to move to higher-quality and affordable programs are constrained as they may no longer have access to sufficient student aid. Specifically, Federal law sets lifetime limits on the amount of grant and subsidized loan assistance students may receive: Federal Pell Grants may be received only for the equivalent of 12 semesters of full-time attendance, and Federal subsidized loans may be received for no longer than 150 percent of the published program length.[28] These limitations make it even more critical that students' initial choices in GE programs prepare them for employment that provides adequate earnings and do not result in excessive debt.

In addition to concerns that some GE programs are not meeting the gainful employment requirement, the Department remains concerned that students seeking to enroll in these programs do not have access to reliable information that will enable them to compare programs in order to make informed decisions about where to invest their time and limited educational funding. As we noted in the 2011 Prior Rule, the Government Accountability Office (GAO) and other investigators have found evidence of high-pressure and deceptive recruiting practices at some for-profit institutions. See 76 FR 34386. In 2010, the GAO released results of undercover testing at 15 for-profit colleges across several States.[29] Thirteen of the colleges tested gave undercover student applicants “deceptive or otherwise questionable information” about graduation rates, job placement, or expected earnings.[30] Similarly, a more recent report by the Senate HELP Committee on the for-profit education sector found evidence that many of the most prominent for-profit institutions engage in aggressive sales practices and provide misleading information to prospective students.[31] Recruiters described “boiler room”-like sales and marketing tactics and internal institutional documents showed that recruiters are taught to identify and manipulate emotional vulnerabilities and target non-traditional students.[32]

More recently, a growing number of State and other Federal law enforcement authorities have launched investigations into whether the institutions that offer GE programs are using aggressive or even deceptive marketing and recruiting practices. Several State Attorneys General have already sued for-profit institutions to stop these fraudulent marketing practices and manipulations of job placement rates. On August 19, 2013, the New York State Attorney General announced a $10.25 million settlement with Career Education Corporation (CEC), a private for-profit education company, after its investigation revealed that CEC significantly inflated its graduates' job placement rates in disclosures made to students, accreditors, and the State.[33] The State of Illinois sued Westwood College for misrepresentations and false promises made to students enrolling in the company's criminal justice program.[34] The Commonwealth of Kentucky has filed lawsuits against several private for-profit institutions, including National College of Kentucky, Inc., for misrepresenting job placement rates, and Daymar College, Inc., for misleading students about financial aid and overcharging for textbooks.[35] And most recently, early this year, a group of 13 State Attorneys General issued Civil Investigatory Demands to Corinthian Colleges, Inc., Education Management Co., ITT Educational Services, Inc., and CEC, seeking information about student placement rate data and marketing and student recruitment practices of the companies. The States participating include Arizona, Arkansas, Connecticut, Idaho, Iowa, Kentucky, Missouri, Nebraska, North Carolina, Oregon, Pennsylvania, Tennessee, and Washington.

A 2012 report released by the Senate HELP Committee found extensive evidence of aggressive and deceptive recruiting practices, excessive tuition, and regulatory evasion and manipulation by for-profit colleges that preyed on service members, veterans, and their families as “dollar signs in uniform.” [36] The Los Angeles Times reported that recruiters from for-profit colleges have been known to recruit at Wounded Warriors centers and at veterans hospitals, where injured soldiers are pressured into enrolling through promises of free education and more.[37] Some for-profit colleges lure service members and veterans through a number of improper practices, including by offering post-9/11 GI Bill benefits that are intended for living expenses as “free money,” which is difficult for jobless veterans returning home to turn down.[38] This results in many veterans enrolling in online courses to get the monthly benefits even if they have no intention of completing the coursework.[39] In addition, some institutions have recruited veterans with serious brain injuries and emotional vulnerabilities without providing adequate support and counseling, engaged in misleading recruiting practices onsite at military installations, and failed to accurately disclose information regarding the graduation rates of veterans.[40] In June 2012, an investigation in 20 States, led by the Commonwealth of Kentucky's Attorney General, resulted in a $2.5 million settlement with QuinStreet, Inc. and the closure of GIBill.com, a Web site that appeared as if it was an official site of the U.S. Department of Veterans Affairs, but was in reality a for-profit portal that steered veterans to 15 colleges, almost all for-profit institutions, including Kaplan University, the University of Phoenix, Strayer University, DeVry University, and Westwood College.[41]

Further, the Consumer Financial Protection Bureau issued Civil Start Printed Page 16436Investigatory Demands to Corinthian Colleges, Inc. and ITT Educational Services, Inc. in November, 2013, demanding information about their marketing, advertising, and lending policies.[42] The Securities and Exchange Commission also subpoenaed records from Corinthian Colleges, Inc. on June 6, 2013, seeking student information in the areas of recruitment, attendance, completion, placement, and loan defaults.[43] These inquiries supplement the Department's existing monitoring and compliance efforts to protect against such abuses.

Simply put, without reliable information, students, prospective students, and their families are vulnerable to inaccurate or misleading information when they make critical decisions about their educational investments and, based on that information, may enroll in poorly performing programs. Furthermore, without accurate and comparable information, the public, taxpayers, and the Government are in the dark as to the performance of these programs and the return on the Federal investment in these programs. Although we do not seek to impose requirements through this rulemaking that specifically address all of these allegations of abuse, the proposed regulations would help ensure, among other things, that students, prospective students, and their families and the public, taxpayers, and the Government are provided with reliable and comparable information about the student outcomes of GE programs.

We acknowledge that since the prior rulemaking effort in 2011, some for-profit institutions have made positive changes to their GE programs. For example, some institutions now offer trial enrollment periods for students before they require a full financial commitment and scholarships to students who reach milestones toward completing their programs.[44] These steps show that positive change is possible, but the concerns highlighted here demonstrate that more improvement in the sector is needed. To encourage institutions to start or continue to take effective action to reduce debt and increase earnings prospects for students, by this regulatory action, we propose to define what it means for a program to provide training that prepares students for gainful employment in a recognized occupation by establishing measures a program must meet in order to be eligible for title IV, HEA program funds, and to better inform students, prospective students, and their families, as well as the public, taxpayers, and the Government, by requiring institutions to report and disclose relevant information about the outcomes of their GE programs.

Legal Authority

We seek, through this regulatory action, to define a statutory requirement that applies only to certain educational programs—GE programs—and which is a condition of eligibility for title IV, HEA program funds. Title IV, HEA program funds are Federal student aid funds available to students and parents to assist them in paying for a postsecondary educational program. These funds include student loans under the Direct Loan Program, the Federal Perkins Loan (Perkins Loan) Program, and (until 2010) the FFEL Program; grants under the Federal Pell Grant Program, the Federal Supplemental Educational Opportunity Grant Program, the Iraq-Afghanistan Service Grant Program, and the TEACH Grant Program; and earnings under the Federal Work-Study Program.

Under title IV of the HEA, institutions must establish eligibility to offer eligible programs in order for their students to receive Federal student aid funds. In some cases, eligible institutions must separately establish the eligibility of their programs in order for students in those programs to receive title IV, HEA assistance. See, e.g., 20 U.S.C. 1001(a)(3), 34 CFR 668.8(c) (educational program offered by public or private non-profit institution of higher education must lead to or be creditable toward recognized credential); 34 CFR 600.20(c) (approval required for institution to increase level of programs from undergraduate to graduate); 20 U.S.C. 1088(b)(3), 34 CFR 668.8(m) (program offered through telecommunications eligible only if accredited by agency recognized by the Department to evaluate such programs).

One type of program for which an institution must establish program-level title IV, HEA eligibility is “a program of training to prepare students for gainful employment in a recognized occupation,” which is the subject of this rulemaking. 20 U.S.C. 1001(b)(1), 1002(b)(1)(A)(i), (c)(1)(A). Section 481 of the HEA articulates this same requirement: as pertinent here, it defines an “eligible program” as a “program of training to prepare students for gainful employment in a recognized profession.” 20 U.S.C. 1088(b). This statutory requirement—the “gainful employment” requirement—is what the Department seeks to define here.

The Department's authority for this regulatory action is derived primarily from these provisions, which establish the gainful employment requirement, and two additional sources. These authorities, including relevant legislative history which supports components of the GE accountability framework, are discussed here and also in more detail in “§ 668.403 Gainful employment framework.” Specifically, section 410 of the General Education Provisions Act provides the Secretary with authority to make, promulgate, issue, rescind, and amend rules and regulations governing the manner of operations of, and governing the applicable programs administered by, the Department. 20 U.S.C. 1221e-3. This authority includes the power to promulgate regulations relating to programs administered by the Department, such as the title IV, HEA programs that provide Federal loans, grants, and other aid to students. Furthermore, section 414 of the Department of Education Organization Act (DEOA) authorizes the Secretary to prescribe those rules and regulations the Secretary determines necessary or appropriate to administer and manage the functions of the Department. 20 U.S.C. 3474. These authorities thus empower the Secretary to promulgate regulations that, in this case, define the gainful employment requirement in the HEA by: establishing measures to determine the eligibility of GE programs for title IV, HEA program funds; requiring institutions to report information about the programs to the Secretary; and requiring institutions to Start Printed Page 16437disclose information about the programs to students, prospective students, and their families, the public, taxpayers, and the Government, and institutions.

Section 431 of the DEOA gives the Department added authority to establish rules to require institutions to make data available to the public on the performance of their GE programs and about students enrolled in those programs. That section gives the Secretary the authority to inform the public about federally supported education programs, and to collect data and information on applicable programs for the purpose of obtaining objective measurements of their effectiveness in achieving their intended purposes. 20 U.S.C. 1231a. This provision lends additional support for the proposed reporting and disclosure requirements, which will enable the Secretary to collect data and information related to GE programs, for the purpose of evaluating whether they are achieving their intended purpose, and to inform the public about relevant information related to those federally supported programs.

As discussed in the “Background of The Proposed Regulations, Public Participation, and Negotiated Rulemaking,” some of these authorities were subject to scrutiny by the U.S. District Court for the District of Columbia in Association of Private Sector Colleges and Universities v. Duncan, 870 F.Supp.2d 133 (D.D.C. 2012), and 930 F.Supp.2d 210 (D.D.C. 2013), a suit brought by APSCU to challenge the Department's 2011 prior rulemaking efforts to define the gainful employment requirement. In deciding that challenge, the court reached several conclusions about the Department's rulemaking authority in this matter, and its conclusions have informed and framed the Department's exercise of that authority in proposing these regulations. Notably, the court agreed with the Department's position that the Secretary enjoys broad authority to make, promulgate, issue, rescind, and amend the rules and regulations governing the applicable programs administered by the Department, such as the title IV, HEA programs, and that the Secretary is “authorized to prescribe such rules and regulations as the Secretary determines necessary or appropriate to administer and manage the functions of the Secretary or the Department.” APSCU v. Duncan, 870 F.Supp.2d at 141; see 20 U.S.C. 3474. Furthermore, in answering the question whether the Department's regulatory effort to define the gainful employment requirement fell within its statutory authority, the court found the exercise within that power. Specifically, it concluded that the phrase “gainful employment in a recognized occupation” is ambiguous and that in enacting the requirement that used that phrase, Congress delegated interpretive authority to the Department. APSCU v. Duncan, 870 F.Supp.2d at 146.

Likewise, the court upheld the Department's disclosure requirements, which are still in effect, rejecting APSCU's challenge to this provision and finding that the disclosure requirements “fall comfortably within [the Secretary's] regulatory power,” and are “not arbitrary or capricious.” Id. at 156.

Overview of Accountability and Transparency Frameworks

As stated previously, the Department's goals in the proposed regulations are twofold: to establish an accountability framework for GE programs, and to increase the transparency of student outcomes of GE programs. In addition, we believe a key benefit of this regulatory action would be to receive suggestions on how to identify programs that are exceptional performers, and how to share best practices with institutions interested in improving their programs. Although recognition of exceptional programs is not expressly addressed in the proposed regulations, we invite comment on ways in which the best programs could, consistent with our authority under the HEA, be identified and rewarded and how best practices could be highlighted and shared with others.

In service of these goals, we are proposing an accountability framework based upon program certification requirements and minimum standards for program outcomes. We are also proposing reporting and disclosure requirements designed to both support the accountability framework and to increase transparency so that relevant information regarding GE programs is disseminated to students, prospective students, and their families, the public, taxpayers, and the Government, and institutions.

As part of the accountability framework, to determine whether a program provides training that prepares students for gainful employment as required by the HEA, we propose procedures to establish a program's eligibility and to measure its outcomes on a continuing basis. To establish a program's eligibility, an institution would be required to certify that each of its GE programs meets all applicable accreditation and licensure requirements necessary for a student to obtain employment in the occupation for which the program provides training. This certification would be incorporated into the institution's program participation agreement. For a more detailed discussion of the proposed certification requirements, see “§ 668.414 Certification requirements for GE programs.”