|

Code of Federal Regulations (Last Updated: November 8, 2024) |

|

Title 12 - Banks and Banking |

|

Chapter X - Bureau of Consumer Financial Protection |

|

Part 1024 - Real Estate Settlement Procedures Act (Regulation X) |

Appendix C to Part 1024 - Instructions for Completing Good Faith Estimate (GFE) Form

-

Appendix C to Part 1024 - Instructions for Completing Good Faith Estimate (GFE) Form

The following are instructions for completing the GFE required under section 5 of RESPA and 12 CFR 1024.7 of the Bureau regulations. The standardized form set forth in this Appendix is the required GFE form and must be provided exactly as specified; provided, however, preparers may replace HUD's OMB approval number listed on the form with the Bureau's OMB approval number when they reproduce the GFE form. The instructions for completion of the GFE are primarily for the benefit of the loan originator who prepares the form and need not be transmitted to the borrower(s) as an integral part of the GFE. The required standardized GFE form must be prepared completely and accurately. A separate GFE must be provided for each loan where a transaction will involve more than one mortgage loan.

General Instructions

The loan originator preparing the GFE may fill in information and amounts on the form by typewriter, hand printing, computer printing, or any other method producing clear and legible results. Under these instructions, the “form” refers to the required standardized GFE form. Although the standardized GFE is a prescribed form, Blocks 3, 6, and 11 on page 2 may be adapted for use in particular loan situations, so that additional lines may be inserted there, and unused lines may be deleted.

All fees for categories of charges shall be disclosed in U.S. dollar and cent amounts.

Specific Instructions

Page 1

Top of the Form - The loan originator must enter its name, business address, telephone number, and email address, if any, on the top of the form, along with the applicant's name, the address or location of the property for which financing is sought, and the date of the GFE.

“Purpose.” - This section describes the general purpose of the GFE as well as additional information available to the applicant.

“Shopping for your loan.” - This section requires no loan originator action.

“Important dates.” - This section briefly states important deadlines after which the loan terms that are the subject of the GFE may not be available to the applicant. In Line 1, the loan originator must state the date and, if necessary, time until which the interest rate for the GFE will be available. In Line 2, the loan originator must state the date until which the estimate of all other settlement charges for the GFE will be available. This date must be at least 10 business days from the date of the GFE. In Line 3, the loan originator must state how many calendar days within which the applicant must go to settlement once the interest rate is locked. In Line 4, the loan originator must state how many calendar days prior to settlement the interest rate would have to be locked, if applicable.

“Summary of your loan .” - In this section, for all loans the loan originator must fill in, where indicated:

(i) The initial loan amount;

(ii) The loan term; and

(iii) The initial interest rate.

For reverse mortgage transactions:

(i) The initial loan amount disclosed on the GFE is the amount of the initial principal limit of the loan;

(ii) The loan term is disclosed as “N/A” when the loan term is conditioned upon the occurrence of a specified event, such as the death of the borrower or the borrower no longer occupying the property for a certain period of time; and

(iii) The initial interest rate is the interest rate indicated on the legal obligation.

The loan originator must fill in the initial monthly amount owed for principal, interest, and any mortgage insurance. The amount shown must be the greater of: (1) The required monthly payment for principal and interest for the first regularly scheduled payment, plus any monthly mortgage insurance payment; or (2) the accrued interest for the first regularly scheduled payment, plus any monthly mortgage insurance payment. For reverse mortgage transactions where there are no regular payment periods, the loan originator must disclose “Not Applicable” or “N/A” for the initial monthly amount owed for principal, interest, and any mortgage insurance.

The loan originator must indicate whether the interest rate can rise, and, if it can, must insert the maximum rate to which it can rise over the life of the loan. The loan originator must also indicate the period of time after which the interest rate can first change.

The loan originator must indicate whether the loan balance can rise even if the borrower makes payments on time, for example in the case of a loan with negative amortization. If it can, the loan originator must insert the maximum amount to which the loan balance can rise over the life of the loan. For Federal, State, local, or tribal housing programs that provide payment assistance, any repayment of such program assistance should be excluded from consideration in completing this item. If the loan balance will increase only because escrow items are being paid through the loan balance, the loan originator is not required to check the box indicating that the loan balance can rise. For reverse mortgage transactions, the loan originator must indicate that the loan balance can rise even if the borrower makes payments on time and the maximum amount to which the loan balance can rise must be disclosed as “Unknown.”

The loan originator must indicate whether the monthly amount owed for principal, interest, and any mortgage insurance can rise even if the borrower makes payments on time. If the monthly amount owed can rise even if the borrower makes payments on time, the loan originator must indicate the period of time after which the monthly amount owed can first change, the maximum amount to which the monthly amount owed can rise at the time of the first change, and the maximum amount to which the monthly amount owed can rise over the life of the loan. The amount used for the monthly amount owed must be the greater of: (1) The required monthly payment for principal and interest for that month, plus any monthly mortgage insurance payment; or (2) the accrued interest for that month, plus any monthly mortgage insurance payment. For reverse mortgage transactions, the loan originator must disclose that the monthly amount owed for principal, interest, and any mortgage insurance cannot rise.

The loan originator must indicate whether the loan includes a prepayment penalty, and, if so, the maximum amount that it could be.

The loan originator must indicate whether the loan requires a balloon payment and, if so, the amount of the payment and in how many years it will be due. Reverse mortgage transactions are not considered to be balloon transactions for the purposes of this disclosure on the GFE.

“Escrow account information.” - The loan originator must indicate whether the loan includes an escrow account for property taxes and other financial obligations. The amount shown in the “Summary of your loan” section for “Your initial monthly amount owed for principal, interest, and any mortgage insurance” must be entered in the space for the monthly amount owed in this section. For reverse mortgage transactions where the lender will establish an arrangement to pay for such items as property taxes and homeowner's insurance through draws from the principal limit, the loan originator must indicate that an escrow account is included and the amount shown in this section must be disclosed as 'N/A.'

“Summary of your settlement charges.” - On this line, the loan originator must state the Adjusted Origination Charges from subtotal A of page 2, the Charges for All Other Settlement Services from subtotal B of page 2, and the Total Estimated Settlement Charges from the bottom of page 2.

Page 2

“Understanding your estimated settlement charges.” - This section details 11 settlement cost categories and amounts associated with the mortgage loan. For purposes of determining whether a tolerance has been met, the amount on the GFE should be compared with the total of any amounts shown on the HUD-1 in the borrower's column and any amounts paid outside closing by or on behalf of the borrower.

“Your Adjusted Origination Charges”

Block 1, “Our origination charge.” - The loan originator must state here all charges that all loan originators involved in this transaction will receive, except for any charge for the specific interest rate chosen (points). A loan originator may not separately charge any additional fees for getting this loan, including for application, processing, or underwriting. The amount stated in Block 1 is subject to zero tolerance, i.e., the amount may not increase at settlement.

Block 2, “Your credit or charge (points) for the specific interest rate chosen.” - For transactions involving mortgage brokers, the mortgage broker must indicate through check boxes whether there is a credit to the borrower for the interest rate chosen on the loan, the interest rate, and the amount of the credit, or whether there is an additional charge (points) to the borrower for the interest rate chosen on the loan, the interest rate, and the amount of that charge. Only one of the boxes may be checked; a credit and charge cannot occur together in the same transaction.

For transactions without a mortgage broker, the lender may choose not to separately disclose in this block any credit or charge for the interest rate chosen on the loan; however, if this block does not include any positive or negative figure, the lender must check the first box to indicate that “The credit or charge for the interest rate you have chosen” is included in “Our origination charge” above (see Block 1 instructions above), must insert the interest rate, and must also insert “0” in Block 2. Only one of the boxes may be checked; a credit and charge cannot occur together in the same transaction.

For a mortgage broker, the credit or charge for the specific interest rate chosen is the net payment to the mortgage broker from the lender (i.e., the sum of all payments to the mortgage broker from the lender, including payments based on the loan amount, a flat rate, or any other computation, and in a table funded transaction, the loan amount less the price paid for the loan by the lender). When the net payment to the mortgage broker from the lender is positive, there is a credit to the borrower and it is entered as a negative amount in Block 2 of the GFE. When the net payment to the mortgage broker from the lender is negative, there is a charge to the borrower and it is entered as a positive amount in Block 2 of the GFE. If there is no net payment (i.e., the credit or charge for the specific interest rate chosen is zero), the mortgage broker must insert '0' in Block 2 and may check either the box indicating there is a credit of '0' or the box indicating there is a charge of '0.'

The amount stated in Block 2 is subject to zero tolerance while the interest rate is locked, i.e., any credit for the interest rate chosen cannot decrease in absolute value terms and any charge for the interest rate chosen cannot increase. (Note: An increase in the credit is allowed since this increase is a reduction in cost to the borrower. A decrease in the credit is not allowed since it is an increase in cost to the borrower.)

Line A, “Your Adjusted Origination Charges.” - The loan originator must add the numbers in Blocks 1 and 2 and enter this subtotal at highlighted Line A. The subtotal at Line A will be a negative number if there is a credit in Block 2 that exceeds the charge in Block 1. The amount stated in Line A is subject to zero tolerance while the interest rate is locked.

In the case of “no cost” loans, where “no cost” refers only to the loan originator's fees, Line A must show a zero charge as the adjusted origination charge. In the case of “no cost” loans where “no cost” encompasses third party fees as well as the upfront payment to the loan originator, all of the third party fees listed in Block 3 through Block 11 to be paid for by the loan originator (or borrower, if any) must be itemized and listed on the GFE. The credit for the interest rate chosen must be large enough that the total for Line A will result in a negative number to cover the third party fees.

“Your Charges for All Other Settlement Services”

There is a 10 percent tolerance applied to the sum of the prices of each service listed in Block 3, Block 4, Block 5, Block 6, and Block 7, where the loan originator requires the use of a particular provider or the borrower uses a provider selected or identified by the loan originator. Any services in Block 4, Block 5, or Block 6 for which the borrower selects a provider other than one identified by the loan originator are not subject to any tolerance and, at settlement, would not be included in the sum of the charges on which the 10 percent tolerance is based. Where a loan originator permits a borrower to shop for third party settlement services, the loan originator must provide the borrower with a written list of settlement services providers at the time of the GFE, on a separate sheet of paper.

Block 3, “Required services that we select.” - In this block, the loan originator must identify each third party settlement service required and selected by the loan originator (excluding title services), along with the estimated price to be paid to the provider of each service. Examples of such third party settlement services might include provision of credit reports, appraisals, flood checks, tax services, and any upfront mortgage insurance premium. The loan originator must identify the specific required services and provide an estimate of the price of each service. Loan originators are also required to add the individual charges disclosed in this block and place that total in the column of this block. The charge shown in this block is subject to an overall 10 percent tolerance as described above.

Block 4, “Title services and lender's title insurance.” - In this block, the loan originator must state the estimated total charge for third party settlement service providers for all closing services, regardless of whether the providers are selected or paid for by the borrower, seller, or loan originator. The loan originator must also include any lender's title insurance premiums, when required, regardless of whether the provider is selected or paid for by the borrower, seller, or loan originator. All fees for title searches, examinations, and endorsements, for example, would be included in this total. The charge shown in this block is subject to an overall 10 percent tolerance as described above.

Block 5, “Owner's title insurance.” - In this block, for all purchase transactions the loan originator must provide an estimate of the charge for the owner's title insurance and related endorsements, regardless of whether the providers are selected or paid for by the borrower, seller, or loan originator. For non-purchase transactions, the loan originator may enter “NA” or “Not Applicable” in this Block. The charge shown in this block is subject to an overall 10 percent tolerance as described above.

Block 6, “Required services that you can shop for.” - In this block, the loan originator must identify each third party settlement service required by the loan originator where the borrower is permitted to shop for and select the settlement service provider (excluding title services), along with the estimated charge to be paid to the provider of each service. The loan originator must identify the specific required services (e.g., survey, pest inspection) and provide an estimate of the charge of each service. The loan originator must also add the individual charges disclosed in this block and place the total in the column of this block. The charge shown in this block is subject to an overall 10 percent tolerance as described above.

Block 7, “Government recording charge.” - In this block, the loan originator must estimate the State and local government fees for recording the loan and title documents that can be expected to be charged at settlement. The charge shown in this block is subject to an overall 10 percent tolerance as described above.

Block 8, “Transfer taxes.” - In this block, the loan originator must estimate the sum of all State and local government fees on mortgages and home sales that can be expected to be charged at settlement, based upon the proposed loan amount or sales price and on the property address. A zero tolerance applies to the sum of these estimated fees.

Block 9, “Initial deposit for your escrow account.” - In this block, the loan originator must estimate the amount that it will require the borrower to place into a reserve or escrow account at settlement to be applied to recurring charges for property taxes, homeowner's and other similar insurance, mortgage insurance, and other periodic charges. The loan originator must indicate through check boxes if the reserve or escrow account will cover future payments for all tax, all hazard insurance, and other obligations that the loan originator requires to be paid as they fall due. If the reserve or escrow account includes some, but not all, property taxes or hazard insurance, or if it includes mortgage insurance, the loan originator should check “other” and then list the items included.

Block 10, “Daily interest charges.” - In this block, the loan originator must estimate the total amount that will be due at settlement for the daily interest on the loan from the date of settlement until the first day of the first period covered by scheduled mortgage payments. The loan originator must also indicate how this total amount is calculated by providing the amount of the interest charges per day and the number of days used in the calculation, based on a stated projected closing date.

Block 11, “Homeowner's insurance.” - The loan originator must estimate in this block the total amount of the premiums for any hazard insurance policy and other similar insurance, such as fire or flood insurance that must be purchased at or before settlement to meet the loan originator's requirements. The loan originator must also separately indicate the nature of each type of insurance required along with the charges. To the extent a loan originator requires that such insurance be part of an escrow account, the amount of the initial escrow deposit must be included in Block 9.

Line B, “Your Charges for All Other Settlement Services.” - The loan originator must add the numbers in Blocks 3 through 11 and enter this subtotal in the column at highlighted Line B.

Line A + B, “Total Estimated Settlement Charges.” - The loan originator must add the subtotals in the right-hand column at highlighted Lines A and B and enter this total in the column at highlighted Line A + B.

Page 3

“Instructions”

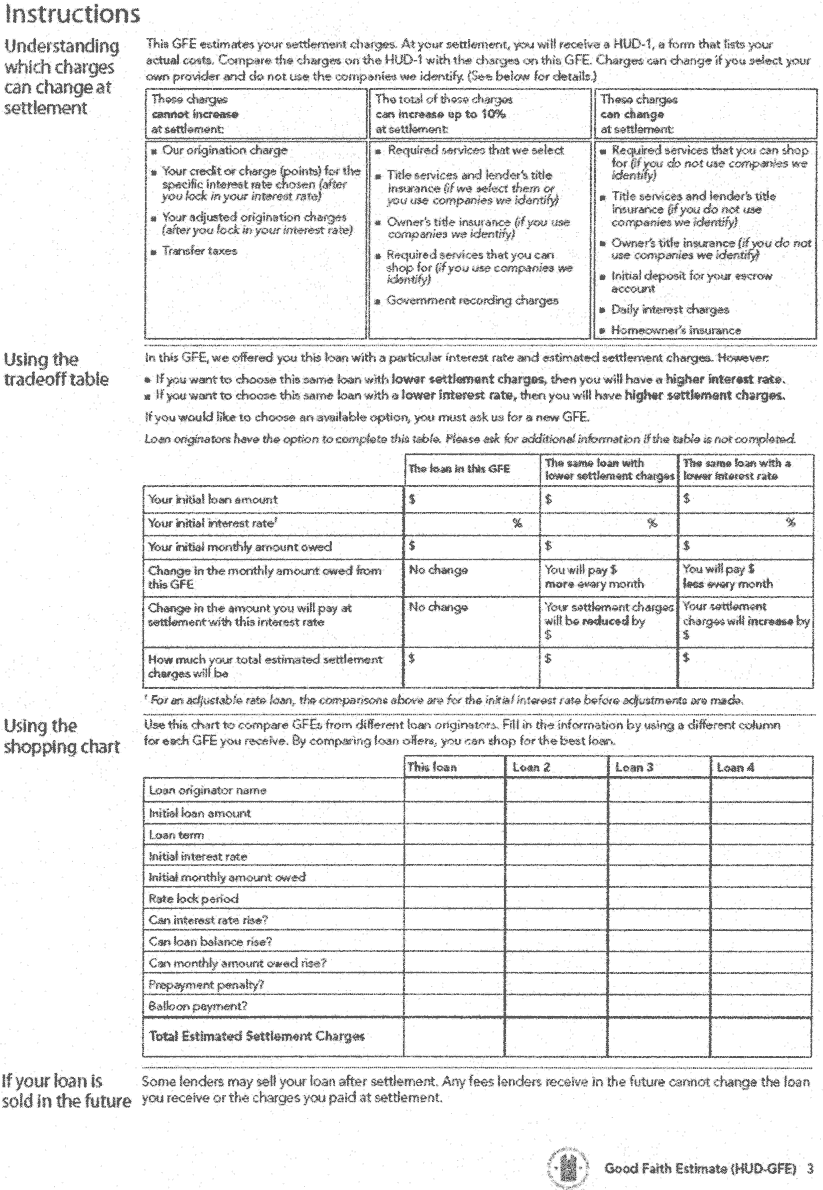

“Understanding which charges can change at settlement.” - This section informs the applicant about which categories of settlement charges can increase at closing, and by how much, and which categories of settlement charges cannot increase at closing. This section requires no loan originator action.

“Using the tradeoff table.” - This section is designed to make borrowers aware of the relationship between their total estimated settlement charges on one hand, and the interest rate and resulting monthly payment on the other hand. The loan originator must complete the left hand column using the loan amount, interest rate, monthly payment figure, and the total estimated settlement charges from page 1 of the GFE. The loan originator, at its option, may provide the borrower with the same information for two alternative loans, one with a higher interest rate, if available, and one with a lower interest rate, if available, from the loan originator. The loan originator should list in the tradeoff table only alternative loans for which it would presently issue a GFE based on the same information the loan originator considered in issuing this GFE. The alternative loans must use the same loan amount and be otherwise identical to the loan in the GFE. The alternative loans must have, for example, the identical number of payment periods; the same margin, index, and adjustment schedule if the loans are adjustable rate mortgages; and the same requirements for prepayment penalty and balloon payments. If the loan originator fills in the tradeoff table, the loan originator must show the borrower the loan amount, alternative interest rate, alternative monthly payment, the change in the monthly payment from the loan in this GFE to the alternative loan, the change in the total settlement charges from the loan in this GFE to the alternative loan, and the total settlement charges for the alternative loan. If these options are available, an applicant may request a new GFE, and a new GFE must be provided by the loan originator.

“Using the shopping chart.” - This chart is a shopping tool to be provided by the loan originator for the borrower to complete, in order to compare GFEs.

“If your loan is sold in the future.” - This section requires no loan originator action.

[76 FR 78981, Dec. 20, 2011, as amended at 78 FR 80105, Dec. 31, 2013]