-

Start Preamble

Start Printed Page 87734

AGENCY:

Federal Deposit Insurance Corporation (FDIC).

ACTION:

Final rule.

SUMMARY:

The FDIC is adopting a final rule to facilitate prompt payment of FDIC-insured deposits when large insured depository institutions fail. The final rule requires each insured depository institution that has two million or more deposit accounts to (1) configure its information technology system to be capable of calculating the insured and uninsured amount in each deposit account by ownership right and capacity, which would be used by the FDIC to make deposit insurance determinations in the event of the institution's failure, and (2) maintain complete and accurate information needed by the FDIC to determine deposit insurance coverage with respect to each deposit account, except as otherwise provided.

DATES:

Effective April 1, 2017.

Start Further InfoFOR FURTHER INFORMATION CONTACT:

Marc Steckel, Deputy Director, Division of Resolutions and Receiverships, 571-858-8224; Teresa J. Franks, Associate Director, Division of Resolutions and Receiverships, 571-858-8226; Shane Kiernan, Counsel, Legal Division, 703-562-2632; Karen L. Main, Counsel, Legal Division, 703-562-2079.

End Further Info End Preamble Start Supplemental InformationSUPPLEMENTARY INFORMATION:

I. Policy Objectives

With this final rule (“final rule”), the FDIC adopts regulatory requirements that will facilitate the FDIC's prompt payment of deposit insurance after the failure of insured depository institutions (“IDIs”) with two million or more deposit accounts. These institutions are typically large and complex. By law, the FDIC must pay deposit insurance “as soon as possible” after an IDI fails while also resolving the IDI in the manner least costly to the Deposit Insurance Fund (“DIF”).[1] The FDIC believes that prompt payment of deposit insurance is essential to the FDIC's mission for several reasons. First, prompt payment of deposit insurance maintains public confidence in the FDIC, the banking system and overall financial stability. Second, facilitating prompt access to insured funds for depositors enables them to meet their financial needs and obligations. A delay in the payment of deposit insurance—especially in the case of the failure of one of the largest IDIs—could harm the entire financial system and national economy. For example, the failure of such a large IDI could cause disruptions to check clearing processes, direct debit arrangements, or other payment system functions. Third, prompt payment can help to avoid a reduction in franchise value by expanding options for resolution thereby decreasing potential losses to the DIF. Fourth, the final rule seeks to promote long term stability in the banking system by reducing moral hazard.

The final rule is expected to significantly reduce the difficulties the FDIC would face in making prompt deposit insurance determinations at the largest IDIs. While the FDIC is authorized to rely upon the deposit account records of a failed IDI to determine deposit insurance coverage, the institution's records can be voluminous and inconsistent. Moreover, they may be incomplete for deposit insurance purposes. Consolidation of the banking industry has resulted in larger institutions that have more complex information technology systems (“IT systems”) and data management challenges. The final rule generally requires IDIs with two million or more deposit accounts (“covered institutions”) to maintain complete and accurate depositor information and to configure their IT systems in a manner that permits the FDIC to calculate deposit insurance coverage promptly in the event of failure.

The final rule will facilitate consideration of the full range of resolution options that can be invoked by the FDIC to resolve a covered institution in a manner that satisfies the least-cost resolution requirement. These resolution methods include: Purchase-and-assumption transactions; establishment of bridge depository institutions; and payout and liquidation, in which the FDIC pays depositors the insured amount of their deposits and liquidates the failed IDI's assets to pay remaining claims. Expanding the range of resolution options and including those that impose losses on uninsured depositors can also improve market discipline.

In order to resolve a bank under the least-cost requirement, the FDIC must be able to estimate the cost to the DIF of each possible resolution type. As part of this estimate, the FDIC must be able to rapidly identify insured versus uninsured deposits. Insufficient information about a bank's insured deposits and the difficulties posed in identifying relationships between deposit accounts at the time of closing, due in part to the large volume of deposit accounts managed by the institution, may impede the FDIC's ability to meet the least-cost requirement or to ensure timely access to insured funds.

Covered institutions often use multiple deposit systems, which complicates deposit insurance determinations. Depending on the structure of the deposit systems, data aggregation and account identification may be burdensome, inefficient, and time-consuming, all adding to the cost of resolution. For certain types of deposit accounts, depositors need daily access to funds, so prompt payment is essential to providing confidence and maintaining financial stability. While challenges resulting from incomplete information are present when any bank fails, obtaining the necessary information could significantly delay the availability of funds when information is incomplete for a large number of accounts. Such delays could lead to a decrease in public confidence in the FDIC's deposit insurance program. Ensuring the swift availability of funds for millions of depositors at a large institution promotes financial stability by increasing confidence in deposit insurance and availability of funds.

Another of the final rule's policy objectives is that depositors at both large and small failed banks receive the same prompt access to their deposits with full recognition of and respect for the deposit insurance limits, which should reduce potential disparities that might undermine market discipline or create unintended competitive advantages in the deposit market. Confidence in the ability of the FDIC to promptly determine insured amounts and provide access to insured deposits should help uninsured depositors realize that they may face losses in a large bank failure. This realization should mitigate moral hazard and help to curtail excessive risk taking on the part of the largest banks.

II. Background

A. Legal Authority

The FDIC is authorized to prescribe rules and regulations as it may deem necessary to carry out the provisions of the Federal Deposit Insurance Act (“FDI Act”).[2] Under the FDI Act, the FDIC is responsible for paying deposit insurance “as soon as possible” following the Start Printed Page 87735failure of an IDI.[3] It must also implement the resolution of a failed IDI at the least cost to the DIF.[4] To pay deposit insurance, the FDIC uses a failed IDI's records to aggregate the amounts of all deposits that are maintained by a depositor in the same right and capacity and then applies the standard maximum deposit insurance amount (“SMDIA”) of $250,000.[5] As authorized by law, the FDIC generally relies on the failed institution's deposit account records to identify deposit owners and the right and capacity in which deposits are maintained.[6] The FDIC has a right and a duty under section 7(a)(9) of the FDI Act to take action as necessary to ensure that each IDI maintains, and the FDIC receives on a regular basis from such IDI, information on the total amount of all insured deposits, preferred deposits, and uninsured deposits at the institution.[7] Requiring covered institutions to maintain complete and accurate records regarding the ownership and insurability of deposits and to have an IT system that can be used to calculate deposit insurance coverage in the event of failure will facilitate the FDIC's prompt payment of deposit insurance and enhance the ability to implement the least costly resolution of these institutions.

B. Current Regulatory Approach

Although the statutory requirement that the FDIC pay insurance “as soon as possible” does not specify a time period for paying insured depositors, the FDIC strives to pay depositors promptly in the event of an IDI's failure. Indeed, the FDIC strives to make most insured deposits available to depositors by the next business day after a bank fails. For the reasons set forth earlier, the FDIC believes that prompt payment of deposit insurance is essential.

The FDIC took an initial step toward ensuring that prompt deposit insurance determinations could be made at large IDIs through the issuance of § 360.9 of the FDIC's regulations.[8] Section 360.9 applies to IDIs with at least $2 billion in domestic deposits and at least 250,000 deposit accounts or $20 billion in total assets.[9] Currently, there are 155 IDIs that meet those criteria. Section 360.9 requires these institutions to be able to provide the FDIC with standard deposit account information that can be used in the event of the institution's failure. The appendices to 12 CFR part 360 prescribe the form and content of the data files that those institutions must provide to the FDIC. Section 360.9 also requires these institutions to maintain the technological capability to automatically place (and later release) provisional holds on deposit accounts if an insurance determination could not be made by the FDIC by the next business day after failure. Additionally, large volumes of deposit account data must be transferred from the IDI to the FDIC pursuant to § 360.9, which could cause further delay.

While § 360.9 would assist the FDIC in fulfilling its legal mandates regarding the resolution of a failed institution that is subject to that rule, the FDIC believes that if the largest of depository institutions were to fail with little prior warning, additional measures would be needed to ensure the prompt and accurate payment of deposit insurance to all depositors.

C. Need for Further Rulemaking

The FDIC is authorized to rely upon the deposit account records of a failed IDI to determine the amount of deposit insurance available on each account. However, in the FDIC's experience, it is not unusual for a failed bank's records to be ambiguous or incomplete. For example, an account may be titled as a joint account but may not qualify to be insured as a joint account because signature cards are missing or have not been signed by all joint account holders. A further complication is that bank records on trust accounts are often in paper form or electronically scanned images that require a time-consuming manual review.

In addition to problems with ambiguity or incompleteness of an institution's records, it is also possible that an institution simply is not required to maintain record of the beneficial owners of deposits with respect to certain types of deposit accounts under the existing regulatory framework. For example, under part 330, a deposit may be insured even if record of beneficial ownership is maintained outside of the IDI by an agent or third party that has been designated to maintain such record.

Under each of these circumstances, in order to ensure the accurate payment of deposit insurance without imposing risk of overpayment by the DIF, the FDIC would need to delay the payment of deposit insurance while it manually reviews files and obtains additional information. Such delays in the insurance determination process could increase the likelihood of disruptions to an assuming institution's or an FDIC-managed bridge depository institution's payment processing functions, such as clearing checks and authorizing direct debits.

While these challenges to accurately determining and promptly paying deposit insurance may be present at any size of failed institution, they become increasingly formidable as the size and complexity of the institution increases. Larger institutions are generally more complex, have more deposit accounts, greater geographic dispersion, multiple deposit systems, and more issues with data accuracy and completeness. The largest IDIs which grew through acquisition have inherited the legacy recordkeeping and deposit account systems of the acquired banks. Those systems might have inaccurate or incomplete deposit account records. Additionally, acquired records might not be automated or compatible with the acquiring institution's deposit systems, resulting in use of multiple deposit platforms.

Although some of the largest institutions are able to conduct their banking operations without integrating these inherited systems or updating the acquired deposit account records, the state of their deposit systems would complicate and prolong the deposit insurance determination process in the event of failure. Because of the potential problems posed by delays in determination and payment of deposit insurance, improved strategies must be implemented to ensure that deposit insurance can be paid promptly.

The FDIC's experiences during the most recent financial crisis, which peaked in the months following the promulgation of § 360.9, indicated that failures can often happen with very little notice and time for the FDIC to prepare. Since 2009, the FDIC was called upon to resolve 47 institutions with 30 days or less to plan the resolution (which includes review of deposit account records). While these 47 institutions were smaller, the financial condition of two banks with a very large number of deposit accounts—Washington Mutual Bank and Wachovia—deteriorated very quickly, also leaving the FDIC little time to prepare.[10] If a large bank were to fail because of liquidity problems rather than capital deterioration, for example, the FDIC would anticipate having less lead time to prepare to make deposit insurance determinations, which could result in the need for more time post-Start Printed Page 87736failure and less prompt payment of deposit insurance.

The FDIC has worked with institutions covered by § 360.9 for several years to confirm their ability to comply with that rule's requirements. This implementation process has led the FDIC to conclude that the standard data sets and other requirements of § 360.9 are not sufficient to mitigate the complexities presented in the failure of the largest institutions. Based on its experience reviewing deposit data (and often finding inaccurate or incomplete data), deposit recordkeeping systems, and capabilities for imposing provisional holds in the course of its § 360.9 compliance visits, the FDIC believes that § 360.9 has not been as effective as intended in enhancing the capacity of the FDIC to make prompt deposit insurance determinations necessary for the largest IDIs. Specifically, the continued growth in the number of deposit accounts at larger IDIs and the number and complexity of deposit systems used by many of these institutions since the promulgation of § 360.9 would exacerbate the difficulties present in making prompt deposit insurance determinations. Additionally, the institutions covered by § 360.9 are permitted discretion when populating the data fields that often results in missing information.

A failed IDI that has multiple deposit systems would further complicate the aggregation of deposits by depositor in a particular right and capacity, causing additional delay. Additionally, deposit taking practices have evolved, and innovative products and services have proliferated throughout the financial services markets. Customer use of deposit accounts has changed. Accounts that may have been used in the past as traditional savings vehicles are now used more frequently for transactional purposes. For example, checking accounts held in connection with a formal revocable trust are used to pay for everyday living expenses. Brokered deposits are sometimes held in money market deposit accounts (“MMDAs”).

Using the FDIC's IT system to make deposit insurance determinations at a failed institution with a large number of deposit accounts would require the transmission of massive amounts of deposit data from the IDI's IT system to the FDIC's IT system. The transfer of such a large volume of data would be very time consuming and the time required for processing that data would present a significant impediment to making deposit insurance determinations in the timely manner that the public has come to expect. The 38 institutions currently covered by the final rule each have between 2 million and 87 million deposit accounts as of June 30, 2016. Requiring these covered institutions to enhance their deposit account data and upgrade their IT systems so that the FDIC can promptly determine deposit insurance available on most deposit accounts using the covered institutions' IT systems would help to resolve the timing issues presented when transferring and processing such a large volume of deposit data.

Advance Notice of Proposed Rulemaking

On April 28, 2015, the FDIC published in the Federal Register an Advance Notice of Proposed Rulemaking (“ANPR”) seeking comment on whether certain IDIs such as those that have two million or more deposit accounts should be required to take steps to ensure that depositors would have access to their FDIC-insured funds in a timely manner (usually within one business day of failure) if one of these institutions were to fail.[11] Specifically, the FDIC sought comment on whether these IDIs should be required to enhance their recordkeeping to maintain and be able to provide substantially more accurate and complete data on each depositor's ownership interest by right and capacity for all or a large subset of the institution's deposit accounts. The FDIC sought comment on whether these IDIs' IT systems should have the capability to calculate the insured and uninsured amounts for each depositor by deposit insurance right and capacity for all or a substantial subset of deposit accounts at the end of any business day. The FDIC also sought comment on the potential costs and benefits associated with instituting such requirements. The comment period ended on July 27, 2015. The FDIC received 10 comment letters. The FDIC also had six meetings or conference calls with banks, trade groups, and software providers.

Notice of Proposed Rulemaking

Following the ANPR, the FDIC developed and then published in the Federal Register a notice of proposed rulemaking entitled “Recordkeeping for Timely Deposit Insurance Determination” soliciting public comment on its proposal to require each IDI with two million or more deposit accounts to maintain complete and accurate information needed to allow the FDIC to determine promptly the deposit insurance coverage for each deposit account, and to have an IT system that is capable of calculating the insured and uninsured amounts for all deposit accounts in accordance with the FDIC's deposit insurance rules set forth in 12 CFR part 330 (the “NPR” for the “proposed rule”).[12] Under the proposed rule, each covered institution's IT system would facilitate the FDIC's deposit insurance determination by being able to calculate deposit insurance coverage for each deposit account and adjust account balances to the insured amount within 24 hours after the appointment of the FDIC as receiver should the covered institution fail. Relief from the proposed rule's requirements would have come in the form of: An extension of the implementation deadlines; an exception from the information collection requirements for certain deposit accounts or types of deposit accounts if conditions for exception could be met; exemption from all of the proposed rule's requirements if all the deposits a covered institution takes are fully insured; or release from all of the proposed rule's requirements when a covered institution no longer meets the definition of a covered institution. Each covered institution would need to certify compliance with the proposed rule annually, with enforcement measures to be taken in accordance with § 8 of the FDI Act, if necessary.

The NPR's comment period expired on June 27, 2016. The FDIC received 14 comment letters in total from IDIs, industry trade associations, financial intermediaries, mortgage servicing companies, technology firms, an industry consultant, and an individual. In addition, FDIC staff participated in meetings or conference calls with industry representatives. The FDIC considered all of the comments it received when developing the final rule, and the comments and the FDIC's responses are discussed in VI. Discussion of Comments.

III. Description of the Final Rule

A. Summary

The scope of the final rule is unchanged from the NPR. It applies to any IDI that has two million or more deposit accounts, defined as a “covered institution.” As contemplated by the proposed rule, under the final rule, each covered institution must configure its IT system to be capable of accurately calculating the deposit insurance available for each deposit account in accordance with the FDIC's deposit insurance rules set forth in 12 CFR part 330 should the covered institution fail. Start Printed Page 87737The FDIC would use the covered institution's IT system to facilitate the deposit insurance determinations in the event of the covered institution's failure.

In order for the FDIC to effectively use the covered institution's IT system to calculate deposit insurance, the covered institution's deposit account records must contain certain information concerning the identity of the owner of the funds on deposit and details about the right and capacity in which the deposit is held for deposit insurance purposes. The proposed rule would have required covered institutions to maintain this information in their deposit account records for all accounts unless the FDIC granted the covered institution an exception from this requirement. In light of comments received in response to the NPR, the final rule modifies this approach. Recognizing that insured depository institutions do not maintain all information needed for deposit insurance determination in their deposit account records for every account, along with the significant challenges associated with collecting that information, the FDIC has bifurcated the recordkeeping requirement.

Under the final rule's general recordkeeping requirements, a covered institution will need to ensure that its deposit account records contain the information needed for its IT system to be able to calculate deposit insurance coverage for those deposit accounts for which it already maintains the necessary information. A covered institution should, in the normal course of business, already maintain in its deposit account records the information necessary to do this for: Single ownership accounts; joint ownership accounts; accounts held by a corporation, partnership, or unincorporated association for themselves; informal revocable trust (i.e., “payable-on-death” or “in-trust-for”) accounts; and any account of an irrevocable trust for which the covered institution itself is the trustee.

The final rule recognizes that, under the FDIC's deposit insurance rules set forth in 12 CFR part 330, the amount of deposit insurance available may not be determinable without reference to information that an IDI does not, and is not otherwise required to, maintain in its deposit account records under the existing regulatory framework. After an IDI fails, this information must be provided to the FDIC so that the FDIC can determine the full amount of deposit insurance available. Accordingly, under the final rule, a covered institution does not need to meet the general recordkeeping requirements described in this section, but may instead meet alternative recordkeeping requirements with respect to certain types of deposit accounts for which it is not required under 12 CFR part 330 to maintain in its deposit account records the information that would be needed for the FDIC to determine the full amount of deposit insurance coverage. Certain additional provisions apply to deposit accounts with transactional features.

To meet the alternative recordkeeping requirements, the covered institution must maintain in its deposit account records certain information that will facilitate the FDIC's prompt collection of the information needed to determine deposit insurance with respect to those deposit accounts after its failure. These alternative recordkeeping requirements apply to deposit accounts that would be insured on a “pass-through” basis (such as brokered deposits) because beneficial owner information is not maintained by the covered institution, and to deposit accounts for which the amount of insurance is dependent on additional facts (such as deposit accounts held in connection with a trust). The FDIC also recognizes that it may not always be feasible for a covered institution to maintain information in its deposit account records needed to calculate the deposit insurance with respect to official items prior to presentment and, therefore, if the information needed for deposit insurance calculation is not available, the covered institution will need to maintain in its deposit account records certain information that will facilitate the FDIC's deposit insurance determination after the failure of a covered institution.

For deposit accounts with “transactional features” for which the covered institution maintains its deposit account records in accordance with the alternative recordkeeping requirements set forth in § 370.4(b)(1), a covered institution must certify that the information needed to calculate deposit insurance coverage will be submitted to the FDIC so that deposit insurance can be determined within 24 hours after the appointment of the FDIC as receiver. The FDIC has been concerned about timely deposit insurance determinations for accounts with transactional features since the inception of this rulemaking process. One of the options presented in the ANPR was that “[f]or a large subset of deposits (“closing night deposits”), including those where depositors have the greatest need for immediate access to funds (such as transaction accounts and money market deposit accounts (“MMDAs”), deposit insurance determinations would be made on closing night.” [13] The FDIC acknowledged that the concept of “closing night deposits” served as a proxy for those deposit accounts for which depositors would expect immediate access to their funds on the next business day. The ANPR explained that in order to make deposit insurance determinations on closing night, the covered institutions would be required to: “Obtain and maintain data on all closing night deposits . . . at the end of any business day (since failure can occur on any business day).” [14] The ANPR solicited comment from the banking industry regarding what types of deposits should be considered as “closing night deposits.”

After reviewing the comments received on the ANPR, the FDIC concluded that there really was no consensus among the potentially covered institutions regarding what types of deposits could be designated as “closing night deposits.” As a result, the FDIC adopted the approach in the proposed rule that, generally, covered institutions would need to collect and maintain the necessary depositor information for all deposit accounts unless the conditions for exception could be satisfied. Then, the FDIC would have all the depositor information necessary to begin the deposit insurance determinations immediately upon the covered institution's failure. However, in response to the commenters' objections to the proposed rule's approach, the FDIC developed the bifurcated approach set forth in the final rule. In this way, the final rule is consistent with the recordkeeping standards established in §§ 330.5 and 330.7; i.e., the deposit records for certain types of deposit accounts may be maintained off-site and with third parties rather than at the covered institution. Nevertheless, the requisite beneficial ownership information for those accounts must be made available to the FDIC so that the deposit insurance determination can be completed during the closing night process. The FDIC believes that requiring covered institutions to certify that the information needed to calculate deposit insurance coverage for certain deposit accounts with transactional features will be submitted to the FDIC by the respective account holder in time for the calculation to be performed within 24 hours after the appointment of the FDIC as receiver is important to ensure that the FDIC can make deposit insurance determinations expeditiously Start Printed Page 87738after failure of a covered institution to avoid delays in payment processing.

The proposed rule would have provided a two-year timeframe for implementation of IT system and recordkeeping requirements. Under the final rule, a covered institution has three years after the effective date for implementation and can apply to the FDIC for extension of that timeframe.

B. Section-by-Section Description of the Final Rule

1. Section 370.1 Purpose and Scope

The purpose of the final rule is to help the FDIC overcome the challenges it faces when fulfilling its statutory mandate to pay deposit insurance as soon as possible after the failure of an IDI with millions of deposit accounts at the least cost to the DIF. These challenges become more pronounced as the number of deposit accounts at an IDI rises above two million. Moreover, the number of deposit accounts is highly correlated with other attributes that contribute to this challenge, such as the complexity of account relationships and the use of multiple deposit systems by these institutions. Accordingly, the final rule requires IDIs with two million or more deposit accounts to configure their IT systems to be capable of calculating the amount of deposit insurance coverage available for each deposit account in the event of failure.

2. Section 370.2 Definitions

This section provides definitions of terms that are used in the final rule. A covered institution is an IDI which, based on its Reports of Condition and Income (“Call Reports”) filed with the appropriate Federal banking agency, has two million or more deposit accounts during the two consecutive quarters preceding the effective date of the final rule or thereafter.

For purposes of the final rule, account holder is defined as the person who has opened a deposit account with a covered institution and with whom the covered institution has a direct legal and contractual relationship with respect to the deposit. An account holder is often, but not always, the person who actually owns deposits in a deposit account, and to whom deposit insurance inures under the FDIC's deposit insurance rules set forth in 12 CFR part 330. The person who actually owns the deposits is commonly referred to as the “beneficial owner” of a deposit or as the “principal.” When the account holder does not have ownership rights to deposits, it is typically acting as an agent, custodian, or fiduciary on behalf of the beneficial owner of the deposit. In these situations, deposit insurance coverage can “pass through” the account holder to the beneficial owner of the deposit, and the deposit would be insured to the beneficial owner based on the deposit insurance right and capacity in which those deposits are owned. Because the account holder is the party with whom a covered institution has a deposit account relationship, it is the account holder who will need to provide the information needed for purposes of calculating deposit insurance. For that reason, the final rule's recordkeeping requirements with respect to certain deposit accounts are framed around the relationship between the covered institution and the account holder.

Several terms are defined by reference to their statutory or regulatory definitions. Specifically, brokered deposit has the same meaning as provided in 12 CFR 337.6(a)(2); deposit has the same meaning as provided under section 3(l) of FDI Act (12 U.S.C. 1813(l)); deposit account records has the same meaning as provided in 12 CFR 330.1(e); and standard maximum deposit insurance amount (or “SMDIA”) has the same meaning as provided pursuant to section 11(a)(1)(E) of the FDI Act (12 U.S.C. 1821(a)(1)(E)) and 12 CFR 330.1(o). Ownership rights and capacities are set forth in 12 CFR part 330.

Compliance date means the date that is three years after the later of the effective date of this part or the date on which an IDI becomes a covered institution. In response to the NPR, commenters had suggested that a four-year implementation period be provided. In light of the bifurcated approach to recordkeeping taken in the final rule, the FDIC believes that a three-year implementation period will be sufficient.

Payment instrument means a check, draft, warrant, money order, traveler's check, electronic instrument, or other instrument, payment of funds, or monetary value (other than currency). This definition is consistent with § 1002(18) of the Consumer Financial Protection Act of 2010 (12 U.S.C. 5481(18)) and common banking usage.

Transactional features, with respect to a deposit account, means that the depositor or account holder can make transfers or withdrawals from the deposit account to make payments or transfers to third persons or others (including another account of the depositor or account holder at the same institution or at a different institution) by means of a negotiable or transferable instrument, payment order of withdrawal, check, draft, prepaid account access device, debit card, or other similar order made by the depositor and payable to third parties, or by means of a telephonic (including data transmission) agreement, order or instruction, or by means of an instruction made at an automated teller machine or similar terminal or unit. For purposes of this definition, “telephonic (including data transmission) agreement, order or instruction” includes orders and instructions made by means of facsimile, computer, internet, handheld device, or other similar means. When interpreting this definition, the FDIC will consider the frequency with which a depositor or account holder may make transfers or withdrawals with respect to a deposit account, in addition to other account features. For example, an account comprised of time deposits will not be deemed to have transactional features solely because it allows a depositor or account holder who is not the beneficial owner to redeem or withdraw the time deposit and transfer the proceeds on a one-time basis to the beneficial owner.

Unique identifier means an alpha-numeric code associated with an individual or entity that is used by a covered institution to monitor its relationship with only that individual or entity. The unique identifier may be, but is not required to be, a government-issued identification number such as a social security number or tax identification number. It could also be a customer identification number already in use by the covered institution for other operational or regulatory purposes.

3. Section 370.3 Information Technology System Requirements

As was proposed in the NPR, each covered institution is required to configure its IT system to be capable of accurately calculating the deposit insurance available to each beneficial owner of funds on deposit in accordance with the FDIC's deposit insurance rules set forth in 12 CFR part 330. Additionally, the IT system must be able to adjust account balances within 24 hours after the appointment of the FDIC as receiver. Each covered institution's IT system would need to be capable of grouping each beneficial owner's deposits within the applicable ownership right and capacity because deposit insurance is available up to the SMDIA for each ownership right and capacity in which the deposits are held. To do this, a covered institution must maintain in its deposit account records certain information, as described in § 370.4. The covered institution's IT system would also need to be able to Start Printed Page 87739generate a record that reflects the deposit insurance calculation. This record would contain, at a minimum, the name and unique identifier of the account holder or beneficial owner of a deposit if the account holder is not the beneficial owner, the balance of each beneficial owner's deposits in each deposit account grouped by ownership right and capacity, the aggregated balance of each beneficial owner's deposits within each applicable ownership right and capacity, the amount of the aggregated balance within each ownership right and capacity that is insured, and the amount of the aggregated balance within each ownership right and capacity that is uninsured. Appendix B to the final rule specifies the data format for the records that the covered institution's IT system would need to produce.

If a covered institution were to fail, its depositors' access to their funds would need to be restricted while the FDIC makes deposit insurance determinations in order to avoid overpayment. Each covered institution's IT system would need to be capable of restricting access to some or all of the funds in each deposit account until the FDIC has determined the deposit insurance coverage for that account using the covered institution's IT system.

The deposit insurance determinations for most deposit accounts would be made within 24 hours after failure and holds on those accounts would be removed. Holds would remain in place on deposit accounts for which a deposit insurance determination has not been made within that time frame and would be removed after the determination has been made.

The covered institution's IT system would need to adjust the balance in each deposit account, if necessary, after the deposit insurance determination has been completed so that only insured deposits are made available. Specifically, if any of a beneficial owner's deposits within a particular ownership right and capacity were not insured, then the covered institution's IT system would need to debit the respective deposit accounts for the uninsured amount associated with each account. To the extent that a beneficial owner of deposits is uninsured, it will have a claim against the receivership for the failed covered institution that would be paid out of the assets of the receivership on equal footing with all other deposit claims, including the FDIC's subrogated claim for insured deposits.

A covered institution's IT system would need to be capable of performing these functions for most deposit accounts within 24 hours after the FDIC's appointment as receiver should the covered institution fail, and within 24 hours after the FDIC receives from the remaining account holders the additional information needed to determine deposit insurance coverage.

The FDIC's regulations and resources concerning deposit insurance that are available to the public on the FDIC's Web site are useful tools that covered institutions can use to develop the capabilities of their IT systems to meet the final rule's requirements.[15] The FDIC also intends to offer guidance and outreach to facilitate covered institutions' efforts to meet this requirement.

4. Section 370.4 Recordkeeping Requirements

In response to commenters' recommendations, the final rule's recordkeeping requirements have been modified from those set forth in the proposed rule. While the proposed rule would have required covered institutions to collect and maintain significantly more information on deposit relationships than is currently contemplated under part 330, the final rule recognizes that such information may continue to reside in records maintained outside the covered institution by either the account holder or a party designated by the account holder, as set forth in part 330. The final rule contemplates, however, that in many instances, a covered institution will already maintain in its deposit account records the necessary information for its IT system to calculate deposit insurance coverage and therefore the institution will be capable of fulfilling the general recordkeeping requirement to maintain in its deposit account records for each account the unique identifier for the appropriate parties and the applicable ownership right and capacity code. Accordingly, § 370.4(a) imposes a general recordkeeping requirement whereby the covered institution must assign a unique identifier to each account holder, beneficial owner, grantor, and beneficiary, as appropriate, and assign the applicable ownership right and capacity code listed in Appendix A. A covered institution should, in the normal course of business, already have in its deposit account records the necessary information to do this for, among others, deposit accounts that would be insured as: single ownership accounts; joint ownership accounts; accounts owned by a corporation, partnership, or unincorporated association; informal revocable trust (i.e., “payable-on-death” or “in-trust-for”) accounts; and any account held in connection with an irrevocable trust for which the covered institution itself is the trustee.

The final rule recognizes, however, that under the FDIC's deposit insurance rules, where an IDI's deposit account records disclose the existence of a relationship that might provide a basis for additional insurance, the details of the relationship must be ascertainable from either the IDI's deposit account records or from records maintained by the depositor or by a third party that has undertaken to maintain such records for the depositor. (See 12 CFR 330.5 concerning recognition of deposit ownership and fiduciary relationships; 12 CFR 330.7 concerning accounts held by an agent, nominee, guardian, custodian, or conservator; 12 CFR 330.10 concerning revocable trust accounts; and 12 CFR 330.13 concerning irrevocable trust accounts.) Accordingly, under § 370.4(b), a covered institution may meet alternative recordkeeping requirements with respect to those types of accounts. Under the alternative recordkeeping requirements, the covered institution must maintain in its deposit account records for each deposit account where the basis for additional deposit insurance is contained in records maintained by the account holder, or a party designated by the account holder, the unique identifier for only the account holder. It must also maintain in its deposit account records information sufficient to populate the “pending reason” field of the pending file set forth in Appendix B, which is to be generated by the covered institution's IT system pursuant to § 370.3(b) of the final rule. For deposit accounts held in connection with formal trusts for which the covered institution is not trustee, the covered institution will need to maintain in its deposit account records the unique identifier of the account holder, and the unique identifier of the grantor (if the grantor is not the account holder) if the account has transactional features. The unique identifier of the grantor is needed in order to begin calculating how much deposit insurance would be available, at a minimum, on deposit accounts held in connection with a formal trust. The covered institution will also need to maintain in its deposit account records information sufficient to populate the “pending reason” field of the pending file set forth in Appendix B, which is to be Start Printed Page 87740generated by the covered institution's IT system pursuant to § 370.3(b) of the final rule.

Additionally, a covered institution will need to maintain in its deposit account records the information needed for its IT system to calculate deposit insurance coverage with respect to payment instruments drawn on an account of the covered institution (commonly referred to as “official items”), such as a cashier's check, teller's check, certified check, personal money order, or foreign draft. The FDIC recognizes that it may not always be feasible to identify the beneficial owner of such instruments and, therefore, if the necessary information is not available, the covered institution will need to maintain in its deposit account records for those accounts only the “pending reason” code to indicate that more information is needed before deposit insurance can be calculated. This will be used to populate the “pending reason” field of the pending file set forth in Appendix B, which is to be generated by the covered institution's IT system pursuant to § 370.3(b) of the final rule.

To the extent that a covered institution does not meet the recordkeeping requirements set forth in § 370.4(a) and instead meets the alternative recordkeeping requirements set forth in § 370.4(b), it must take the additional action set forth in § 370.5 with respect to those deposit accounts that have transactional features.

5. Section 370.5 Actions Required for Certain Deposit Accounts With Transactional Features

The FDIC is concerned that many deposit accounts held in the name of someone other than the beneficial owner of the deposit (such as an agent, nominee, custodian, fiduciary, or other third party) are relied upon for transactions. In the case of a failure of a covered institution, with its millions of deposit accounts, any material delay in the payment of deposit insurance could undermine public confidence in the financial system and be extremely disruptive not only for individual depositors but also for the community or region as a whole. Widespread or extended delay could even result in systemic consequences. Therefore, § 370.5(a) imposes the requirement that, with respect to deposit accounts with transactional features that are held in the name of a third party for the benefit of others, the covered institution certify that all information needed to calculate deposit insurance coverage can and will be submitted to the FDIC upon failure of the covered institution to minimize any delay in the FDIC's efforts to calculate deposit insurance within 24 hours after appointment as receiver using the covered institution's IT system. The timeframe within which this information must be received will likely need to be less than 24 hours because the covered institution's IT system will need time to process the information once received. This requirement applies not only to traditional demand and checking accounts, but also to savings deposit accounts that have transactional features, such as MMDAs, and to prepaid accounts that are entitled to deposit insurance coverage. The final rule provides, however, that this certification requirement does not apply with respect to mortgage servicing accounts, lawyers trust accounts, real estate trust accounts, or accounts held by employee benefits plans. A covered institution that is unable to provide this certification must apply to the FDIC for an exception from the certification requirement. In addition, the final rule makes clear that a covered institution's failure to provide the certification shall be deemed not to constitute a violation of this part if the FDIC has granted the covered institution relief from the certification requirement.

6. Section 370.6 Implementation

This section provides that a covered institution must comply with the final rule no later than the compliance date, which is three years after the later of the effective date of the final rule or the date on which the institution becomes a covered institution by reaching the threshold of two million deposit accounts. Under § 370.6(b), a covered institution may request that the FDIC extend the implementation time period. The request must state the amount of additional time needed and the reasons therefor. It must also report the total number of, and dollar amount in, accounts for which the covered institution's IT system could not calculate deposit insurance coverage if the covered institution were to fail as of the date of the request.

7. Section 370.7 Accelerated Implementation

The final rule provides for accelerated implementation on a case-by-case basis and after notice from the FDIC to a covered institution in three scenarios. The first would be when a covered institution has received a composite rating of 3, 4, or 5 under the Uniform Financial Institution's Rating System (CAMELS rating) in its most recently completed Report of Examination. The second scenario would be when a covered institution has become undercapitalized, as defined in the prompt corrective action provisions of 12 CFR part 325. The third would be when the appropriate Federal banking agency or the FDIC, in consultation with the appropriate Federal banking agency, has determined that a covered institution is experiencing a significant deterioration of capital or significant funding difficulties or liquidity stress, notwithstanding the composite rating of the covered institution by its appropriate Federal banking agency in its most recent Report of Examination.

While the FDIC recognizes concerns about the imposition of an accelerated implementation deadline during economic distress, including the concern that a covered institution's attention might be diverted to solving critical problems that threaten its financial condition, providing depositors with immediate access to funds and preserving systemic stability is also critical. The ability to accelerate the implementation deadline must be balanced against any hardship an accelerated implementation period might impose on a covered institution. Before accelerating the implementation time period, the FDIC would consult with the covered institution's appropriate Federal banking agency. The FDIC would also evaluate the complexity of the covered institution's deposit systems and operations, the extent of the covered institution's asset quality difficulties, the volatility of the covered institution's funding sources, the expected near-term changes in the covered institution's capital levels, and other relevant factors appropriate for the FDIC's consideration as deposit insurer.

8. Section 370.8 Relief

Under § 370.8(a) of the final rule, a covered institution may submit a request to the FDIC for an exemption if it demonstrates that it has not and will not take deposits which, when aggregated, would exceed the SMDIA (currently $250,000) for any beneficial owner of the funds on deposit. In other words, if each owner of deposits were to have an amount equal to or less than the SMDIA on deposit at a covered institution, then all deposits would be fully insured. Deposit insurance determinations at failed covered institutions that meet this condition should not be complicated and, therefore, the FDIC does not believe that requiring such covered institutions to develop the capability to calculate deposit insurance coverage would be necessary.

Recognizing that circumstances may currently exist, or emerge in the future, Start Printed Page 87741for which a covered institution is unable to comply with the recordkeeping requirements set forth in § 370.4 or some particular provision therein with respect to an identified deposit account or class of deposit accounts, § 370.8(b) allows a covered institution to request an exception for those accounts. In its request letter, the covered institution must demonstrate the need for an exception, describe the impact of an exception on the ability to accurately calculate deposit insurance for the related deposit accounts, and state the number of, and the dollar value of deposits in, those deposit accounts. When reviewing the request, the FDIC would consider the implications that a delayed deposit insurance determination would have for a particular account holder or the beneficial owners of deposits, the nature of the deposit relationship, and the ability of the covered institution to obtain the information needed for an accurate calculation of deposit insurance.

A covered institution that no longer meets the criteria for being a covered institution may submit a request for release from the final rule's requirements. Section 370.8(c) provides that if the number of deposit accounts at a covered institution drops below the two million deposit account threshold for three consecutive quarters based on Schedule RC-O in the Report of Condition and Income, the institution may request release. Like any other IDI, an institution released under this paragraph would become a covered institution again if it were to have two million or more deposit accounts for two consecutive quarters.

The objectives of the final rule supersede the objectives of 12 CFR 360.9. Accordingly, if a covered institution reaches full compliance with the final rule, the results intended under § 360.9 will be largely accomplished. Paragraph (d) permits a covered institution to request a release from the requirements set forth in § 360.9 upon submission of its first certification of compliance with the final rule's requirements.

This section further provides that the FDIC will consider all requests made under relevant provisions of the final rule on a case-by-case basis in light of the final rule's objectives, and that the FDIC's grant of a covered institution's request may be conditional or time-limited.

9. Section 370.9 Communication With the FDIC

This section requires that within ten business days after either the effective date of the final rule or becoming a covered institution, whichever is later, a covered institution notify the FDIC of the person(s) responsible for implementing the recordkeeping or IT system requirements set forth in this part. Point-of-contact information, reports and requests are to be submitted in writing to: Office of the Director, Division of Resolutions and Receiverships, Federal Deposit Insurance Corporation, 550 17th Street NW., Washington, DC 20429-0002.

10. Section 370.10 Compliance

The final rule sets forth a two-part approach for compliance. First, beginning on or before the compliance date and annually thereafter, a covered institution must certify that it has implemented and successfully tested its IT system for compliance with the final rule's requirements during the preceding calendar year. The certification must be signed by the covered institution's chief executive officer or chief operating officer. Along with its certification of compliance, the covered institution must also submit a summary deposit insurance coverage report to the FDIC. The summary deposit insurance coverage report would list key metrics for evaluating deposit insurance risk to the DIF and coverage available to a covered institution's depositors. Those metrics are: The number of account holders, the number of deposit accounts, and the dollar amount of deposits by ownership right and capacity; the total number of fully-insured deposit accounts and the dollar amount of deposits in those accounts; the total number of deposit accounts with uninsured amounts and the total dollar amount of insured and uninsured amounts in those accounts; the total number of deposit accounts and the dollar amount of deposits in accounts, broken out by account type, for which the covered institution's IT system cannot calculate deposit insurance coverage because it is permitted to maintain alternative recordkeeping requirements as set forth in § 370.4(b); and a description of any substantive change to the covered institution's IT system or deposit taking operations since the prior annual certification.

Second, the FDIC will conduct periodic on-site inspections and tests of each covered institution's IT system's capability to accurately calculate deposit insurance coverage in the event of failure. Testing will begin no sooner than the last day of the first calendar quarter following the compliance date, and will occur no more frequently than on a three-year cycle thereafter, unless there is a material change to the covered institution's IT system, deposit-taking operations, or financial condition. The FDIC will provide data integrity and IT system testing instructions to covered institutions through the issuance of procedures or guidelines prior to the final rule's effective date and before initiating its compliance testing program, and will provide outreach to covered institutions to facilitate their implementation efforts. The final rule also requires covered institutions to assist the FDIC in resolving any issues that arise upon the FDIC's on-site inspection and testing of the IT system's capabilities.

The final rule provides that a covered institution will not be in violation of any requirements of the rule for which the institution has submitted a request for relief pursuant to § 370.6(b) or § 370.8(a)-(c) while awaiting the FDIC's response to the request.

IV. Expected Effects

Using current data, the FDIC estimates that the rule will apply to 38 institutions, each with two million or more deposit accounts.[16] Together, these institutions hold more than $10 trillion in total assets and manage over 400 million deposit accounts.

The FDIC has evaluated the estimated cost to implement this rule, as well as the benefits to the FDIC's resolution process and to the millions of account holders who would need immediate access to their funds in the event of failure of a covered institution. The main determinants of the estimated cost to institutions covered by the final rule are the number of deposit accounts they hold and the number of deposit IT systems they manage. Benefits of the rule include: Ensuring prompt and efficient deposit insurance determinations by the FDIC and thus the liquidity of deposit funds; enabling the FDIC to readily resolve a failed IDI; reducing the costs of failure of a covered institution by increasing the FDIC's resolution options; and promoting long term stability in the banking system by reducing moral hazard.

These benefits are expected to accrue to the public at large. However, because there is no market in which the value of these expected benefits can be determined, it is not possible to quantify these benefits with precision. As the public benefits cannot be quantified, the FDIC presents an analytical framework that describes the qualitative effects of the proposed rule and the quantitative effects where possible, consistent with Start Printed Page 87742the FDIC Statement of Policy on the Development and Review of FDIC Regulations and Policies.

Expected Costs

The FDIC's initial estimate of the cost of this rule, as described in the NPR, was approximately $328 million. The FDIC has updated its cost estimate to $478 million, based in part upon comments the FDIC received in response to the NPR. The updated estimated cost to covered institutions represents $386 million of this total, with the remaining estimated costs accruing to depositors and the FDIC. Even with these updates, the estimated costs to covered institutions remain small relative to their revenues and expenses.

In estimating the costs of this rule, the FDIC engaged the services of an independent consulting firm. Working with the FDIC, the consultant used its extensive knowledge and experience with IT systems at financial institutions to develop a model to provide cost estimates for the following activities:

- Implementing the deposit insurance calculation

- Legacy data clean-up

- Data extraction

- Data aggregation

- Data standardization

- Data quality control and compliance

- Data reporting

- Ongoing operations

Cost estimates for these activities were derived from a projection of the types of workers needed for each task, an estimate of the amount of labor hours required, an estimate of the industry average labor cost (including benefits) for each worker needed, and an estimate of worker productivity. The analysis assumed that manual data clean-up would be needed for 5 percent of deposit accounts, 10 accounts per hour would be resolved, and internal labor would be used for 60 percent of the clean-up. This analysis also projected higher costs for institutions based on the following factors:

- Higher number of deposit accounts

- Higher number of distinct core servicing platforms

- Higher number of depository legal entities or separate organizational units

- Broader geographic dispersal of accounts and customers

- Use of sweep accounts

- Greater degree of complexity in business lines, accounts, and operations

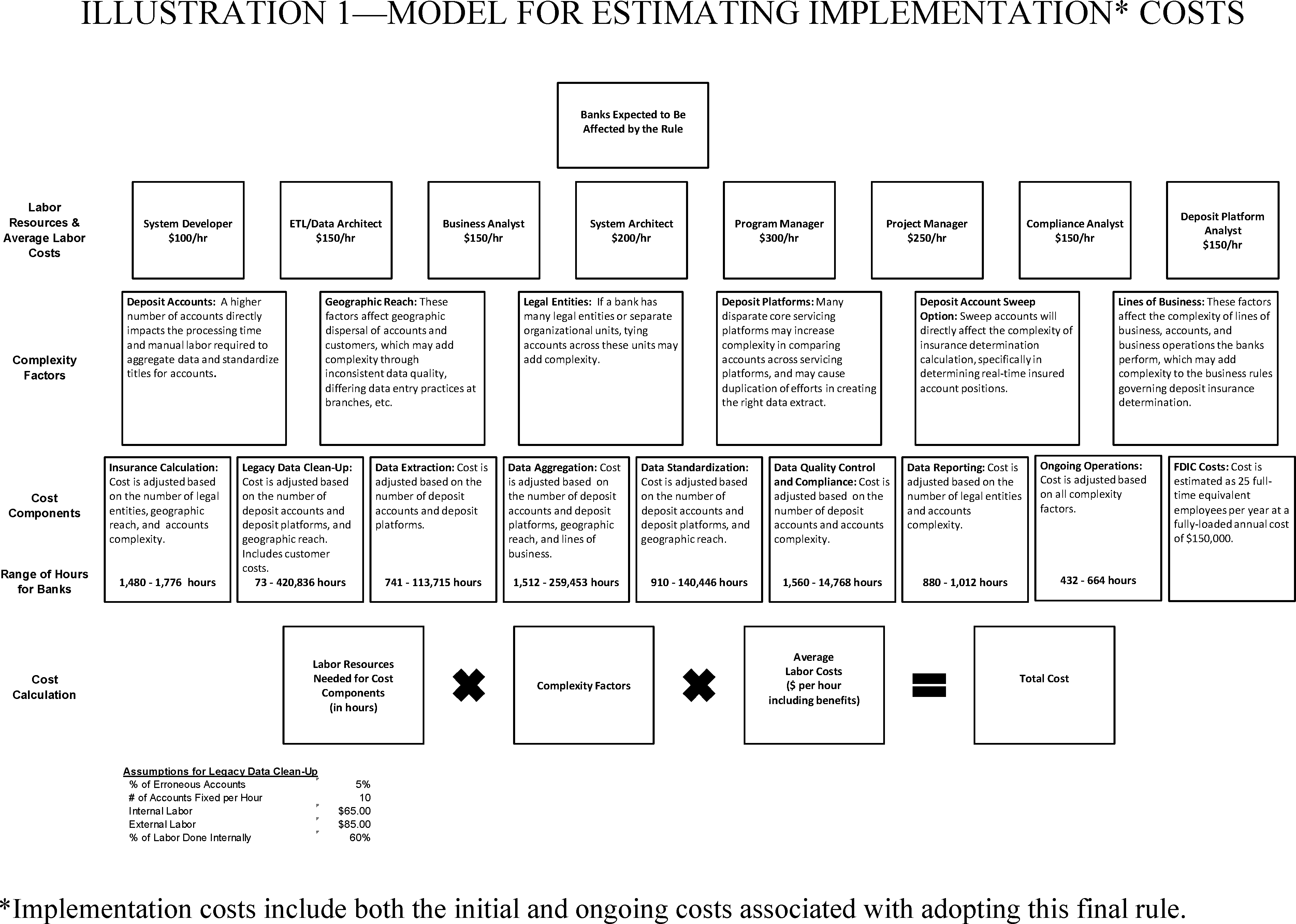

Illustration 1 provides a diagram of the cost model.

Table 1 shows that almost half of the rule's estimated total costs are attributable to legacy data clean-up. These legacy data clean-up cost estimates are sensitive to both the number of deposit accounts and the number of deposit IT systems. More than 90 percent of the legacy data clean-up costs are associated with manually collecting account information from customers and entering it into the covered institution's systems. Data aggregation, which is sensitive to the number of deposit IT systems, makes up about 13 percent of the rule's estimated costs.Start Printed Page 87743

Table 1—Estimated Implementation * Costs by Component

Components Component cost Percent of total Legacy Data Cleanup $226,482,333 47.43% Data Aggregation 64,015,373 13.41% Ongoing Operations ** 55,175,451 11.55% Data Standardization 36,573,894 7.66% FDIC Costs ** 36,001,520 7.54% Data Extraction 25,397,761 5.32% Quality Control and Compliance 18,403,006 3.85% Insurance Calculation 9,500,400 1.99% Reporting 5,971,800 1.25% Total Cost 477,521,538 100% * Estimates of bank implementation costs include both initial and ongoing costs associated with this final rule. ** Present value of annual costs using a 3.5 percent discount rate over a 30-year time horizon. For example, this discount rate is used in OMB Circular No. A-4 and A-94, Appendix C (revised November 2015 for calendar year 2016). Table 2—Comparison of Bank Implementation * Costs to Expenses

[Amounts in thousands]

[Estimated cost to covered institutions: $385,517]

Expense item 2015 Expenses for covered institutions Implementation * cost as percent of expense Noninterest Expense $260,857,965 0.15% Personnel Expense 119,069,416 0.32% Tax Expense 49,262,660 0.78% Interest Expense 26,761,300 1.44% Fixed Expense: Premises 28,446,163 1.36% Cost as Percent of Income Pre-Tax Net Income, 2015 $157,197,668 0.25% Cost per Deposit Account Number of Deposit Accounts, 2Q 2016 416,149.383 $0.93 Cost as Percent of Assets Total Assets, 2Q 2016 $10,558,645,376 0.004% * Estimates of bank implementation costs include both initial and ongoing costs associated with this final rule. These estimates of initial and ongoing costs of implementation are higher than those provided in the NPR. The increase in total estimated implementation costs is the result of updating the data, reviewing the cost methodology, and incorporating comments received on the NPR. Even with the revisions, however, the updated cost estimate does not alter the FDIC's overall assessment of the expected effects of the final rule.

The estimated total cost of the final rule remains relatively small for covered institutions. The estimated costs amount to an average of 93 cents per deposit account and one-quarter of one percent of pre-tax net income, as shown in Table 2. Banks with more serious deficiencies in their current systems or with greater complexity in their business lines, accounts, and operations are expected to incur above-average compliance costs. These estimates may overstate the costs of the final rule because some covered institutions are already undertaking efforts to improve their data quality to address their own operational concerns and to comply with other statutes and regulations.

Expected Benefits

The recent financial crisis has demonstrated that large financial institutions can fail very rapidly. The failure of a covered institution would likely involve millions of deposit insurance claims. An orderly resolution requires ready access to complete and accurate information about the insurance status of depositors. The final rule ensures that the FDIC can conduct an orderly resolution of covered institutions despite the informational challenges they pose.

Financial crises are, by their very nature, unpredictable, and unique and the likelihood, duration and magnitude of any such crisis cannot be predicted with mathematical precision. There are over $9 trillion in deposits in United States banks and the FDIC insures each qualifying account up to a maximum of $250,000, regardless of the events that unfold during any particular crisis. During the recent financial crisis, the federal government provided trillions of dollars of government support to large financial institutions.[17] Some of the Start Printed Page 87744institutions covered by this rule received government support that far exceeds the anticipated costs of this rule.

The FDIC expects that the benefits of the final rule will accrue broadly to the public at large, to bank customers, to IDIs not covered by the rule, and to the covered institutions themselves. As discussed earlier, the FDIC expects the final rule to provide significant benefits, including ensuring prompt and efficient deposit insurance determinations by the FDIC and thus the liquidity of deposit funds; enabling the FDIC to more readily resolve a failed IDI; reducing the costs of failure of a covered institution by increasing the FDIC's resolution options; and promoting long term stability in the banking system by reducing moral hazard.

The public at large will be the primary beneficiaries of the final rule. An effective failed bank resolution maintains liquidity in the economy by providing timely access to insured funds, promotes financial stability by ensuring an orderly, least costly resolution, and reduces moral hazard by recognizing deposit insurance limits (since uninsured depositors could be subject to losses even at the largest banks). Making accurate deposit insurance determinations for all insured institutions is a key component in carrying out the FDIC's mission of maintaining confidence in the banking system and minimizing costs to the DIF.

Broadly, the final rule facilitates the consideration of resolution methods that might otherwise be unavailable, enabling the FDIC to resolve a failing covered institution in the least costly manner. With more resolution options, the FDIC may be less likely to resolve a failing large institution by having another large institution absorb it; absorption by another large institution would further increase concentration among the largest banks and raise concerns about longer term financial stability. This final rule reduces the likelihood of invoking a systemic risk exception, the cost of assistance provided as the result of a failure and receivership for which the systemic risk exception has been invoked, and the associated long-term risk of increased moral hazard and damaged market discipline.[18]

Bank customers will also benefit from the final rule. Timely deposit insurance determinations will give bank customers expeditious access to insured funds to meet their transaction needs and financial obligations. Moreover, any current deficiencies in IT systems and data gathering that prevent covered institutions from identifying relationships between deposit accounts are likely to also prevent them from having the ability to quickly inform customers whether or not their deposits are insured, if asked.

IDIs not covered by the final rule will benefit because the prompt payment of deposit insurance at the largest IDIs should promote public confidence in the banking system as a whole. The provisions of the final rule will help to level the competitive playing field between large banks with two million or more deposit accounts and community banks, which typically maintain far fewer deposit accounts. The requirements of the final rule will reduce the perception that uninsured depositors at large banks are less likely to incur losses in the event of failure than their counterparts at smaller institutions.

The enhancements to data accuracy and completeness supported by the final rule should benefit covered institutions as well. Improvements to data on depositors and information systems as a result of adopting the final rule may lead to efficiencies in managing customer data. Accordingly, the upgrades in depositor information required under this rule are likely to benefit covered institutions by improving their ability to serve their customers and increasing their depositors' confidence that deposit insurance can be paid promptly by the FDIC in the event of failure. Moreover, the processing of daily bank transactions may be less prone to data errors.

V. Alternatives Considered

A number of alternatives were considered in developing the final rule. The major alternatives include (1) adjusting thresholds above or below the proposed two million accounts, (2) imposing recordkeeping requirements on all account types, (3) maintaining the FDIC's current approach to deposit insurance determinations (status quo), (4) developing an internal IT system and transfer processes within the FDIC capable of subsuming the deposit system of any large covered IDI in order to perform deposit insurance determinations, and (5) simplifying deposit insurance coverage rules. The FDIC considers the final rule to be the most effective approach among the alternatives in terms of cost to the industry, the speed and accuracy of deposit insurance determinations, access to funds, and reduction of systemic and information security risks. Development of the final rule was based on a careful evaluation of expected effects, public comments, and the FDIC's experience in resolving failed banks.

In deciding which institutions would be subject to the final rule, the FDIC considered thresholds above and below two million deposit accounts. Raising the threshold would decrease the costs of the final rule to the industry because fewer institutions would be covered, but would also increase the risk that the FDIC would be unable to make timely and accurate deposit insurance determinations for large institutions and limit the FDIC's resolution options, thereby potentially increasing the costs of resolution.

Making a correct and timely deposit insurance determination requires that the FDIC have access to accurate data on deposit accounts as well as on any relationships among those accounts. The FDIC has learned from prior experience that it is possible to manage data quality problems at small institutions without delaying or materially altering the outcome of the deposit insurance determination. However, the ability of the FDIC to promptly manage data quality problems at large institutions declines rapidly with the number and complexity of deposit accounts. Therefore, resolving data quality problems at institutions with the largest number of accounts and most complex deposit account systems prior to failure, as required by this final rule, should substantially lower the risk of inaccuracy or delay in making determinations.

As described in IV. Expected Effects, the FDIC estimates that the costs associated with the two million account threshold for these large IDIs will be relatively modest compared to their net income and other costs of doing business. Decreasing the threshold below two million accounts would impose higher costs on the industry as a whole, and the marginal benefits of Start Printed Page 87745the rule would decline since smaller institutions present less risk to prompt deposit insurance determinations.

In determining the scope of the final rule, the FDIC considered requiring covered institutions to maintain complete and accurate records for all accounts as originally proposed. However, the FDIC recognizes that covered institutions may not maintain in their deposit account records, and may not be able to obtain, for all accounts the information needed for deposit insurance purposes. The FDIC's regulation that sets forth the standards for deposit insurance coverage, 12 CFR part 330, permits records to reside outside of an IDI with respect to certain types of deposit accounts, as long as certain requirements are satisfied, without adverse consequences for the insurability of deposits. Similarly, the final rule recognizes that covered institutions will not have and therefore do not need to keep complete records for deposit insurance purposes for those types of deposit accounts.

Additionally, costs associated with developing the ability to collect data, produce key account holder information in a timely manner, and perform a deposit insurance calculation are estimated to be relatively high for some account types. For example, for covered institutions the costs associated with collecting key information regarding beneficial ownership of deposits held by a prepaid account program manager on behalf of program participants is likely to be higher than for other account types for which beneficial ownership can be readily determined. For trust accounts, the identity and number of beneficiaries can often change, making the costs associated with collecting key information from the account holder, trustee, or other interested parties relatively high.

Another alternative is to maintain the status quo established by 12 CFR 360.9. However, that rule does not adequately address an important problem that arises in the resolution of the largest and most complex institutions. Deposit insurance determinations under § 360.9 necessitate a secure bulk download of depositor data that introduces additional delays in making determinations. The FDIC's experience in resolving large institutions shows that the amount of time for data to download can vary widely based on the file size, complexity of the data, and the number of deposit systems, among other things. Given the limited time available to the FDIC to make determinations, these delays pose the risk of creating financial hardships for depositors and disrupting financial markets.

Another alternative considered was to establish a system to rapidly transmit all deposit data from a failed IDI's IT system to the FDIC for processing in order to calculate and make deposit insurance determinations. Although this alternative utilizes a common deposit insurance calculation IT system, absorbing the deposit system or systems of a large, complex institution quickly enough to make a prompt insurance determination is infeasible as a practical matter. Unlike typical small and mid-sized IDIs, covered institutions have large amounts of data and often use multiple deposit account IT systems which are programmed to meet institution-specific needs. FDIC staff, working with staff from each large institution, would have to develop an individualized solution for each institution tailored to its IT systems and third-party applications. Extensive initial and ongoing testing would be required to establish that the data transmission would allow a prompt and accurate insurance determination. Additionally, covered institutions would still bear the cost of legacy data cleanup and data aggregation, which are the two largest cost components in the cost model.

The alternative of the FDIC establishing an IT system to rapidly transfer all deposit data from a failed IDI would also likely impose large ongoing costs for covered institutions because any significant change to the deposit system of a large IDI would necessitate further testing and validation. Further, the large IT development, testing, and recertification costs borne by the FDIC under this alternative would ultimately be paid by insured depository institutions through ongoing deposit insurance assessments. In contrast, the final rule requires that a covered institution's IT system have the ability to calculate deposit insurance coverage for all deposit accounts in the event of a failure. It would use the data that the covered institution has on hand at the time of failure as well as data collected by the FDIC from depositors shortly after failure. Under the final rule, IT costs would be absorbed by covered institutions rather than by the entire banking industry.

Another alternative the FDIC considered was to simplify deposit insurance coverage rules. Currently, deposit insurance is provided under different ownership rights and capacities, some of which involve complex types of deposit accounts. Reducing the number of rights and capacities or simplifying the coverage rules would reduce the costs associated with covered institutions' development of the capability to calculate deposit insurance coverage. However, efforts to simplify the deposit insurance coverage rules could effectively reduce coverage to depositors at all FDIC insured institutions, an approach that would impose a cost on a wider range of institutions and bank customers. Further, these complex account types present problems when the FDIC must analyze a significant number of these accounts at the same time. The FDIC's established methods for dealing with these more complex accounts in smaller and mid-sized resolutions include manual processing, an approach that could take too long in a larger resolution involving a significant number of these accounts. Consequently, the FDIC is not pursuing simplification of the deposit insurance coverage rules.

VI. Discussion of Comments

Generally, the issues raised by the commenters may be categorized under the following topics: The need for regulation, expected effects of the proposed rule, possible alternatives to the proposed rule, problems with the proposed rule's requirements, and possible adverse consequences.

A. Comments Concerning the Need for Regulation